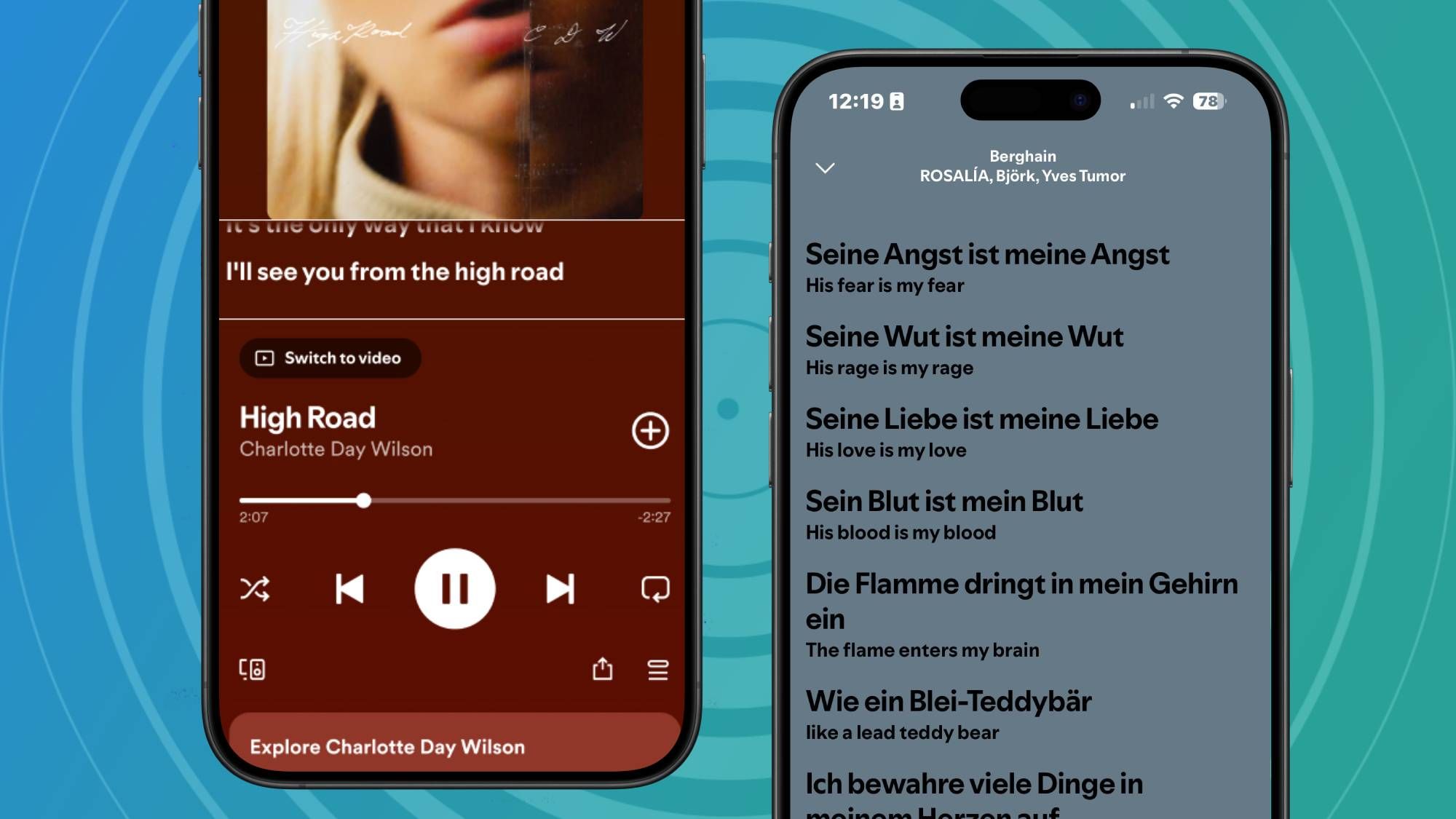

Spotify is launching three upgrades to its Lyrics feature: global Lyric Translations, offline access to Lyrics for Premium subscribers, and a relocated Lyrics tab in the Now Playing view. The enhancements—including a competitive response to Apple Music's translation tool—are aimed at improving user experience and strengthening Premium value proposition, likely supporting engagement and retention but having limited near-term impact on revenue or market valuation.

Market structure: Spotify (SPOT) is the primary beneficiary — translations + offline lyrics reduce friction for non-English catalogs and raise the marginal value of Premium; estimate a realistic engagement uplift of 1–3% and a potential ARPU tailwind of 50–150 bps over 12–24 months. Losers are niche third‑party translation apps and marginal discovery tools; competitive pressure on Apple Music (AAPL) and YouTube Music to match features compresses differentiation but not immediately pricing. Cross‑asset impact is muted: equity vol could tick up around product announcements, fixed income and FX effects are negligible absent larger monetization evidence. Risk assessment: Tail risks include publisher licensing disputes (removal of lyrics or higher royalties) and antitrust scrutiny of bundled features — low probability but high impact (could erase margins >200 bps). Near term (days–weeks) expect sentiment moves only on product rollout metrics; short term (1–3 months) adoption signals matter; long term (4–24 months) cumulative ARPU/retention changes determine revenue. Hidden dependencies: feature benefit depends on accurate sync/translation quality and publisher contracts; aggressive responses from Apple/Google could shorten Spotify’s commercialization window. Trade implications: Tactical long SPOT exposure is justified but size conservatively (2–3% NAV) while monitoring MAU/ARPU prints; implement a directional options hedge — buy a 3–6 month call spread (≈15–25% OTM buy, 35–45% OTM sell) sized to 0.5–1% NAV to cap cost. Relative trade: long SPOT vs short AAPL (smaller notional on AAPL) for 3–6 months captures product-cycle alpha; exit triggers: MAU growth <+0.5% QoQ or gross margin contraction >100 bps. Sector tilt: modestly overweight Media & Entertainment (+1–2% tactical) funded from ad‑heavy digital names. Contrarian angle: The market underestimates the monetization runway of non‑English catalogs — translations may incrementally raise conversion in LATAM/EU by 0.5–1.5% annualized, creating a 3–12% upside to SPOT revenue over 12–24 months if retention improves. Conversely, upside is likely concentrated in a 3–6 month window before competitors copy, so timing matters; history (podcast push) shows feature rollouts often produce hype but limited durable margin expansion unless paired with pricing or large content wins. Unintended consequence: higher support/licensing costs could offset early gains — watch publisher disputes and cost of goods sold trends.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment