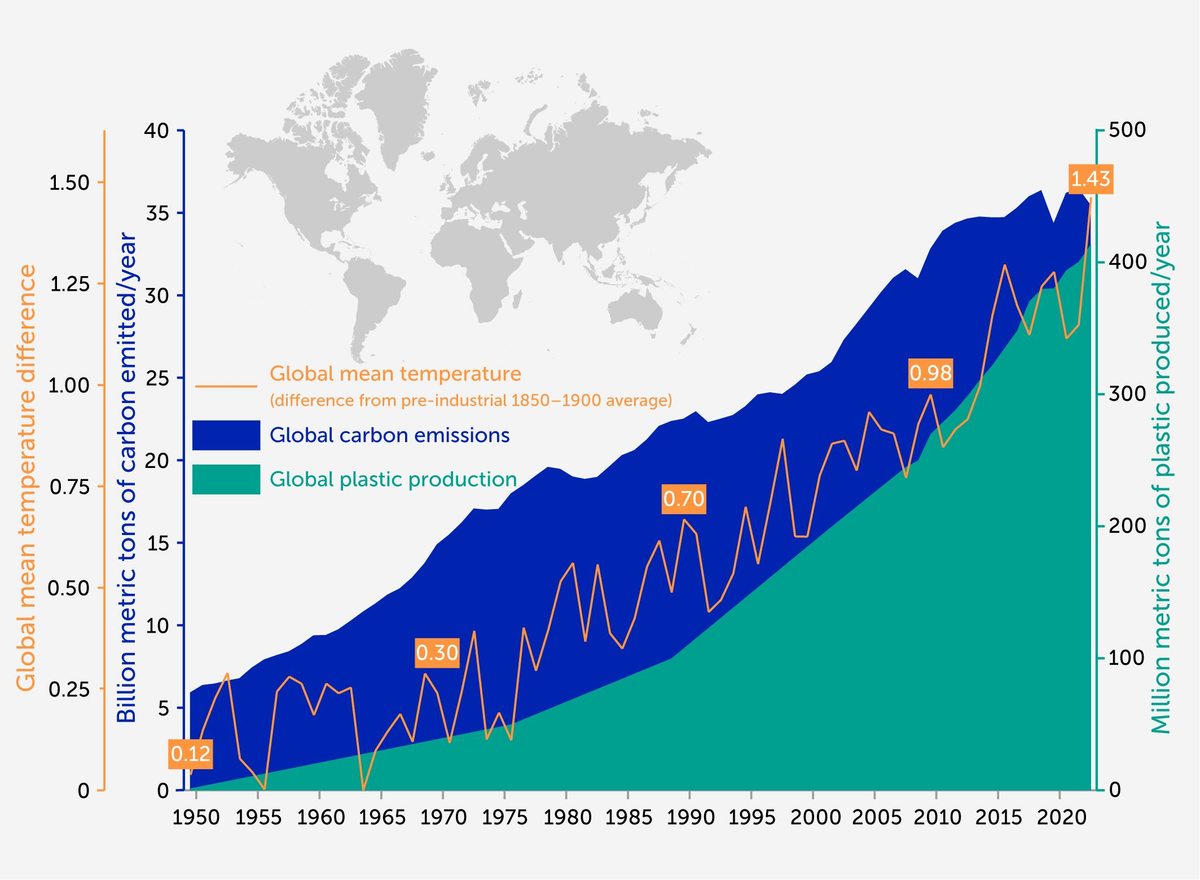

Rising plastic production (from <2 Mt in 1950 to >400 Mt in 2023, projected to triple to ~1,231 Mt by 2060) and its fossil-fuel linkage (over 98% of plastics sourced from fossil chemicals) create growing climate and environmental liabilities, with the plastics life cycle responsible for ~1.8 Gt CO2e (~3.7% of global emissions in 2019). Climate-driven weathering and extreme events accelerate fragmentation and mobilization of micro-/nanoplastics (≈22 Mt leakage/year; ≈6 billion tonnes accumulated), amplifying exposure and regulatory risk — underscored by the breakdown of Global Plastics Treaty talks in Geneva (Aug 2025). Hedge funds should factor heightened policy, reputational and supply-chain risks for petrochemical and waste-exporting businesses while assessing investment opportunities in circular-economy technologies, waste-processing, remediation and related green-finance solutions.

Market structure: Rising plastic production (projected ~3x to 2060) and climate-driven remobilization create near-term winners: integrated oil & gas with petrochemical exposure (e.g., CVX, XOM segments) and commodity chemicals (DOW, LYB) that supply ethylene/propylene; waste-management & circular-economy operators (WM, RSG, VEOEY/Veolia ADR) gain pricing power for collection/recycling services. Losers include pure-play biodegradable/alternative-material firms that raise lifecycle GHGs (reducing political support) and consumer staples (PG, KMB) facing higher compliance costs. Commodities impact: naphtha/LPG/ethylene tightness → upside pressure on petrochemical spreads; corporate capex into recycling implies higher debt issuance in the chemicals/waste sector. Risk assessment: Key tail risk is a legally binding global plastics treaty (probability medium over 1–3 years) that could impose production caps or additive bans and compress petrochemical EBITDA 15–25% for pure plastics producers; a second tail is accelerated carbon pricing on incineration (material to WM margins). Immediate (days–months): reputational/regulatory headlines can swing stocks ±10–20%; medium (6–18 months): legislation and capex plans; long (2–10 years): physical contamination feedbacks and stranded-asset risk. Hidden dependency: fossil-fuel majors pivoting to petrochemicals slows net-zero investment and links oil prices to plastic demand. Trade implications: Tactical plays—establish a 2% long position in WM and 1.5% in RSG (12–24 months) to capture persistent waste-management pricing and take-or-pay recycling contracts; buy a 6–12 month call spread on DOW (ticker DOW) to express petrochemical margin tailwind, funded by selling a nearer-term call (target net cost <0.7% portfolio). Hedge treaty tail risk with 9–12 month 20% OTM puts on LYB (allocate 0.8% as insurance). Pair: long WM, short LYB (equal dollar) as relative-value trade if treaty momentum re-appears. Monitor UNEP/INC resumption within 60–180 days as trigger. Contrarian angles: Consensus underestimates that replacing plastics often raises GHGs — policymakers may prefer circularity/regulation over outright bans, favoring recyclers/waste managers over substitute-material makers. Market may be underpricing early-stage bioremediation/IP (high-risk, high-return): consider a 0.5% venture allocation to validated microbial/enzymatic platforms. Beware unintended consequences: heavy investment into petrochemical capacity now creates stranded risk if an aggressive treaty materializes; size positions accordingly and use option hedges.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30