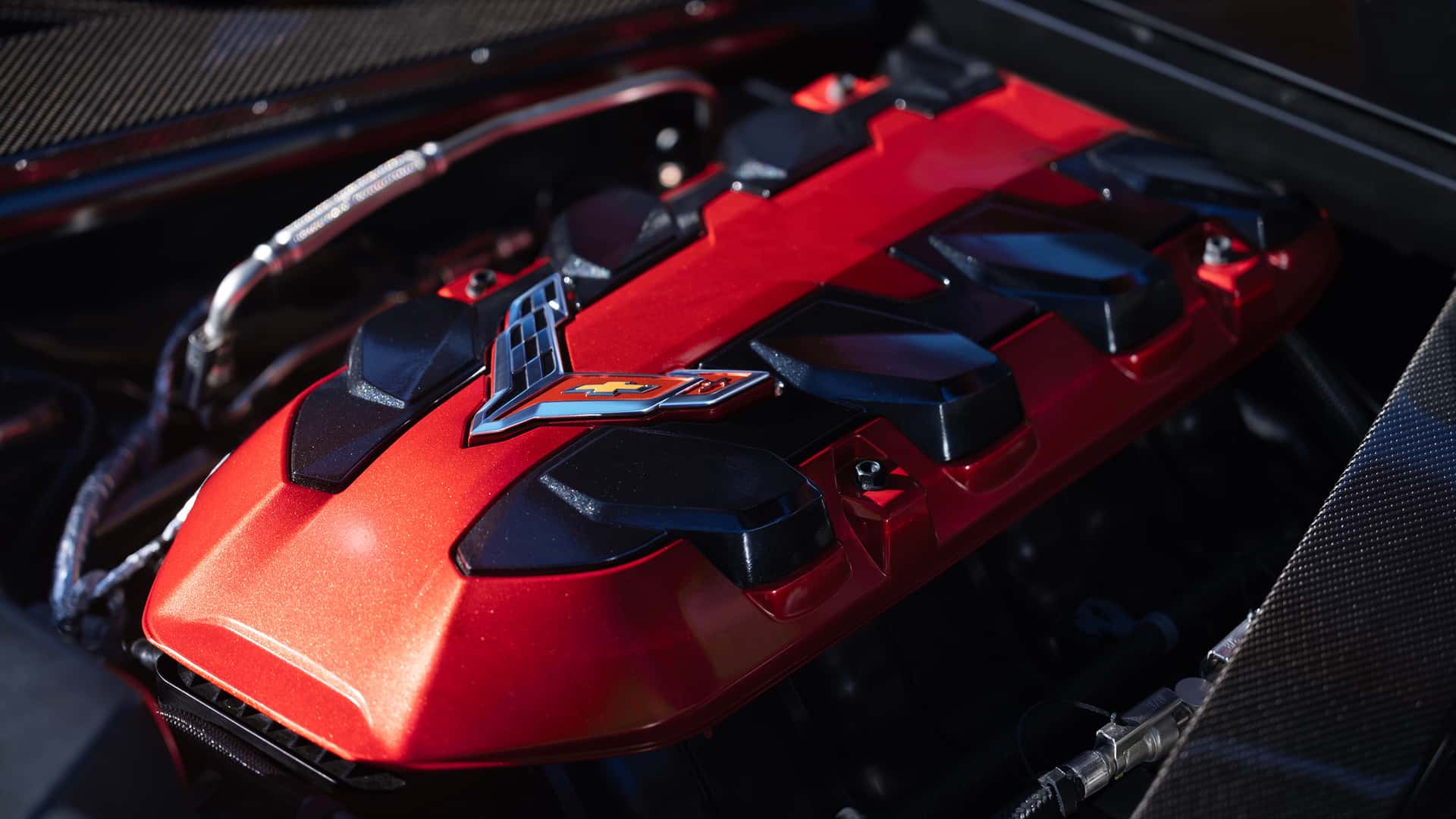

The 2027 Chevrolet Corvette Stingray gains a new naturally aspirated 6.7L LS6 V8 producing 535 hp and 520 lb-ft (up +40 hp and +50 lb-ft vs the outgoing 6.2L). Chevrolet also updated Magnetic Ride Control, offers a ZR1 Performance Pack with a 5.56:1 final drive, revised aero and new Michelin Pilot Sport S 5 tires; pricing is expected to rise from the 2026 base of $72,495 toward roughly $75,000 (~$2.5k, ~3.4% increase) and the updated Stingray should reach dealers this summer.

A recent OEM performance refresh functions as a lineup floor reset rather than a niche halo — that dynamic tends to allow the manufacturer to raise MSRPs across the board while compressing the upside available to direct competitors in the same price band. Over a 3–12 month window expect incremental pricing power to flow to OEM gross margin if production scale is achieved; between 12–24 months the key read will be retail absorption and used-vehicle price signaling.

The non-obvious beneficiaries are component makers with capacity for precision forging, large-bore intake machining and bespoke lubrication subsystems, plus tire makers that win model-specific programs. These are high-margin, low-volume pockets that often require short lead-time capex; expect a transient order lead to translate into 6–18 month revenue visibility and potential backlog-driven beat risk for those suppliers.

Principal risks are demand elasticity and channel behavior: if the OEM lifts MSRP modestly, dealers can offset with incentives, muting margin upside; if they front-load inventory to hit a launch quarter it will create a near-term sales pop followed by weaker comps and higher incentive risk. Over 2–4 years, regulatory push toward hybrids/EVs can shorten the lifecycle premium for incremental ICE performance, capping long-term resale and parts demand.

Contrarian read: market narratives will treat this as sustained product-driven margin expansion, but that underestimates three vectors that can reverse the trade — dealer incentiveing, warranty/quality hiccups on new subsystems, and accelerated electrification of higher-trim variants. Monitor dealer inventory days, early warranty bulletin frequency, and supplier order cadence as high-signal, near-term catalysts that will confirm or reverse the positive thesis.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25