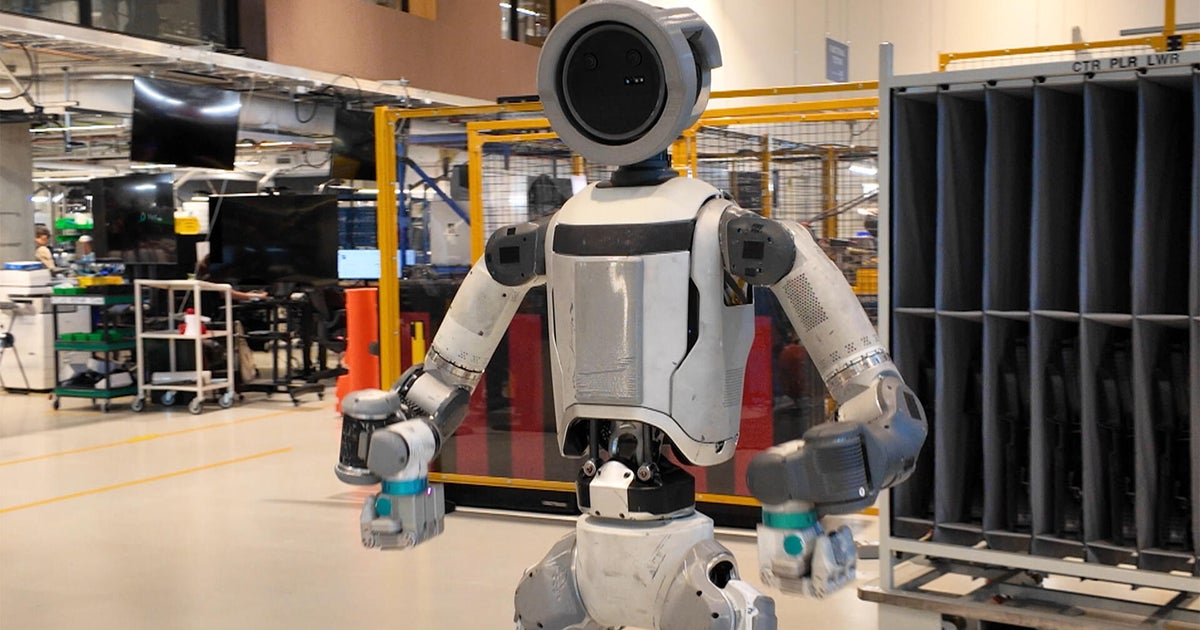

Boston Dynamics has significantly upgraded its Atlas humanoid with greater range of motion, three‑digit tactile hands, continuous-rotation joints and an AI control stack powered by Nvidia chips that can be trained via teleoperation for manipulation tasks. Company engineers demonstrated advanced behaviors (cartwheels, fluid running, self-righting) while executives cautioned that broad deployment hinges on improving reliability and affordability, tempering current market hype about near-term mass adoption. Investors should view this as technical progress that benefits robotics and AI supply chains but not yet a near-term revenue or market-impact catalyst.

Market structure: The immediate winners are AI compute suppliers (NVDA) and specialist robotics hardware/vision suppliers (Cognex, ABB, FANUC/KUKA equivalents) as humanoid prototypes require high-end GPUs, advanced actuators and tactile sensors; I estimate incremental GPU demand could lift NVDA datacenter revenue by low-single-digit percentage points within 12–24 months if pilot programs scale, with multi-year upside if deployments reach tens of thousands. Losers: low-margin systems integrators and staffing-heavy logistics providers face margin pressure as capital substitution accelerates; pricing power shifts to platform/semi providers and specialized component makers, not generalist integrators. Risk assessment: Short-term (days–weeks) risks center on sentiment swings (NVDA earnings, export-control headlines) and 6–12 month tail risks include chip export restrictions, high-profile liability incidents or OSH/regulatory clampdowns that could delay commercial rollouts. Hidden dependencies include supply of HBM memory, rare-earth magnets and teleoperation labor pools; catalysts that accelerate adoption are commercial fleet orders, NVDA robotics SDK launches or defense contracts — negative catalysts are China restrictions or GPU supply shocks. Trade implications: Direct: overweight NVDA and SOXX (semis) and a small allocation to robotics ETFs (IRBO/BOTZ) for 6–18 months; consider long Cognex (CGNX) for vision-sensor exposure. Pair trade: long CGNX (1–2% portfolio) / short Rockwell Automation (ROK) (1%) to express vision-sensor vs legacy PLC exposure. Options: buy 9–15 month NVDA call spreads (debit) 25–40% OTM to cap cost; use 1–3% notional and scale on 5–10% pullbacks. Contrarian angles: Consensus overestimates near-term unit volumes — humanoids scaling to millions is decades away, so valuations that price rapid mass deployment are likely stretched. Conversely, consensus underestimates the recurring-service revenue (software, teleoperation) capture by NVDA-like platform providers; watch for early SaaS-style contracts (signed multi-year agreements) as true valuation inflection — absence of such contracts in 12 months suggests a re-rate downward.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.12

Ticker Sentiment