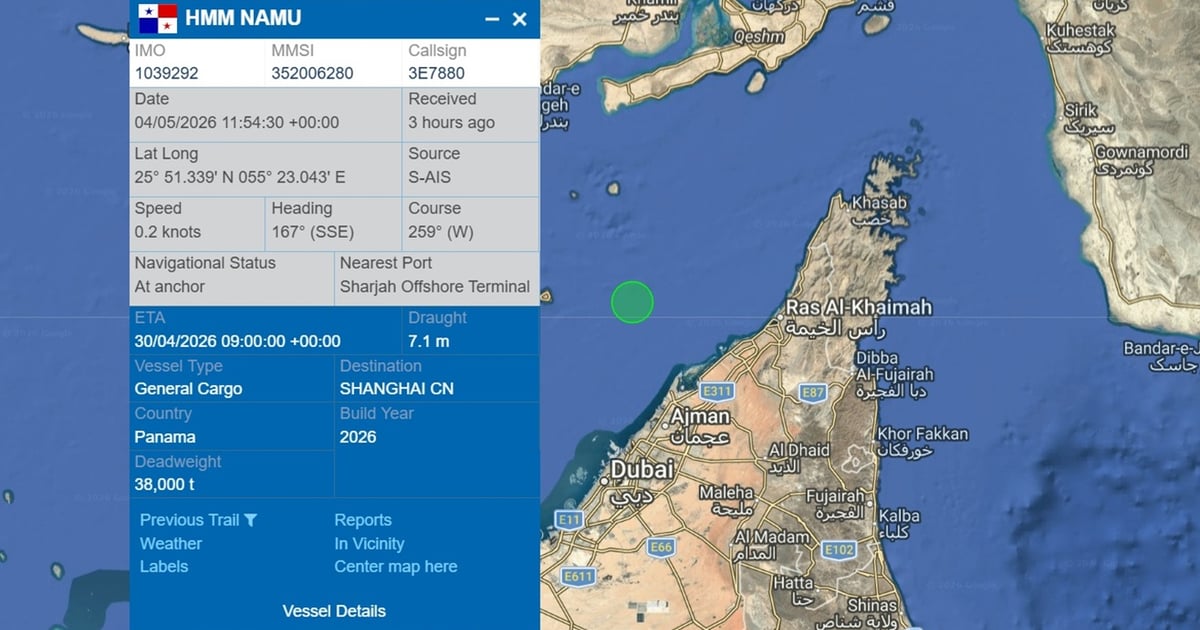

A Panama-flagged South Korean cargo ship, HMM Namu, was hit by an explosion while anchored off Umm Al Quwain, UAE, though all 24 crew are reported safe and no environmental damage has been reported. The incident marks the third attack on a commercial vessel in the region in just over 24 hours, following a suspected drone strike on a tanker 78 nm north of Fujairah and an attack on a bulker west of Sirik, Iran. Iran also announced a new maritime control zone in the Strait of Hormuz, heightening disruption risk for shipping routes and regional freight markets.

This is less about the isolated strikes and more about the probability distribution of shipping risk moving from a one-off shock to a recurring operating constraint. Once anchorages and the approaches to Hormuz are perceived as vulnerable, the market typically prices a higher expected loss via war-risk premia, rerouting optionality, and slower turnaround times before it fully reflects in headline freight indices. That means the first-order impact is on tanker and container utilization, but the second-order winners are marine insurers, private security providers, and shipowners with the cleanest insurance profiles and strongest chartering leverage. The bigger medium-term effect is supply chain friction rather than outright volume destruction. If ships start avoiding waiting areas or idling farther offshore, effective capacity tightens even if nominal ton-miles do not collapse, which is bullish for spot earnings in the most exposed niches and bearish for industries that rely on just-in-time Gulf transshipment. The most vulnerable subsectors are those with low tolerance for delay and high inventory sensitivity: petrochemical feedstocks, auto components, and refrigerated cargoes; the stress will show up first in freight volatility, then in working-capital needs. The tail risk is a misread of attribution that escalates policy response. If market participants interpret more of these events as state-linked or mine-related rather than opportunistic harassment, insurers can re-underwrite the entire region within days, not months, causing a step-function repricing in voyage costs and potentially forcing some owners to suspend Gulf calls. The reversal catalyst is credible maritime escorting plus a period of quiet; absent that, each additional incident compounds into a regime shift where the market assumes the next vessel may be hit before proof of systemic disruption is even visible in trade data.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.55