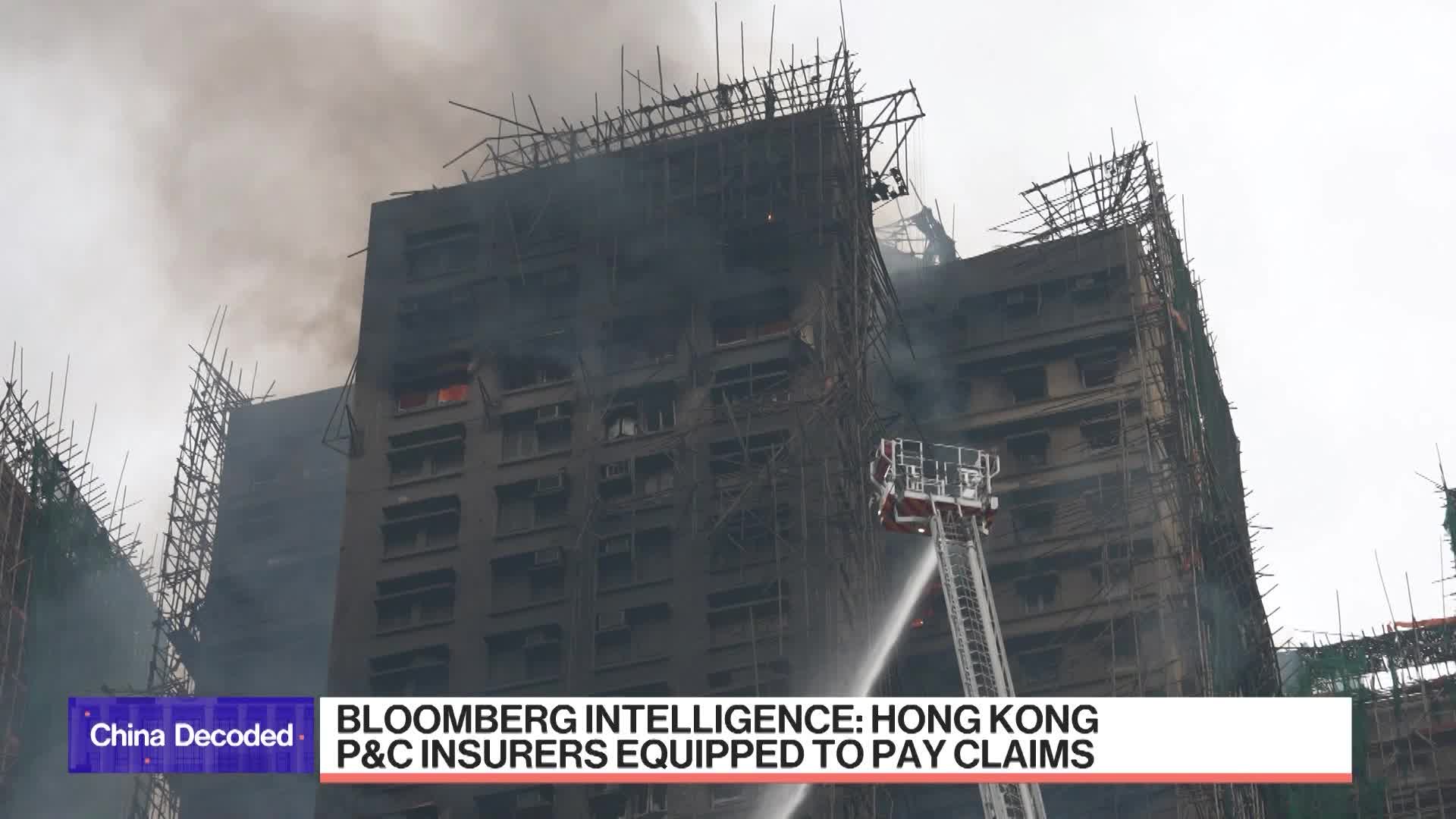

A large residential fire in Hong Kong is expected to generate substantial insurance claims, with quoted coverage figures around HKD 2.6 billion for building/contractor policies and roughly HKD 2.0 billion under property all-risks. The primary insurer is a long-established, state-owned underwriter and significant portions of exposure are expected to be ceded to reinsurance panels, spreading losses across the global insurance market; however, liability allocation, third-party, employee compensation and life-claim complexity mean a lengthy claims process. Low penetration of standalone home-contents insurance (<20%) and modest death-benefit profiles on common savings-linked life policies limit direct payouts to residents, while banks' mortgage-required fire insurance should mitigate lender credit exposure—nonetheless hedge funds should monitor insurer and reinsurer balance sheets and potential legal disputes around liability.

Market structure: Losses are concentrated (media/BI cites ~HKD 2.6bn total coverage and ~HKD 2bn in property-all-risk) so primary insurers and their reinsurance panels will bear most cashflow impact. Winners: global reinsurers and specialty brokers if treaty renewals harden; losers: Hong Kong-focused P&C carriers, small-cap insurers and owners of older residential blocks that face retrofit/liability costs. Pricing power will likely shift toward reinsurers in the next 6–12 months as loss experience is priced into renewals. Risk assessment: Tail events include a large court finding of contractor negligence that expands third‑party liability beyond policy limits or a regulator-mandated retrofit program (>HKD 5–10bn political risk) forcing accelerated capital spend. Immediate timeline (days–weeks): claims triage and priority payouts; short-term (1–3 months): reserve adjustments and loss notices; medium-term (6–18 months): treaty renewals and rate-card repricing. Hidden dependency: low home-contents penetration (<20%) amplifies social/political pressure and could lead to faster government intervention. Trade implications: Favor reinsurer exposure and short/hedge concentrated Hong Kong P&C positions. Expect reinsurance pricing to rise 5–15% at next renewals (6–12 months), creating asymmetric upside for reinsurer equities and equity-like instruments; conversely, Hong Kong REITs and small insurers face potential 5–20% hit to NAV/earnings depending on mandated capex. Use options to buy convexity around volatility spikes and size positions modestly (1–3% of portfolio) given event concentration. Contrarian angles: Consensus underestimates the regulatory/corporate-governance reaction in Hong Kong — if authorities force blanket safety retrofits, that creates a multi‑year revenue tailwind for reinsurers and engineering/retrofit contractors while compressing returns for property owners. The market may be underpricing a short-term reputational shock to large regional insurers (AIA/2318/1299) even if direct cash losses are modest; monitor 30–90 day legal filings as catalysts for re-rating.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.42