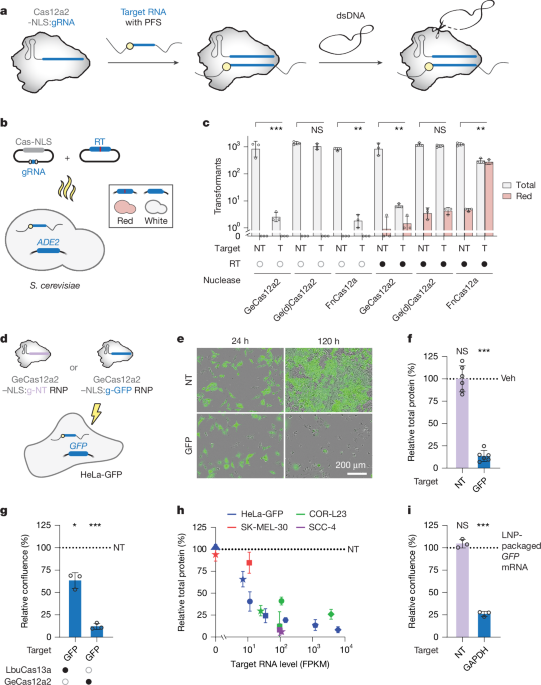

The article reports that CRISPR-Cas12a2 can selectively kill eukaryotic cells by sensing target RNA, enabling programmable elimination of yeast and human cells with minimal observed off-target activation. It demonstrates applications including removal of HPV-infected cells, enrichment of gene-edited cells by up to 4.3-fold, and selective depletion of KRASG12C cancer cells, with in vivo tumor-growth reduction shown in a mouse model. This is a meaningful platform advance for biotech and therapeutic development, though it is still pre-commercial and likely to have limited near-term market impact.

This is a platform-expansion story, not just a one-off academic result. The key second-order effect is that RNA state becomes an actionable kill-switch for eukaryotic cells, which materially broadens the addressable market versus DNA-editing tools that still depend on endogenous repair or repetitive targets. That makes the relevant competition less “CRISPR vs CRISPR” and more “programmed cell death vs antibodies/toxins/viral vectors,” with a faster design cycle and potentially cleaner specificity than protein-targeted biologics. The most important near-term commercial signal is not oncology efficacy per se, but enrichment use cases: counterselecting unedited cells, enriching prime-edited cells, and removing unwanted subclones. Those are upstream workflow products that can be sold into research tools, cell therapy manufacturing, and ex vivo editing, where even modest enrichment lifts can improve batch economics and reduce QC failure rates. If that holds, the initial revenue pool may be more in enabling reagents and delivery systems than in direct therapeutics, which lowers regulatory friction and shortens the path to monetization. The main risk is not specificity in the narrow sense; it’s delivery, expression threshold, and survivorship bias. The kill mechanism looks brutally potent once triggered, but the commercial ceiling depends on whether the system can be packaged safely, activated only in intended cells, and scaled beyond localized or ex vivo settings over the next 12–36 months. Any credible signal that PFS constraints are relaxed, or that a compact/high-fidelity variant improves delivery compatibility, would likely re-rate the whole category. Contrarian view: the market may over-interpret this as immediately therapeutic for solid tumors, when the nearer-term value is probably in manufacturing and research tools. The broader opportunity may also sit in companion diagnostics and guide-design software, because off-target assessment now hinges on transcript abundance and context, not just genome similarity. That shifts the moat toward data, screening, and delivery partnerships rather than a single hero molecule.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.72

Ticker Sentiment