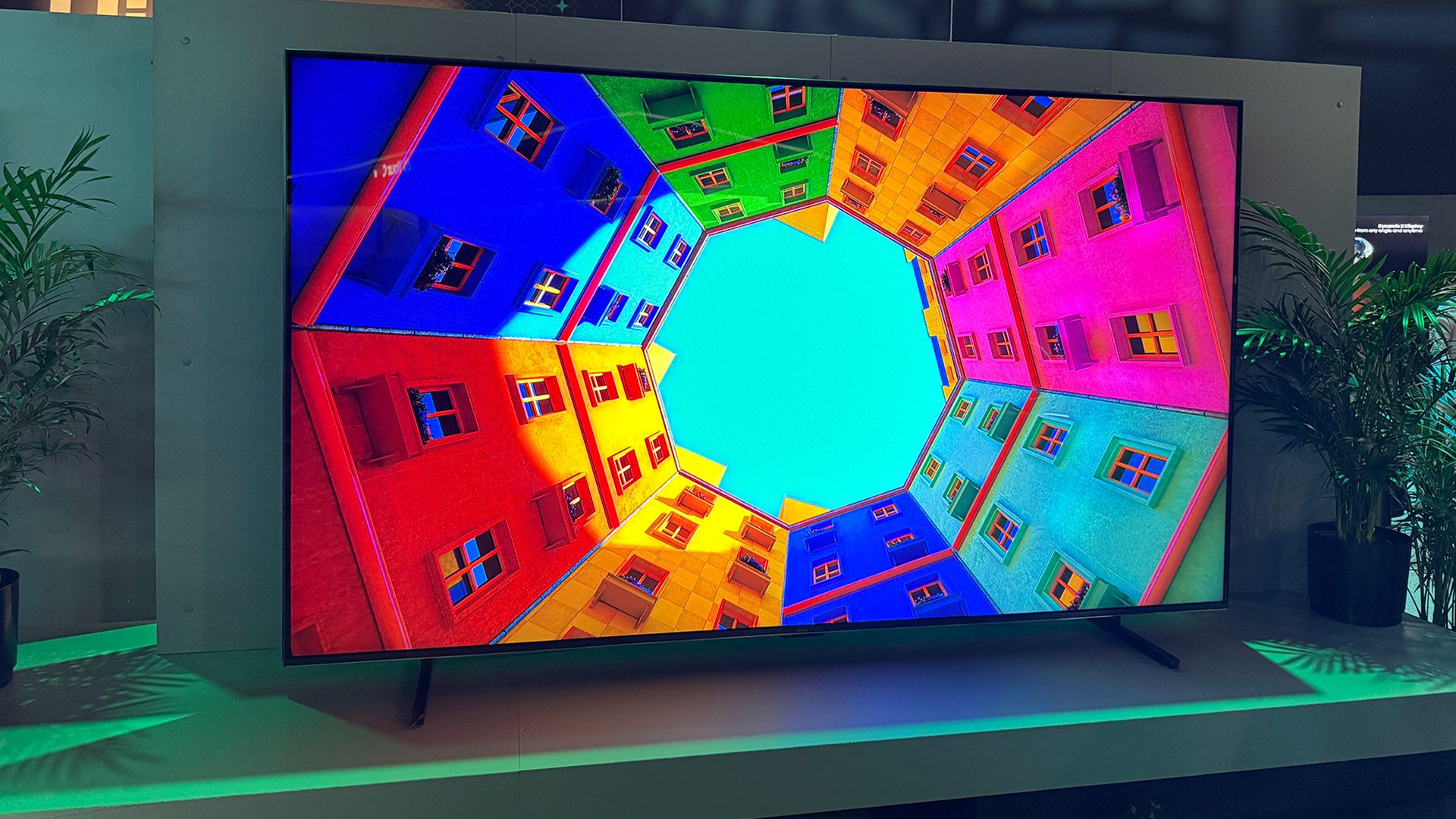

RGB mini‑LED is positioned to be the dominant TV technology story in 2026, with TCL, Hisense, Samsung, LG and Sony planning full series and LG and Samsung already disclosing Micro RGB details ahead of CES; Hisense’s 116‑inch 116UX ($25,000/£19,999) and Samsung’s 115‑inch MRE115MR95F ($29,999/£24,999) are early high‑end examples. The technology uses true RGB backlighting in optical units with local dimming to deliver wider, purer color gamuts (vendor claims include DCI‑P3, Adobe RGB and BT.2020 coverage), higher brightness and improved viewing angles, which could pressure OLED positioning if mainstream sizes and lower prices materialize in 2026, though risks persist from backlight blooming, inconsistent local dimming and limited content mastered to exploit the displays’ capabilities.

Market structure: RGB mini‑LED is a classic technology upgrade that benefits consumer electronics OEMs that can execute premium productization (SONY, Samsung, TCL/Hisense OEM partners) and upstream LED/optics suppliers; I expect RGB mini‑LED to capture ~10–20% of the >$1,000 TV segment by end‑2026, pressuring mid‑tier LCD commoditization and raising ASPs by 5–15% in premium channels. Competitive dynamics favor brands with content partnerships and global distribution (SONY) and platform monetization (ROKU) while pure panel makers reliant on legacy white‑LED LCD volumes face margin pressure. Risk assessment: Tail risks include manufacturing yield failure (15–30% lower than modeled yields would delay adoption), supply constraints on GaN/indium components driving input cost spikes (+20% in worst case), and content mismatch slowing consumer pull‑through; regulatory/trade actions on Chinese suppliers could accelerate reshoring/costs. Time horizons: immediate (days) — watch CES coverage and early reviews; short (weeks/months) — shipment announcements and price cuts; long (quarters) — mix shift in TV ASPs and panel demand. Trade implications: Direct plays — long SONY equity and ROKU ad/OS exposure; pair trade long SONY vs short LPL (LG Display ADR) to express hardware premium vs OLED panel risk. Use event options: buy Feb‑2026 call spreads on SONY to cap cost into CES, and buy OTM puts on LPL as asymmetric hedge if OLED demand collapses. Contrarian: Consensus assumes RGB mini‑LED will immediately displace OLED; that’s underdone on content and yield realities — adoption is likely incremental, not wholesale, in 2026. Mispricings: panel suppliers (LPL) may already price in secular OLED strength; a 10–20% downside exists if RGB mini‑LED gains traction. Monitor CES reviews and component spot prices (GaN/indium moves >+15% in 30 days) as reversal triggers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment