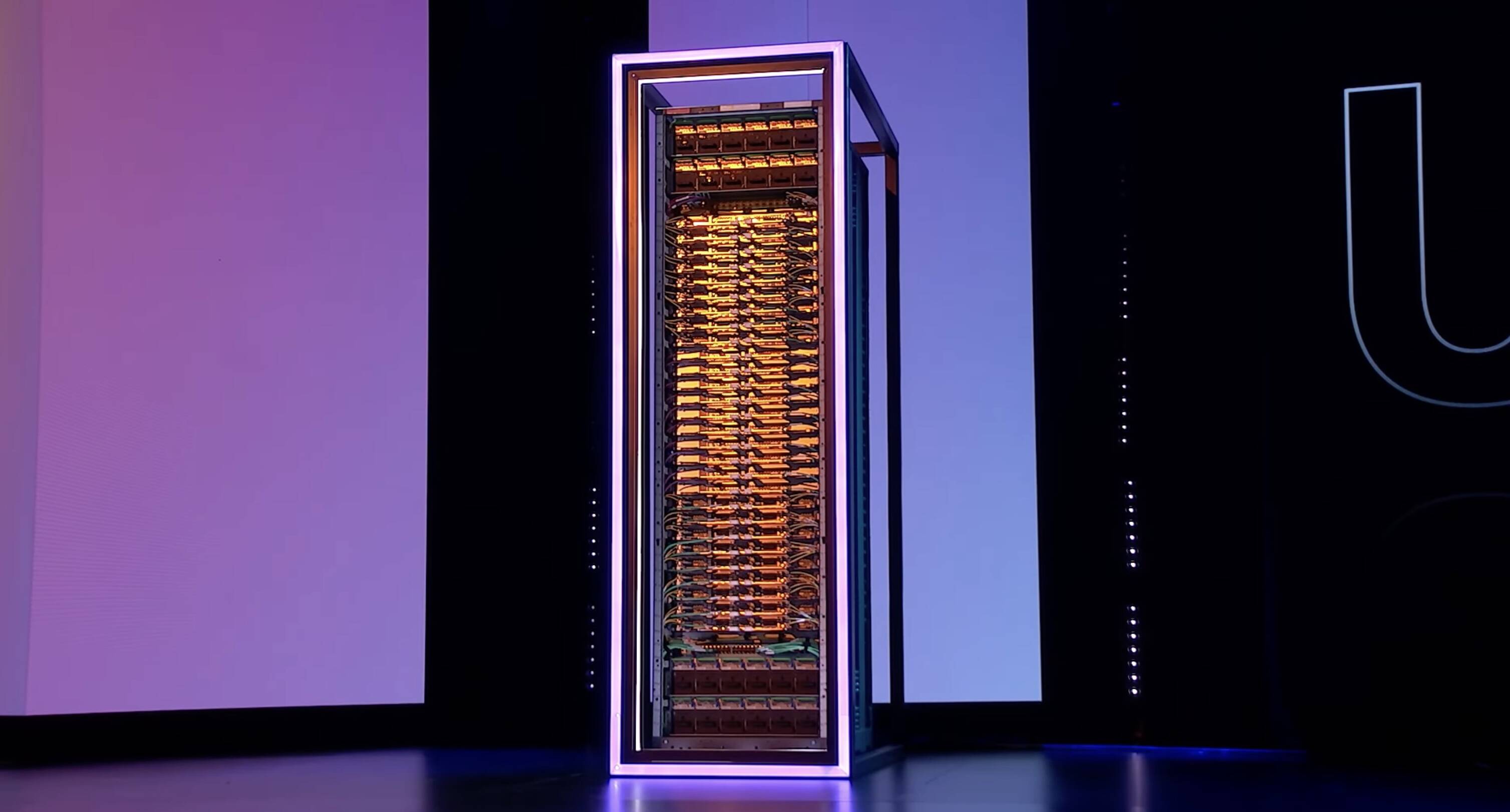

AWS unveiled Trainium3 UltraServer racks that conform architecturally to existing Nvidia and AMD NVL72/Helios designs, using compute blades that pair a Graviton CPU with four Trainium3 accelerators and two Nitro DPUs. Each UltraServer contains 36 blades (144 accelerators) tied together by Amazon's NeuronSwitch (roughly ~20 switches per UltraServer), and AWS plans Trainium4 support for UALink and NVLink Fusion to enable chassis compatibility with Nvidia blades. The announcement signals hyperscalers' move toward standardized, modular rack architectures and switched scale-up fabrics — a structural shift that may streamline supply chains, influence demand for accelerators and interconnects, and heighten competitive dynamics among Amazon, Nvidia, AMD and Google.

Market structure: Hyperscalers (AMZN) and accelerator leaders (NVDA, AMD) are the primary beneficiaries as rack and switch standardization lowers integration cost and speeds deployment; Intel (INTC) is a clear loser as AWS shifts from x86 to Graviton and custom fabrics. Expect NVDA to retain near-term pricing power via software/stack lock‑in and switch/IP revenue, but modular MGX/OCPC-style racks increase substitution risk for individual chip margins over 12–36 months. Risk assessment: Tail risks include an interconnect-scale failure or networking bug causing multi-rack outages (low probability, high impact), accelerated antitrust scrutiny of Nvidia/AWS partnerships within 12–24 months, and supply‑chain shocks (Taiwan/SE Asia) that could spike prices. Immediate (days) impact is minimal; short-term (weeks–months) see order reconfiguration; long-term (2–4 years) could see margin compression if accelerators commoditize and optics adoption changes topologies. Trade implications: Favor pro‑AI infrastructure exposure (NVDA, AMZN, AMD) while underweighting legacy CPU suppliers (INTC) and niche switch vendors susceptible to price competition. Use directional and relative value trades: long NVDA/AWS vs short INTC, and use calibrated option spreads (3–9 month) to express upside with capped cost given elevated IV. Rebalance energy/power exposure modestly upward (utilities/oil +1–2%) to hedge higher datacenter consumption over next 12–24 months. Contrarian angles: Consensus overlooks the acceleration risk of commoditization — modular racks mean customers can swap accelerator vendors faster, pressuring chip ASPs beyond 18 months; conversely, Google's optical/torus approach remains an under‑followed defensive moat at scale. Historical parallel: CPU market share shifts (x86 → ARM) suggest execution and software ecosystems will decide winners, not hardware specs alone.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.12

Ticker Sentiment