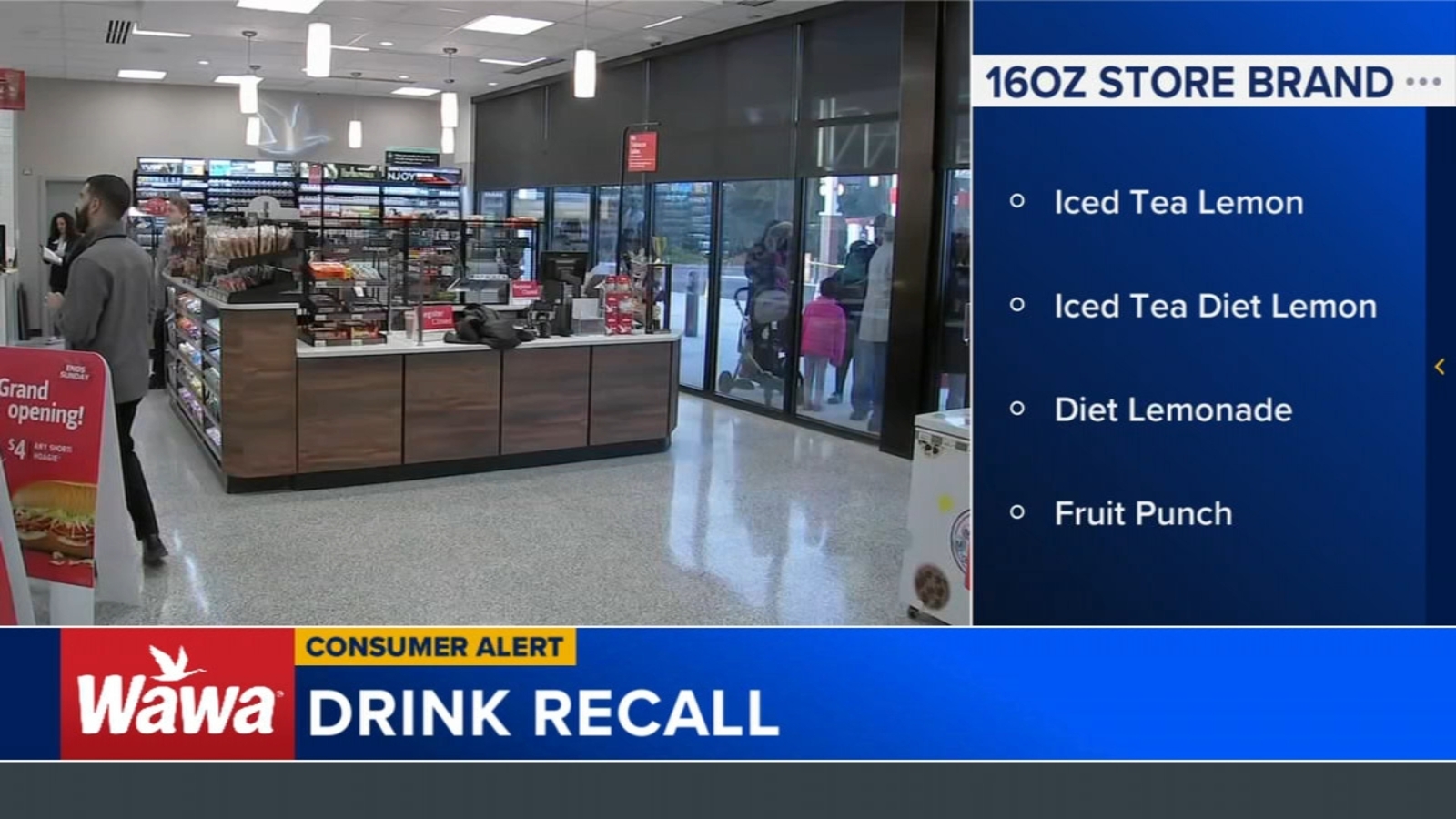

Wawa is recalling four 16-ounce bottled drinks after the FDA reported a production-equipment issue that may have introduced a milk allergen. Affected SKUs (Iced Tea Lemon, Diet Iced Tea Lemon, Diet Lemonade, Fruit Punch) sold in DE, MD, NJ, PA and VA have been removed from stores and customers are urged to discard purchases. No illnesses have been reported, limiting near-term health impact; primary concerns are localized sales loss and reputational risk rather than broader market effects.

This is a localized food-safety shock with outsized second-order effects on compliance spend, inspection frequency, and channel mix rather than on top-line demand for beverages broadly. Expect a near-term (days–weeks) shift of some volume from pre-packaged SKUs into made-to-order and fountain/beverage stations—a structural plus for operators and brands that control on-premise dispense and digital ordering. Over 3–12 months, elevated internal audits, third‑party testing, and potential insurer rate‑filing activity will raise per-store fixed costs; a conservative estimate is $5k–$30k incremental one‑time remediation and audit spend per affected location, plus recurring lab/testing budgets thereafter. If regulators push mandatory traceability or more frequent testing, capitalized compliance costs scale non-linearly for smaller, fragmented operators and private-label bottlers, advantaging large chains and integrated systems with centralized QA. Competitive dynamics favor operators and suppliers who sell fresh or made-to-order beverages (margin-accretive, higher ticket) and vendors of testing/compliance services. Large foodservice brands with established mobile/loyalty ordering can capture displaced transactions quickly and at higher share-of-wallet; that’s a tactical demand reallocation, not permanent brand abandonment, so monitor cadence of repeat behavior over 4–12 weeks. Conversely, single-SKU third‑party bottlers and smaller c-store operators face both one-time disposal/recall costs and longer-term insurance and audit burdens that compress thin operating margins. Watch state-level regulatory responses: a single aggressive inspection regime in the mid‑Atlantic could become a template for other states within 2–6 months, increasing the scope and duration of the impact. Key tail risks: a reported illness cluster (low probability) would dramatically amplify brand damage and regulatory intervention—convert a minor retail event into multi-state litigation and recall cycles over 6–24 months. Reversal catalysts include quick, transparent remediation with third‑party validation (which would cap reputational damage within 2–4 weeks), or a consumer indifference pattern where convenience trumps precaution, muting any long-term shift in channel mix. For portfolio positioning, prefer scale, centralized QA, and public vendors of testing/compliance exposure; avoid undifferentiated bottlers and lightly capitalized independents where fixed-cost shocks are most pernicious.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25