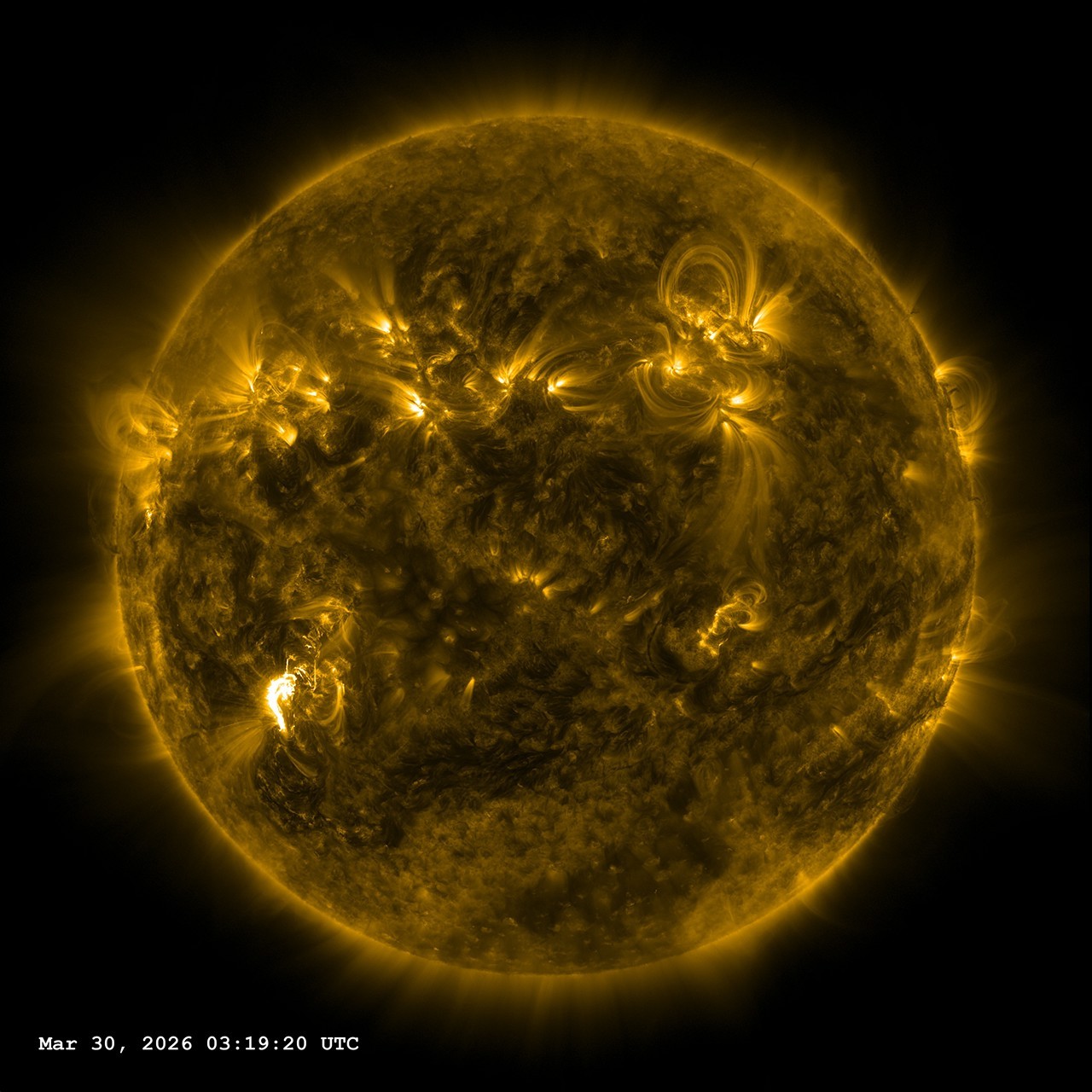

An X1.4 solar flare peaked at 11:19 p.m. EDT on March 29, captured by NASA’s Solar Dynamics Observatory. X-class flares can disrupt radio communications, electric power grids, navigation signals and pose risks to spacecraft and astronauts, though NASA does not expect effects on the Artemis II mission and continues to monitor space weather. Potential operational impacts are sector-specific (communications, utilities, aerospace) rather than broad market-moving events.

This type of transient space-weather event sharpens an underpriced certainty: governments and large network operators will accelerate spending on hardening and redundancy. Expect procurement timelines to compress from multiyear planning into 6–24 month accelerated RFPs for radiation‑hardened components, hardened ground stations, satellite spare-builds, and high-voltage transformer inventories — a multi-decade CAPEX cycle for mission‑critical infrastructure. Near term (days–weeks) the market reaction will be limited and noisy, driven more by headlines than fundamentals; the economically meaningful moves occur in the 3–18 month window as insurers reprice satellite policies and defense primes convert urgency into contracted work. Reinsurers will both raise premiums and tighten coverage clauses, which creates an opportunity for well-capitalized manufacturers to capture higher-margin retrofit and replacement work while smaller operators face liquidity stress if claims or outages occur. Second-order supply‑chain effects: demand will shift toward vendors of radiation-hardened semiconductors, custom power transformers, and hardened electronics test/verification services — a concentrated segment where lead times can double and pricing power emerges. Conversely, highly leveraged smallsat operators and certain satellite-as-a-service models that delayed hedging or lack spare capacity are exposed to cashflow shocks if outages trigger service-level penalties or replacement capex. Tail risk remains low-probability but high-impact: a Carrington‑scale event would create multi‑month economic disruption and force a multi‑year rewrite of grid and space insurance economics. The primary reversal catalyst is improved predictive forecasting and rapid operational mitigations (e.g., power-down procedures, rapid spare deployment), which would compress the expected CAPEX benefit and cap upside for industrial suppliers within 6–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00