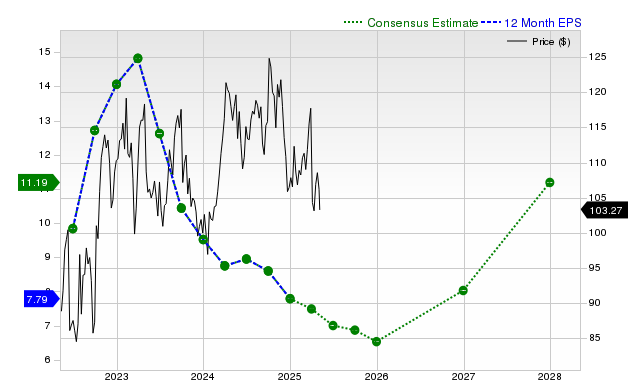

Exxon Mobil (XOM) is attracting significant investor attention despite underperforming the S&P 500 by returning -1% over the past month. While current fiscal year earnings and revenue are projected to decline, analysts have recently revised EPS estimates upwards, contributing to a Zacks Rank #3 (Hold) that suggests near-term market-aligned performance. The company has consistently beaten EPS estimates in the last four quarters and is currently valued at a discount relative to its peers.

Exxon Mobil (XOM) presents a mixed fundamental picture, characterized by recent stock underperformance and near-term operational headwinds, yet offset by improving analyst sentiment and an attractive valuation. The stock's -1% return over the past month lags the S&P 500 composite's +4.5% gain. This performance aligns with significant projected year-over-year declines for the current quarter, with consensus estimates pointing to a -31.8% drop in EPS to $1.46 and an -11.2% fall in sales to $82.62 billion. For the full fiscal year, earnings are expected to decrease by -17.7% and revenue by -4.2%. However, a counter-narrative is emerging from recent analyst activity; consensus EPS estimates have been revised upwards over the last 30 days by +4.9% for the current year and +1.5% for the next. This optimism is centered on a forward-looking recovery, with next year's EPS projected to grow +13.4%. While the company has consistently beaten EPS estimates over the last four quarters, it has only surpassed revenue targets once in that period, indicating potential top-line pressure. This is balanced by a favorable valuation, with a Zacks Value Grade of 'B' suggesting the stock is trading at a discount to its peers, which ultimately culminates in a neutral Zacks Rank #3 (Hold).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment