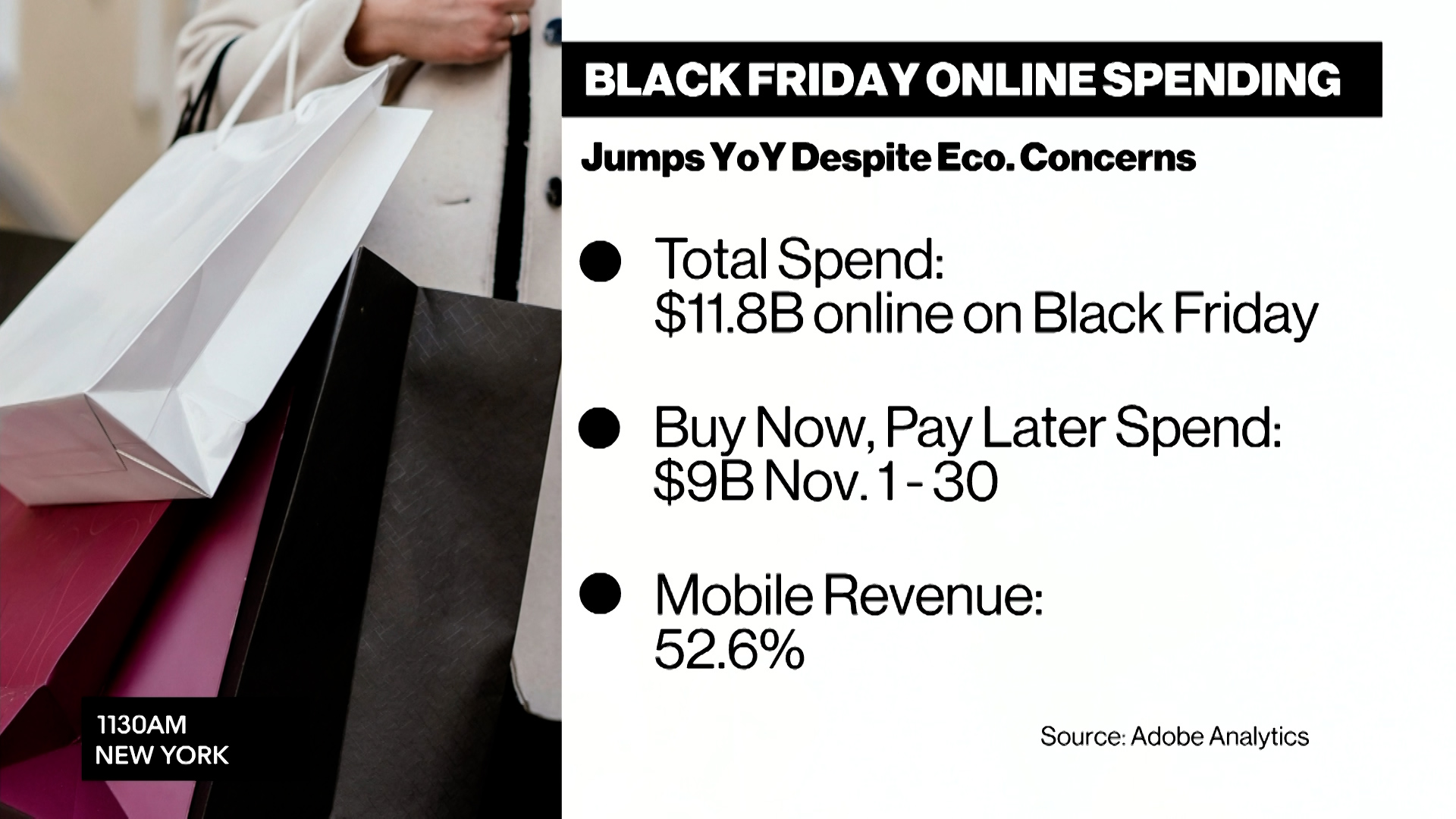

Retail metrics suggest a cautiously optimistic holiday season as in-store traffic and sales growth remain steady while online growth slows off a larger base. Promotions intensified in some specialty apparel categories (discounts up to ~50–60%), though certain brands like Ralph Lauren reduced promo depth (~30% vs 40% last year), and Macy's is highlighting assortment newness (40% newness, 20 new cosmetics brands). Adobe forecasts $20.2 billion in buy-now-pay-later (BNPL) spend this holiday (+11% y/y), retailer earnings have been mixed but generally solid, and consumer demand appears bifurcated with higher-income households continuing to spend while lower-income shoppers are more selective.

Contrarian angles: Consensus underestimates persistence of in-store demand — a sustained 1–3ppt shift of purchase incidence from online to offline over 12–24 months would be underpriced in mall REITs and select retailers. The market may be overindexing BNPL as pure-growth; a 50–100bps rise in delinquencies would compress merchant economics and cause >10% multiple compression for BNPL-native exposures. Historical parallel: post-2009 experiential retail rebound supports a multi-quarter re-rating for curated, low-promo brands; unintended consequence — higher staffing/operating costs could offset gross-margin gains if traffic increases >10% without scale efficiencies.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment