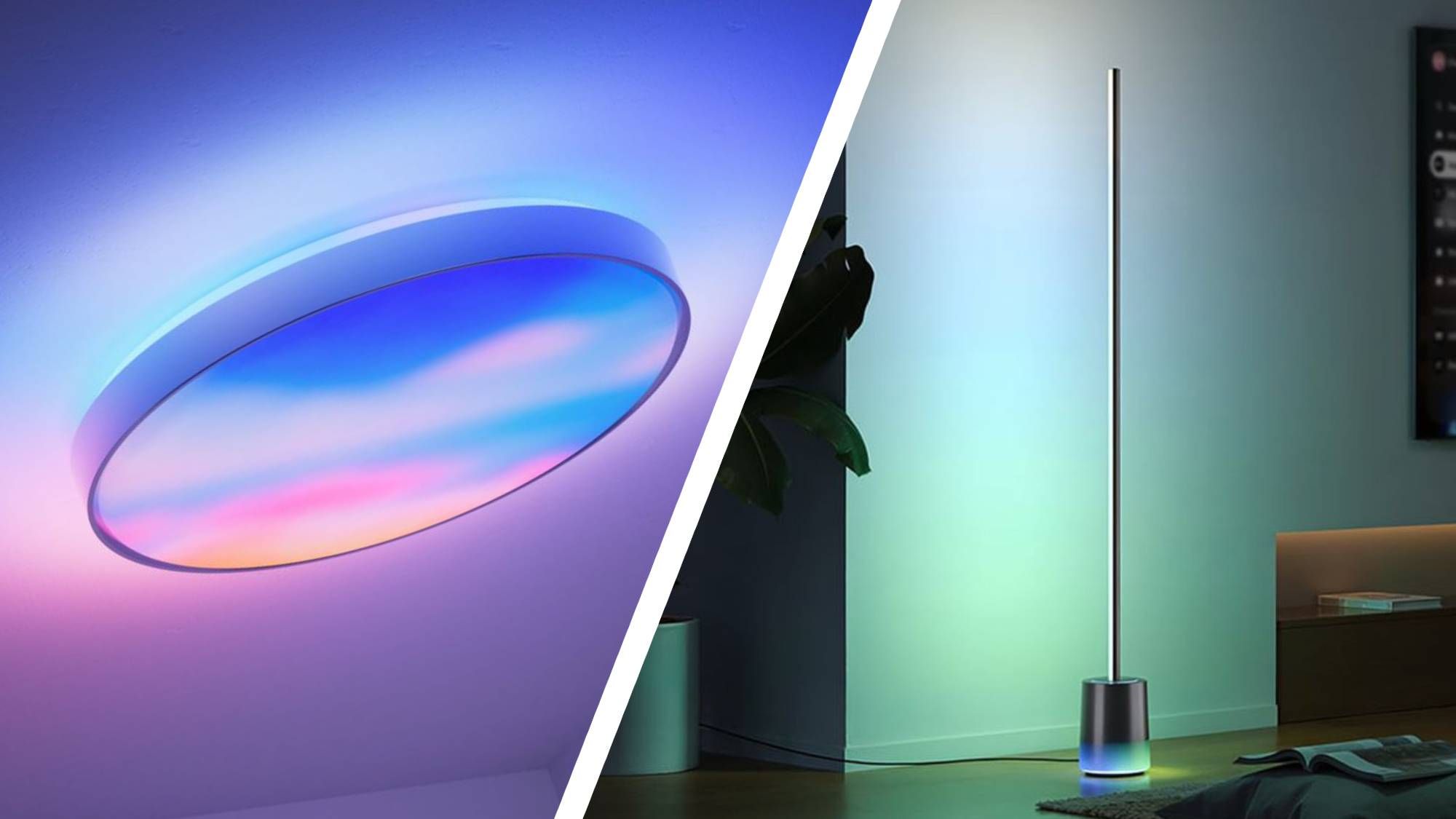

Govee disclosed three new Matter- and HomeKit-compatible smart lighting products at CES 2026 — Floor Lamp 3 (upgraded LuminBlend+ allowing control of ~281 trillion colors and 1,000–10,000K color temperature), Ceiling Light Ultra (21-inch, 616-pixel LED matrix, 5,000 lumens, up to eight animation layers and 20+ presets) and Sky Ceiling Light (21-inch, 5,200 lumens, edge-mounted LEDs that emulate a skylight). The company also launched software features DaySync (time-of-day/sunrise-sunset/local condition-driven lighting) and AI Lighting Bot 2.0 (natural-language scene adjustments), positioning Govee as a stronger competitor to premium offerings like Philips Hue, although pricing and availability were not disclosed.

Market structure: Budget smart‑lighting incumbents (Govee, Amazon/retail channels) are the direct winners; premium ecosystem players led by Signify (Philips Hue, ticker LIGHT) face incremental share pressure. I estimate Govee’s improved software + Matter/HomeKit support could capture 3–5% global color‑bulb unit share within 12–24 months if priced >20% below Hue, compressing LIGHT’s ASPs and gross margins by 100–300bp in that window. Apple (AAPL) is a mild beneficiary as broader HomeKit device counts raise platform stickiness and accessory spend per user. Risk assessment: Tail risks include a security/privacy incident or major firmware recall that halts Govee shipments (high impact, low probability) and regulatory scrutiny if bundling AI features with data collection emerges (6–24 months). Immediate (0–30 days) impact will be muted absent pricing and availability; short term (1–6 months) reviews and launch pricing will drive volatility; long term (6–24 months) depends on Matter adoption and ecosystem lock‑in. Hidden dependencies: app UX, retail placement (Amazon/BestBuy), and supply chain for high‑density LED matrices — any disruption amplifies downside. Trade implications: Tactical pair trade — establish a 1–2% long AAPL position (benefit from HomeKit expansion, target 6–12% upside over 3–9 months) and a 1–2% short position in LIGHT expecting 5–12% downside over 6–12 months if Signify loses pricing power. Options: buy 3–6 month OTM puts on LIGHT (5–10% OTM) sized to cap downside and sell a 6–9 month AAPL 2–5% OTM call spread to fund exposure. Entry: wait for official pricing or first retail reviews (target 2–8 weeks); add if LIGHT outperforms on sentiment by >10% without fundamentals. Contrarian angles: Market may underprice the value of Govee’s AI Lighting Bot 2.0 + DaySync as a defeatable moat for premium users — if verified in reviews, the competitive impact could be faster than consensus. Conversely, the consensus may overestimate disruption: Hue’s ecosystem stickiness and professional installer channel could blunt share loss, so avoid large one‑sided shorts; trim short LIGHT if it rallies >8% on partnership/news not tied to units sold. Historical parallel: Philips Hue faced similar budget entrants in 2018–20 and recovered via ecosystem and services; timeline to judge: 6–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment