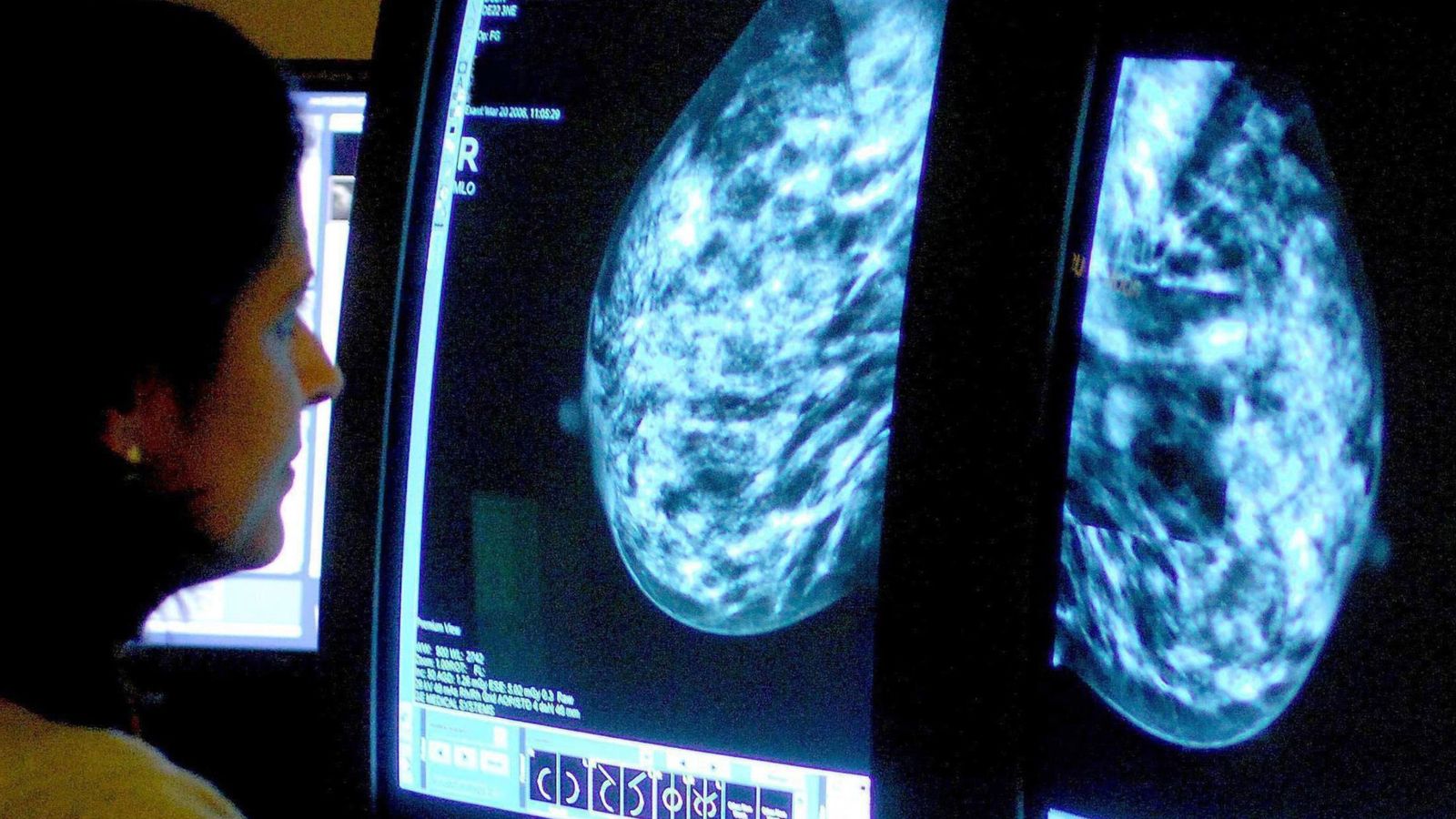

A randomized controlled trial of more than 100,000 Swedish women found AI-assisted mammography — trained on over 200,000 exams from 10+ countries — reduced interval cancers by 12% (1.55 vs 1.76 per 1,000) and increased the share of cancers detected at screening to 81% versus 74% for standard double reading, with similar false‑positive rates (1.5% vs 1.4%). Published in The Lancet, the 2021–22 study suggests AI could improve early detection of clinically relevant breast cancers and reduce advanced disease while potentially easing radiologist workload, though authors stress cautious, monitored implementation across screening programmes.

Market structure: Winners are specialized medical‑imaging AI vendors and incumbents that can bundle software with hardware (HOLX, GE, PHG) plus cloud providers (MSFT, AMZN, GOOGL) that supply training/hosting; payors and large IDNs gain bargaining power as AI reduces interval cancers (trial: 12% fewer). Losers are niche manual‑reading workflows and some radiology staffing providers if adoption accelerates, pressuring per‑read pricing; hospitals face CAPEX for software integration but offset by potential downstream cost savings. Supply/demand: expect sharp near‑term demand for software licenses and integration services, steady demand for hardware upgrades over 12–24 months, and higher cloud compute spend concentrated at a few hyperscalers. Risk assessment: Key tail risks are regulatory reversals (FDA/EMA restrictions), high‑profile model failures or malpractice suits, and reimbursement denial; any of these could wipe out >50% of small AI vendor valuations quickly. Time horizons: immediate (days–weeks) = knee‑jerk moves on regulatory headlines; short (3–12 months) = procurement cycles, pilot rollouts and reimbursement decisions; long (1–3 years) = consolidation and margin capture. Hidden dependencies include data access for retraining (local population drift) and hospital IT upgrade budgets. Trade implications: Direct plays: overweight HOLX (2–3% portfolio) for hardware+software cross‑sell and buy 9–12 month call spreads on MSFT (1% notional) for cloud/Nuance upside. Speculative: small position in ICAD (ICAD) or similar AI pure‑plays via 6–9 month call spreads (0.5–1%) funded by a 1% short in radiology staffing AMN to hedge labor displacement risk. Use tight stops (15%) and scale up if CMS issues a reimbursement code within 3–6 months. Contrarian angles: Consensus underestimates integration friction—histor CAD cycles (2000s) show clinical validation alone doesn’t equal rapid monetization; incumbents may acquire winners, compressing public small‑cap upside. Overreaction is possible: expect volatility around FDA/CMS news; if reimbursement lags >12 months, small AI vendors could be materially overvalued while hardware/cloud names hold steady.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28