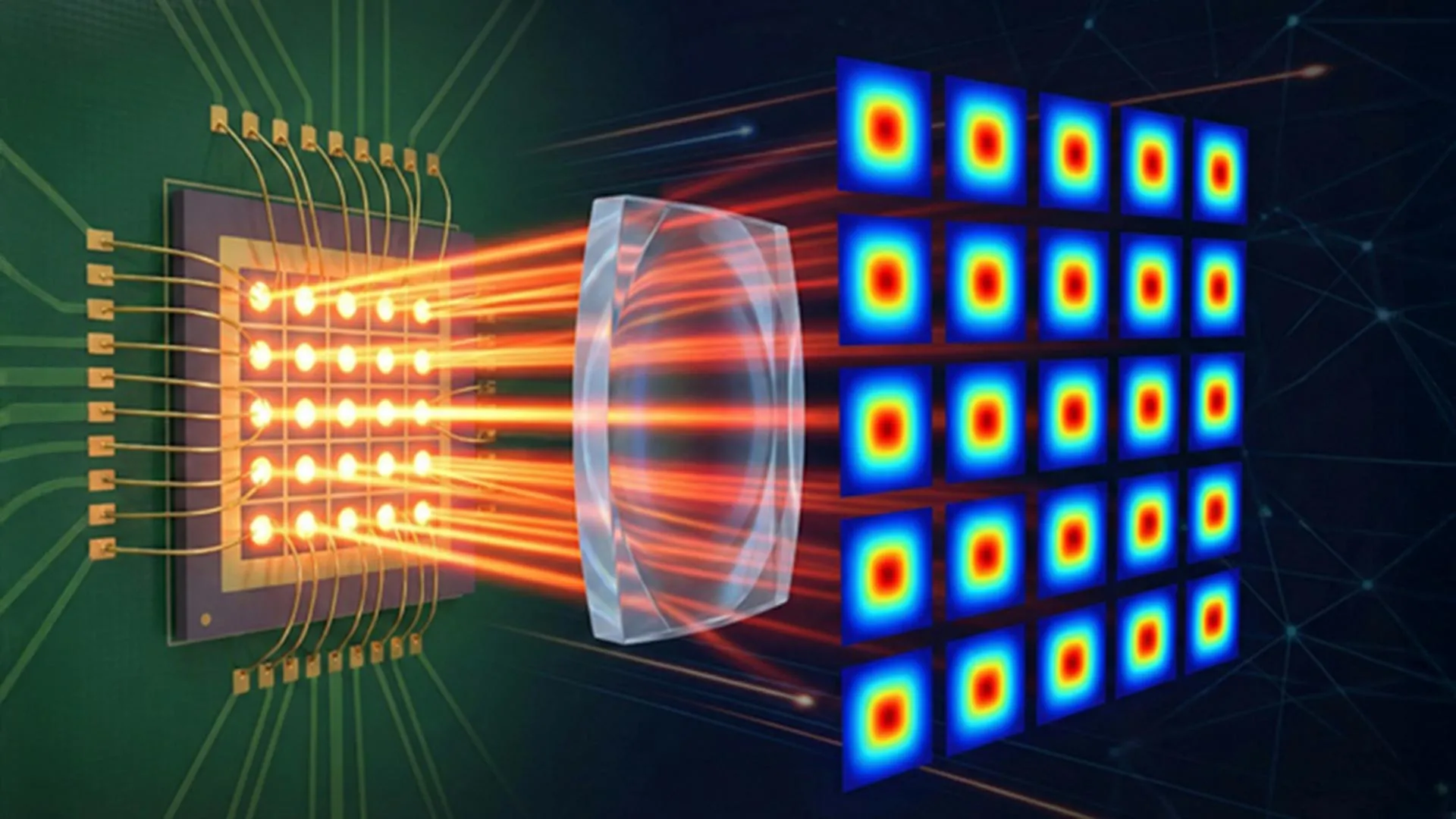

Researchers demonstrated a chip-scale 5×5 VCSEL laser array achieving a combined free-space optical throughput of 362.7 Gbps (21 of 25 lasers active; individual lasers ~13–19 Gbps) over a 2 m link. Measured energy consumption was ~1.4 nJ/bit—about half that of leading Wi‑Fi under comparable conditions—and beam shaping produced >90% uniformity to enable multiuser links. Performance was limited by the commercial photodetector bandwidth, implying higher speeds possible with better receivers; the design is compact (<1 mm chip) and targeted for indoor integration (ceilings, lighting, access points).

This development should be read as the opening salvo of a new indoor bandwidth tier rather than an immediate Wi‑Fi extinction event. The real value accrues to firms that can scale high-volume VCSEL production, integrate beam‑forming optics into ceiling fixtures, and—critically—solve the receiver/photodetector bottleneck; expect meaningful commercial wins only after one to three years of supply‑chain ramp and receiver advances. Second‑order winners include contract manufacturers and capital‑equipment vendors that enable III‑V processing at commodity volumes; conversely, consumer‑focused Wi‑Fi chipset growth could decelerate in dense enterprise deployments where optical offload is economical. Regional manufacturing concentration for compound semiconductors (fabs, substrates, specialized tools) creates a geopolitical supply risk that could compress margins for smaller optical component suppliers even as demand increases. Adoption is gated by standards, eye‑safety/regulatory approvals, and the user‑mobility problem (handsets/AR devices need robust non‑line‑of‑sight or rapid beam‑steering solutions). If standards and receiver ecosystems coalesce within 24 months, expect a discrete capital cycle: lighting OEMs, enterprise AP vendors, and datacenter interconnect suppliers will either acquire optical specialists or partner tightly; if not, commercial deployments will remain niche and incumbents can blunt disruption through improved Wi‑Fi energy and spectral efficiency. Monitor patent filings and M&A flow among optical startups—an acceleration there is the fastest path from lab demo to customer rollouts and is the primary catalyst that would re‑rate small-cap optics names in under 18 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30