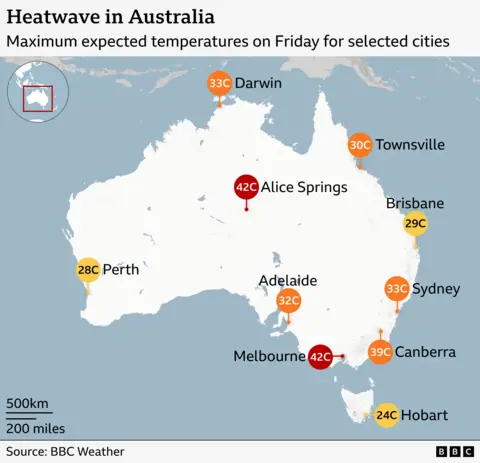

Extreme heat and strong winds have produced 'catastrophic' fire conditions across Victoria and parts of South Australia, with forecasts of around 42C in Victoria and up to 46C in some SA regions. A bushfire near Longwood has burned nearly 36,000 hectares and destroyed at least ten homes in Ruffy, while another blaze near Walwa has consumed more than 17,000 hectares; total fire bans are in place and authorities warn of further property loss, raising localized risks to homeowners, insurers and regional economic activity.

Market structure: Immediate losers are regional homeowners, small commercial property and agriculture (livestock, shearing sheds) with localized credit and cash-flow stress; insurers (IAG, SUN, QBE) face near-term claim spikes and elevated loss ratios. Winners over 3–12 months are building-materials and contractor suppliers (cement, timber, steel) and reinsurers/ILS if catastrophe pricing hardens, as rebuild demand and premium repricing increase revenue/power. Competitive dynamics & supply/demand: Expect a 10–25% increase in regional demand for building materials over 3–6 months, pressuring supply chains and input prices (timber/cement/steel could lift 5–15%). Insurers will try to pass through higher reinsurance costs over 6–12 months, raising premiums and reducing LTV/coverage in high-risk zones, benefiting reinsurers and specialty underwriters. Cross-asset & risks: Near-term risk-off can push AUD down 1–2% and compress 10y Australian yields by 5–15bps; medium-term fiscal relief and reconstruction could increase sovereign issuance and push yields up. Tail risks include multi-state prolonged fires leading to >A$10bn insured losses, regulatory shifts (mandatory building-code upgrades) and supply-chain bottlenecks that amplify price inflation for materials. Trade drivers & catalysts: Key catalysts are weather forecasts, insurer Q-claims releases (next 30–90 days) and reinsurance renewal rounds (notably April renewals). Hidden dependencies include electricity grid strain and agriculture commodity supply shocks; deviations in any of these within 30–180 days can rapidly reprice the trades above.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.70