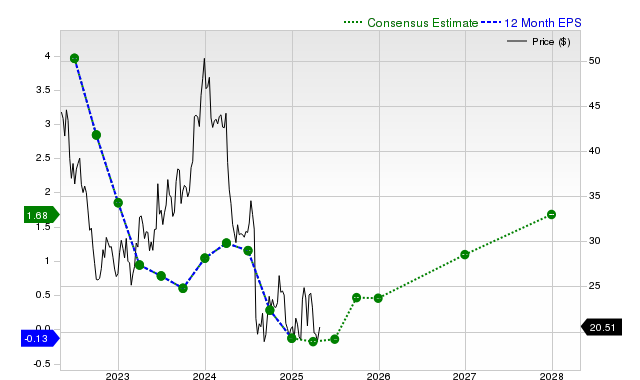

Intel (INTC) is presenting mixed signals, with consensus earnings estimates for the current and next fiscal years experiencing significant downward revisions of -31% and -5.6% respectively over the last month, leading to a Zacks Rank #3 (Hold). Despite these revisions, the company recently surpassed revenue estimates by 8.36% and projects substantial year-over-year EPS growth. However, INTC's stock has underperformed the S&P 500 and the broader semiconductor industry in the past month, suggesting a near-term in-line performance amidst these conflicting fundamental trends.

Intel Corporation (INTC) presents a conflicting fundamental picture, characterized by significant downward earnings estimate revisions that overshadow projected long-term growth and recent top-line strength. Over the past month, the stock's +1.7% return has lagged both the S&P 500 composite's +2.5% gain and the broader Zacks Semiconductor industry's +4.6% advance. This underperformance is primarily driven by deteriorating analyst sentiment, as evidenced by a substantial -31% cut in the consensus earnings estimate for the current fiscal year and a -5.6% reduction for the next, both within the last 30 days. While the company has a strong track record of beating revenue estimates, including an +8.36% surprise in the last reported quarter, this has not translated to consistent profitability, highlighted by a simultaneous -1100% EPS surprise miss. Furthermore, consensus forecasts point to a revenue contraction for the current fiscal year (-1.7%) before a modest recovery next year (+3.8%). With a Zacks Rank #3 (Hold) and a 'C' grade for value, the stock appears to be fairly valued relative to peers, suggesting the market has already priced in these mixed signals.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment