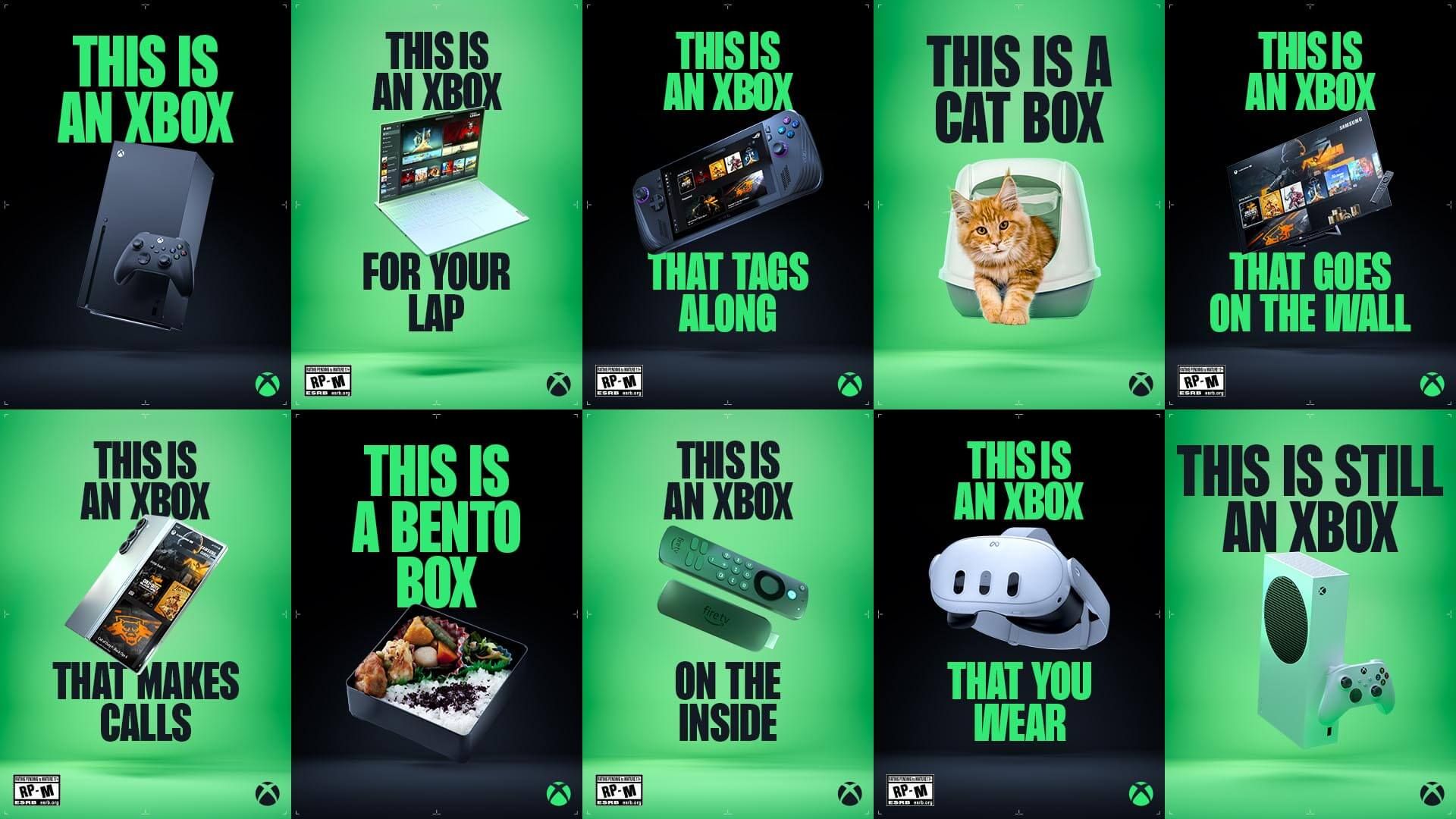

Asha Sharma (new head of Microsoft Gaming) personally axed the controversial "This is an Xbox" marketing campaign and is leading an internal brand reset emphasizing a return to consoles and hardware, with focus on Project Helix (a PC-console hybrid). Xbox hardware performance has lagged—fewer Xbox Series consoles have shipped than Xbox One at the same lifecycle point—and the backlash to the campaign creates reputational headwinds, though this is unlikely to materially move Microsoft’s broader financials near term.

The market reaction to Xbox’s brand reset creates a narrow but persistent bifurcation: hardware-differentiation narratives lift console-first incumbents while eroding the perceived marginal utility of platform-agnostic subscription plays. A 100–200bp swing in consumer preference toward a hardware-led proposition would do outsized work on lifetime monetization — console buyers generate higher attach rates and accessory/service spend for multiple years versus ephemeral streaming/port-access revenue. That dynamic magnifies small share shifts into multi-year revenue streams for the winner.

Second-order supply-chain effects are underappreciated and measurable within two to four production cycles. A renewed focus on “proud hardware” increases demand elasticity for higher-end SoCs, discrete GPUs, DRAM and NVMe, tightening supply for mid-cycle PC OEMs and raising bargaining power for AMD/NVIDIA/TSMC and contract manufacturers; conversely, cloud-only or storefront-agnostic strategies reduce captive accessory and retail economics, pressuring third-party peripheral vendors. Expect visible inventory and price signaling in component orders within 3–9 months as manufacturing lead times and BOM choices are finalized.

For investors, the path to capture this re-pricing runs through platform-specific revenue multipliers and supplier exposure rather than broad software multiples. Near-term volatility will hinge on forthcoming product disclosures and holiday sell-through data; medium-term (6–18 months) earnings revisions will reveal whether consumer spending is truly rotating back toward boxed hardware or remaining service-first. Watch developer licensing concessions and third-party storefront integration as catalysts that can rapidly reframe value capture across ecosystems.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

-0.05

Ticker Sentiment