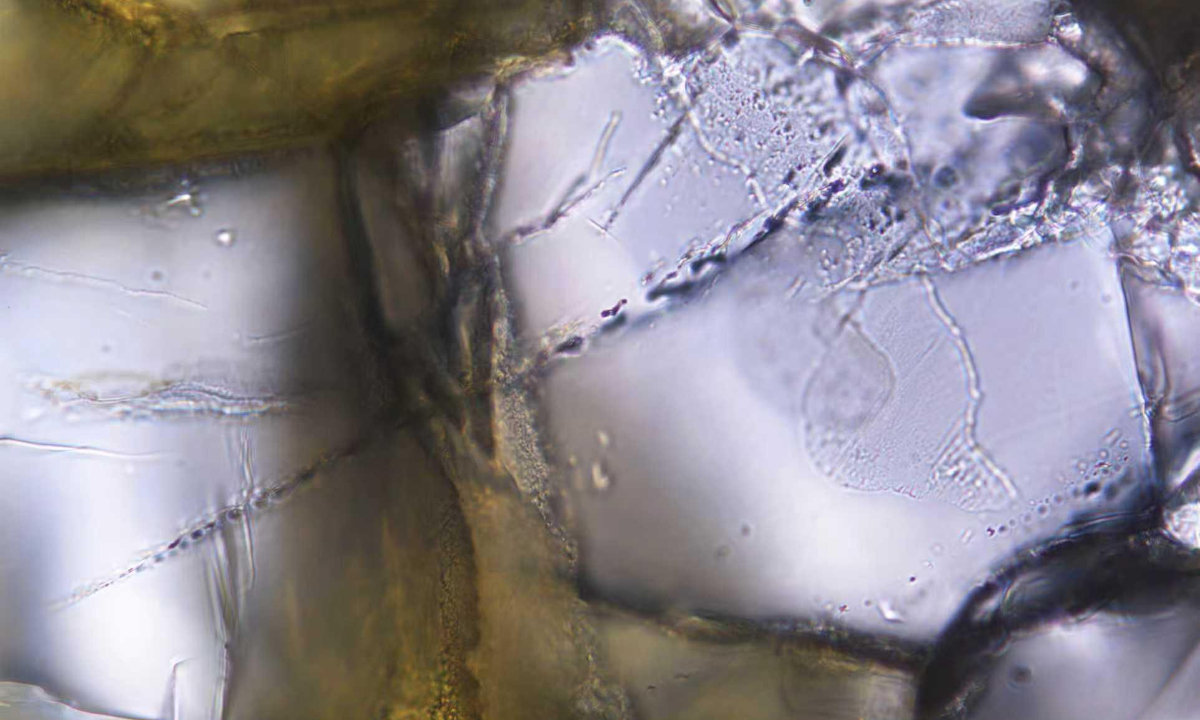

Chinese researchers reported discovery of micrometer-scale fluid inclusions containing natural hydrogen and methane within ophiolites on the Qinghai-Xizang Plateau, linked to serpentinization reactions and suggesting active or past deep hydrogen generation. The team argues the plateau's extensive ophiolite complexes are prime targets for natural-hydrogen exploration, offering a potential low-cost, zero-carbon energy source that could support China’s energy security and green-transition strategies, though commercial viability and timing remain uncertain and will require further exploration and resource assessment.

Market structure: Discovery of natural H2 in Qinghai-Xizang is an early-stage supply shock potential, not immediate commodity displacement. Winners are industrial gas suppliers (Linde/LIN, Air Products/APD) and drill/service firms that can adapt to subsurface H2 extraction; losers are marginal electrolyzer pure-plays if cheap geologic H2 reduces short-term demand for green H2. Expect gradual price pressure on electrolytic H2 margins over 2–5 years if commercial flows scale above ~10–50 ktH2/year regionally; near-term market share shifts will be small. Risk assessment: Tail risks include Chinese regulatory classification that either designates natural H2 as strategic (positive, accelerates capex) or restricts extraction (negative), and technical/operational risk that H2 fluxes are too diffuse to commercialize (<100 t/year per field). Time horizons: immediate (days) – negligible market moves; short-term (3–12 months) – exploration/permit news and R&D reports drive volatility; long-term (2–7 years) – potential material supply if multiple ophiolite provinces prove economic. Hidden dependency: realization requires pipelines, compression, storage and safety standards; those capex needs create bottlenecks and winners among engineering firms. Trade implications: Tactical relative-value opportunity is to overweight industrial gas majors (LIN, APD) via 12–24 month LEAPS while underweight speculative electrolyzer/hydrogen-tech names (PLUG, FCEL) via short call spreads. Use options to express limited risk: buy 18–30 month 15–20% OTM calls on LIN/APD sized 2–3% portfolio each, and sell 3–9 month call spreads on PLUG sized 1–2% to collect premium. Rotate from coal exposure (KOL) into industrial gas over 6–24 months if China confirms resource classification. Contrarian angles: Consensus may assume rapid commercialization; that underestimates infrastructure and economics – geological H2 is low-density and site-specific, so many announced plays will fail. Historical parallel: early shale gas optimism (2008–2012) required years and infrastructure before price effects; natural H2 may mirror a long discovery-to-production timeline, creating opportunities to short hype in small-cap explorers and long established gas/infrastructure names with balance-sheet capacity. Watch for unintended consequence: cheap natural H2 could delay green-electrolyzer subsidies, reshaping policy risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25