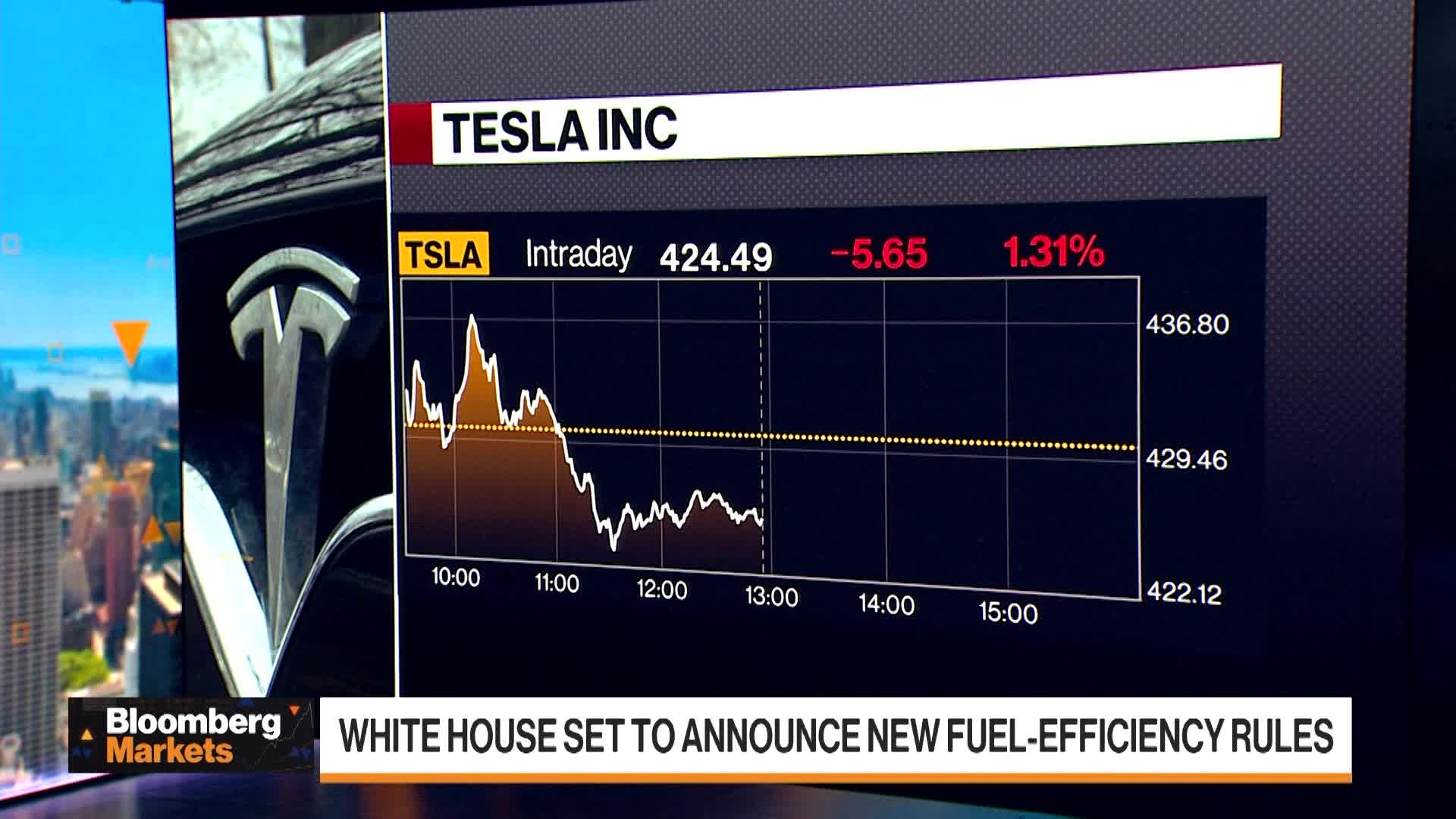

Average new-car transaction prices are roughly $50,000 as of September, and the Trump administration has rolled back fuel-economy penalties and eliminated the prior $7,500 EV tax credit, reducing automakers' need to purchase EV credits and lowering pressure to sell electric vehicles. The policy shift is intended to improve affordability and protect auto jobs, potentially benefiting legacy automakers and lowering EV adoption headwinds, while tariffs remain a multi-billion-dollar cost headwind that manufacturers are partially absorbing. For investors, the net effect is sector-specific: potential margin relief and reduced regulatory costs for traditional OEMs versus a weaker structural tailwind for EV makers, offset by tariff-driven cost risk.

Market structure: Rolling back fuel-economy requirements and zeroing-out credit penalties structurally benefits legacy ICE OEMs (e.g., F, GM) by lowering compliance costs and reducing the need to buy EV credits from Tesla, while harming high-valuation pure-play EV sellers (TSLA sentiment -0.65). Expect OEM gross-margin relief of ~50–250 bps over 12–24 months if EV-premia and credit purchases decline, but tariffs still impose multibillion-dollar headwinds that will offset some pass-through to consumers. Risk assessment: Immediate market moves (days) will be headline-driven around policy releases and court challenges; short-term (weeks–months) the key risks are tariff escalations and state-level standards (CA) creating patchwork compliance costs; long-term (1–3 years) the biggest tail risk is accelerated state/federal litigation or a rebound in oil prices that re-accelerates EV demand. Hidden dependencies include consumer finance rates, used-car price normalization, and supplier covenant stress — monitor auto supplier bond spreads for early signs of margin squeeze. Trade implications: Prefer selective long exposure to legacy OEMs and ICE-supplier suppliers (APTV, BWA) sized 1–3% positions with 6–12 month horizons, funded by short/hedged positions in TSLA (options-based) and battery/miner names. Use put spreads on TSLA (3–9 month) to express downside while selling covered calls on stabilized OEM longs; expect relative outperformance of ICE supply chain by 10–30% if EV incentive frameworks remain weakened. Contrarian angles: Consensus assumes lower car prices will quickly boost volumes — that ignores consumer-rate sensitivity and manufacturers absorbing tariffs. History (past fuel-rule relaxations) shows regulatory reversals typically shift timing not the long-term secular trend: battery cost curves + state mandates can re-tighten EV demand within 12–36 months, so size positions small and timebox them to policy/court catalysts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment