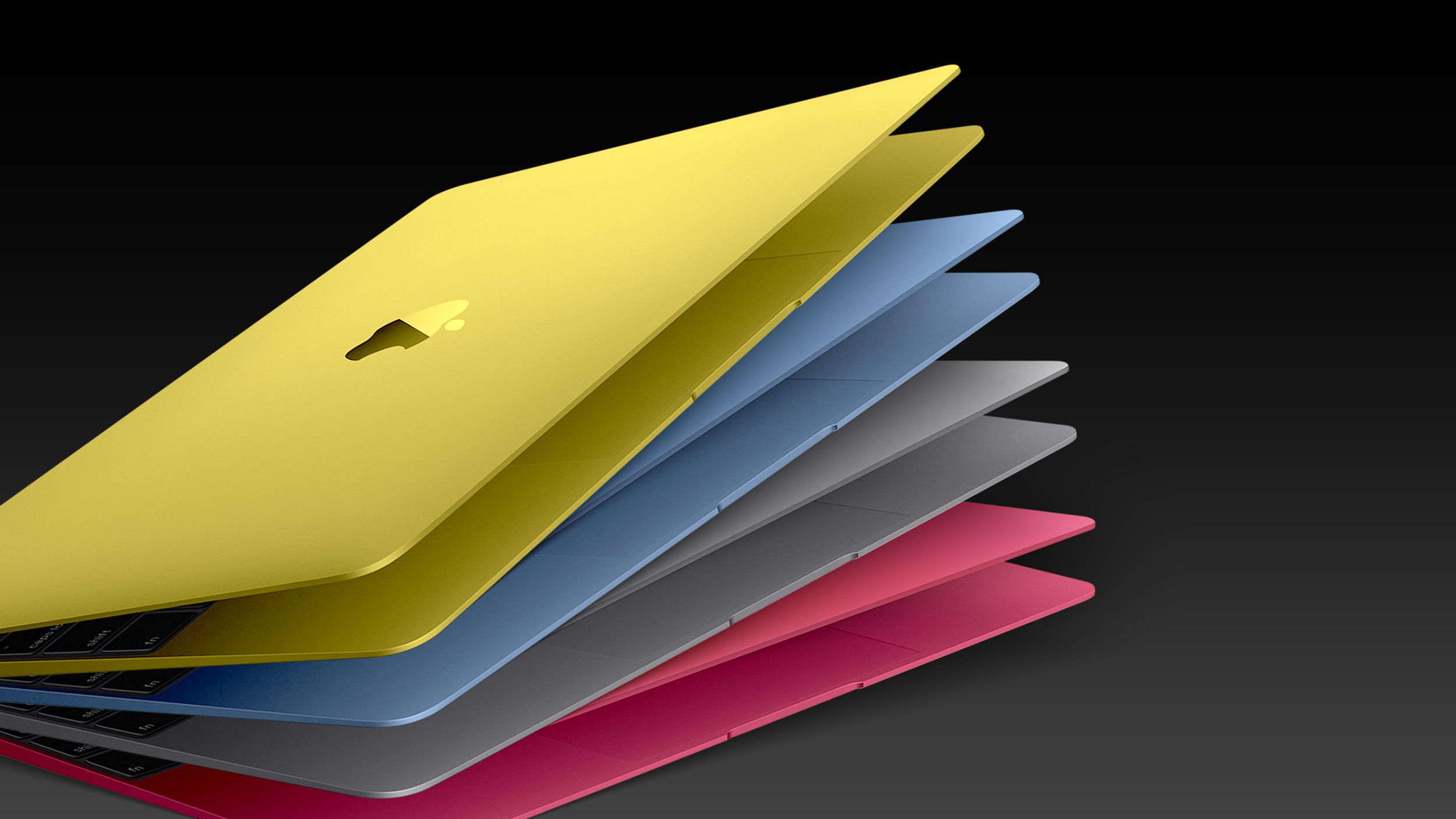

Apple is expected to unveil a rumored low-cost MacBook at its March 4, 2026 event, reportedly featuring a 12.9-inch display, aluminum chassis, multiple bold color finishes, and an iPhone-derived A18 Pro chip instead of an M-series processor, with pricing likely well below $1,000. If confirmed, the product would expand Apple's addressable laptop market and echo its entry-level iPad strategy, with implications for average selling prices, gross margins and competitor pricing dynamics; investors should monitor confirmation, expected specs, and supply-chain signals ahead of the launch.

Market structure: A low-cost, colorful MacBook priced well below $1,000 expands Apple’s TAM in education and first-time laptop buyers and directly benefits AAPL (higher unit volumes), TSM (A18 Pro wafer demand), and retailers like AAPL stores/BestBuy. Losers: low-cost Windows OEMs (HPQ, DELL) and Chromebook makers will face pricing pressure and potential share loss; Apple’s pricing power shifts toward volume-driven device attach for services rather than per-device ASPs. Cross-asset: expect a modest IV lift in AAPL options into Mar 4, small risk-on bid in equities and USD, negligible bond impact; aluminum/extrusion suppliers could see a +1-3% order bump within a quarter. Risk assessment: Tail risks include product performance shortfall vs M-series (bad reviews), A18 supply prioritized to iPhone creating insufficient initial Mac supply, or margin compression if BOM rises — each could trigger >10% downside in AAPL over 3 months. Time horizons: immediate (days) = IV/event risk; short-term (weeks) = sell-through and initial SKU availability; long-term (quarters) = unit share, services attach, and margin mix. Hidden dependencies: SoC allocation (TSM capacity) and retail channel inventory management; catalysts are March 4 reviews, 2-week preorder data, and Apple’s next earnings guide. Trade implications: Direct: modest tactical long AAPL equity (2–3% portfolio) ahead of Mar 4 to capture positive surprise, with 6% stop and 8–12% 3-month target; buy Apr 2026 0.30–0.40 delta call debit spreads sized 1% notional to limit downside. Relative value: long AAPL / short HPQ or DELL (market-value neutral, 1–2% net exposure) for 3–6 months to exploit share shift. Supplier play: add 1–2% long TSM on confirmation of A18 use, 6–12 month horizon, target +10–20%. Contrarian angles: Consensus emphasizes a clean win — underappreciated risks include brand dilution and cannibalization of higher-margin MacBook Air, which could mute EPS upside; historical parallel: colorful iBook-era novelty didn’t sustain enterprise demand. If AAPL rallies >6% intraday on the announcement, that may be an overdone move; use that as a systematic profit-taking signal to reduce exposure by half and reassess sell-through metrics over 2–4 weeks.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28

Ticker Sentiment