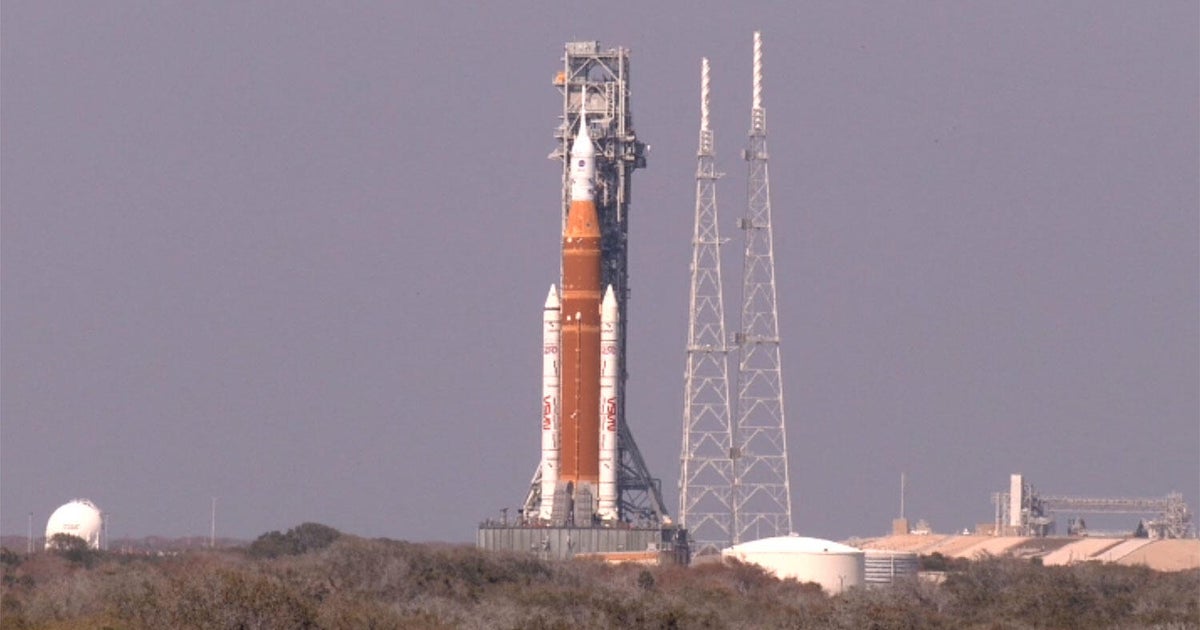

NASA rolled the Artemis II Space Launch System off Pad 38B and back to the Vehicle Assembly Building to diagnose and repair a helium pressurization failure in the Interim Cryogenic Propulsion Stage that surfaced after a second wet dress rehearsal, delaying the crewed lunar flyby from a March window to no earlier than April 1. Engineers used a 6.6-million-pound crawler to move the 3.5-million-pound rocket and 11.3-million-pound mobile launch platform (23.6 million pounds combined) on a 4-mile, 10–12 hour transfer; work in the VAB will allow access to the ICPS to inspect valves, umbilical filters or quick-disconnects and to replace limited-life batteries in the self-destruct and ICPS systems.

Market structure: Near-term winners are large aerospace & defense primes (Lockheed Martin LMT, Northrop Grumman NOC, Boeing BA) and specialist ground-support/avionics suppliers who capture incremental MRO and troubleshooting spend; losers are consumer-space/early-stage orbital tourism names (SPCE) and small single-contract suppliers whose revenue lags if launches slip. Pricing power shifts modestly toward primes that can bundle remediation work and warranty/maintenance contracts; expect 1–3% revenue uplift for primes over the next 6–12 months from additional pad-to-VAB work but concentrated by contractor. Risk assessment: Tail risks include a high-profile on-pad failure causing multi-quarter program halt or congressional funding scrutiny—this could widen speculative-grade aerospace credit spreads by 50–200 bps and compress small-cap equity multiples by 20–40% if delays exceed 6 months. Hidden dependencies: helium supply chains and specialized valve vendors create single-point-of-failure concentration; monitor supplier backlogs and contract change orders over the next 30–90 days as leading indicators. Trade implications: Tactical trades favor small tactical long positions in prime contractors (1–3% portfolio each in LMT/NOC) and thematic exposure via UFO (space ETF) sized 0.5–1% to capture structural secular demand; short selective consumer/early-stage names (SPCE) sized 0.5–1% where sentiment is pricing flawless cadence. Use 3–6 month option structures (buy 10% OTM calls on primes, buy puts or put spreads on speculative names) to express convexity while limiting cash outlay; scale in over 2–8 weeks around official NASA milestones. Contrarian angles: Consensus treats this as operational noise; undervalued is the asymmetric upside for defense primes if NASA shifts more repair/upgrade work on existing contractors—this could justify a +5–10% re-rating versus peers within 3–9 months. Conversely, market may underprice the chance of multi-month slippage cascading into FY budget fights; set price-based stop-losses (e.g., −15%) and a hard reassessment if Artemis misses Q2 (June 30) launch window.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25