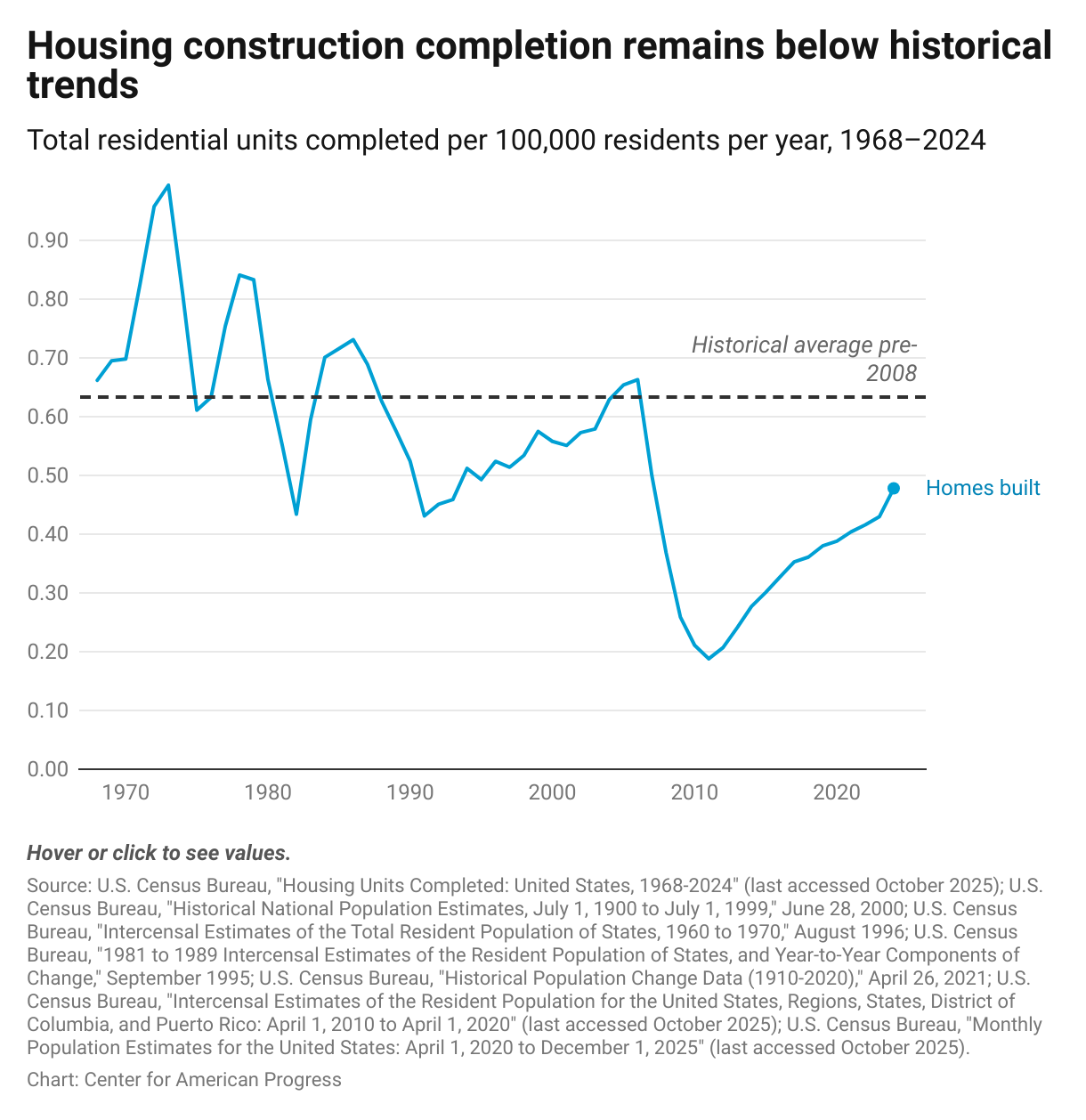

The Center for American Progress proposes a $95 billion, five-year agenda to close a roughly 2 million‑unit U.S. housing shortfall by rapidly scaling supply and cutting other housing costs through three pillars: removing local barriers (including a Rent Relief for Reform program that ties up to $1,000/year in renter relief and discretionary‑grant penalties to measurable housing production), deploying lower‑cost construction at scale (factory‑built homes, a proposed ARPA‑Home innovation agency, relaxed HUD manufactured‑home rules, and targeted tax/finance tools), and consumer protections (tariff exemptions on building materials, curbs on algorithmic rent‑setting and junk fees, federal reinsurance for FAIR plans, and reforms to lower closing and construction finance costs). The plan cites specific impacts—about $1,000 annual savings for a typical renter in high‑cost areas, roughly $24,000 savings for a first‑time buyer, and an estimated $135 billion in five‑year tariff savings on construction inputs—and calls for GSE actions (pilot securitization of single‑close construction loans) while warning against privatization moves that could raise mortgage rates by 0.2–0.8 percentage points. If enacted, the package would accelerate housing starts, shift demand toward modular/manufactured housing and construction finance solutions, and materially affect regional housing markets, construction input demand, and mortgage‑market dynamics.

The Center for American Progress (CAP) lays out a targeted, three-pillar, five-year agenda to close an estimated roughly 2 million unit U.S. housing supply gap at an estimated cost of about $95 billion, combining supply-side production (factory-built homes, ARPA-Home), demand-side relief (Rent Relief for Reform or R3), and consumer protections (tariff exemptions, anti-algorithm rules). CAP projects tangible household impacts: up to $1,000 per year in rent relief for qualifying renters, roughly $24,000 in first-time buyer savings from lower construction and transaction costs, and an estimated $135 billion in construction-cost savings over five years from removing tariffs on materials. Policy mechanics and finance proposals are explicit and investor-relevant: R3 ties up to $1,000/year renter payments to local production targets and discretionary-grant penalties; CAP urges GSE pilots to securitize single-close construction-to-permanent loans to lower financing costs; and reforms to manufactured-home rules could cut unit costs by $5,000–$10,000. The report highlights acute bottlenecks—115,000 permitted-but-unstarted multifamily units in August 2025 versus 81,000 in 2019—and identifies algorithmic rent-setting, junk fees, tariffs, and insurer withdrawals as near-term drivers of cost and regulatory risk. Execution risk centers on local adoption lags (zoning reform timelines of 3–10 years), political resistance to federal conditionality, and potential adverse outcomes from proposed GSE privatization (analysts estimate mortgage-rate increases of 0.2–0.8 percentage points). Investors should therefore differentiate between assets that gain from federal scaling of modular/manufactured production and those exposed to regulatory curbs on fees or to mortgage-rate shocks, and monitor legislative progress and pilot outcomes closely.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.40

Ticker Sentiment