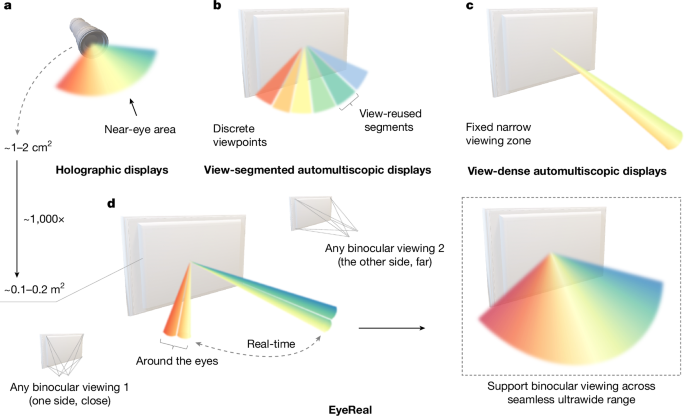

EyeReal, a deep-learning-driven autostereoscopic display prototype, dynamically optimizes limited optical space–bandwidth product to deliver glasses-free full-parallax 3D with seamless viewing beyond 100°, real-time light-field synthesis at over 50 Hz and 1,920×1,080 resolution using consumer-grade multilayer LCD stacks. The system eliminates the need for specialized optics, runs inference on an NVIDIA RTX 4090 (training used 32 A800 GPUs), and uses a three-layer LCD prototype—suggesting a lower-cost, scalable route to wide-angle 3D for applications in entertainment, education and industrial design that could influence demand for display panels and GPU compute in downstream commercialization scenarios.

Market structure: EyeReal’s software-heavy path removes a hardware moat and shifts value to GPUs/AI stacks, panel OEMs able to supply multilayer LCDs and content toolchains. Expect winners: NVIDIA (NVDA) for training/inference demand and panelmakers (BOE, LG Display) for multi-layer orders; losers: niche near‑eye AR headset makers if glasses‑free adoption accelerates. If adoption scales, compute demand could add low-single-digit percent to NVDA GPU cycles within 12–24 months and increase panel ASPs modestly as multilayerisation premiums appear. Risk assessment: Tail risks include export controls on high-end inference chips, failed consumer adoption (VAC/IPD complaints), patent litigation and component shortages; any could negate demand and depress supplier margins. Time horizons: immediate (days/weeks) — PR-driven sentiment swings; short-term (3–6 months) — pilot OEM deals and prototype orders; long-term (12–36 months) — commercial deployments and content ecosystem development. Hidden dependencies: reliance on high‑throughput GPUs, RGB‑D camera tracking, and calibrated supply chains; a bottleneck in any node amplifies downside. Trade implications: Direct play — overweight NVDA (tactical 1–2% position) and selective display OEMs; modest long on ADBE (0.5–1%) for content tooling adoption over 6–18 months; keep MSFT neutral-to-long (0.5%) for cloud GPU exposure if Azure GPU inventory tightens. Options — buy 3–6 month NVDA call spreads sized to 1% notional (capped risk), hedge with out‑of‑the‑money puts if catalyst timelines extend. Rotate into semiconductors and display supply chain on confirmed OEM purchase orders; underweight pure XR headset hardware names until multi‑user scaling is proven. Contrarian angles: Consensus (hype around instant mass adoption) likely overestimates consumer pace — multi‑user, time‑multiplex scaling and color/brightness tradeoffs could delay revenues 12–24 months. Conversely, the market may underprice NVDA’s capture of low‑latency inference demand; if OEM pilots convert to orders within 6 months, NVDA upside can exceed 20–30% from current levels. Historical parallel: AI-driven hardware cycles (2016–2021) show steep early adoption of GPUs followed by commoditization; monitor OEM order flow and patent/standard announcements as primary over/under‑reaction signals.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment