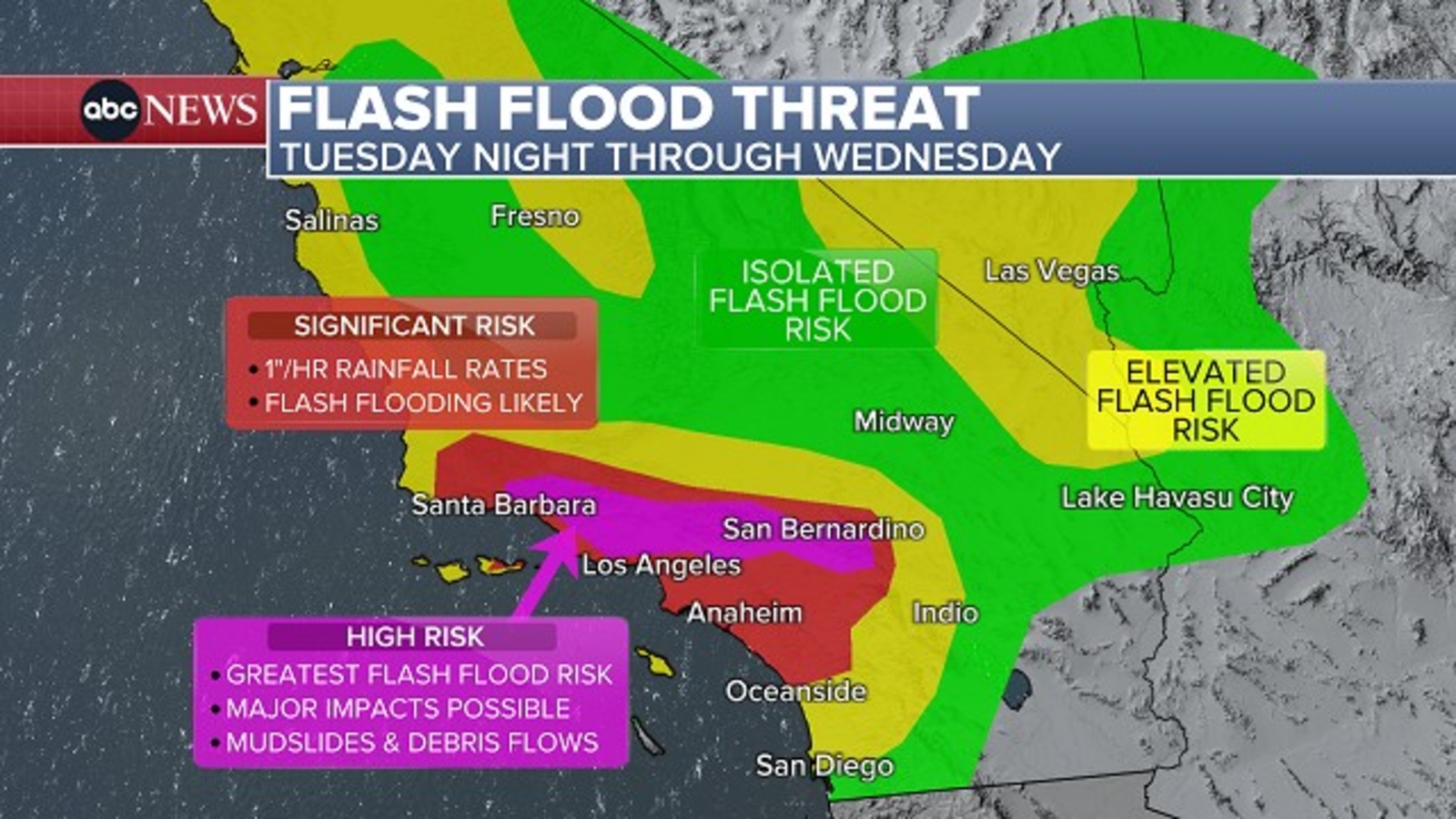

The National Weather Service upgraded parts of Southern California to a rare "high risk" (level 4/4) for excessive rainfall and life‑threatening flash flooding on Christmas Eve, with the greatest threat concentrated over wildfire burn scars and increased potential for mudslides and debris flows. The advisory covers portions of Los Angeles, Ventura and San Bernardino counties — including Burbank, Altadena, Glendale, San Bernardino, Santa Clarita and Thousand Oaks — and notes that such high‑risk designations are issued on roughly 4% of days but account for a disproportionate share of flood fatalities and damages. Market-relevant implications are primarily local and operational: heightened near-term risk of property damage and insurance claims, plus potential disruptions to transportation, logistics and regional infrastructure that could affect real‑estate exposure and insurer loss estimates.

Market structure: Immediate winners are remediation/repair chains (Home Depot HD, Fastenal FAST), heavy-equipment suppliers (Caterpillar CAT) and short-haul trucking; losers are local residential RE (CA-focused builders like KBH) and property insurers with concentrated Southern California exposure. Shipping and logistics hubs (LA/Long Beach ports) will see supply re-routing for days–weeks, raising West-Coast inland trucking/warehousing rates by an estimated 5–15% during disruptions and pressuring retail inventory flows into Q1. Risk assessment: Tail risks include a multi-burn-scar mudslide causing >$1B insured losses and a state emergency declaration that triggers large FEMA payouts and regulatory scrutiny of insurer rate filings; such an event could widen P/C spreads and depress regional property values by 5–15% locally over 6–12 months. Near-term (days) cadence is logistics disruption and surge in remediation spend; medium-term (weeks–months) is insurance claims/earnings hits; long-term (quarters–years) is higher insurance premiums and increased public infrastructure spend. Trade implications: Tactical plays include short-dated puts on CA-heavy insurers (45–60 day put spreads) to capture immediate claim risk, and 1–3 month longs in HD/CAT and remediation contractors for pick-up in retrofit/cleanup demand (estimate incremental revenue +2–6% in next quarter). Pair trades: short KBH vs long LEN/DHI to express regional weakness; optional strategies: buy 3–6 month calls on CAT/HD or buy reinsurance names (RE, RNR) on a 6–12 month horizon to capture premium repricing. Contrarian angles: Consensus focuses on insurer pain; the market may underprice remediation/DIY spend lift and infrastructure contractors who can see 10–25% margin tailwinds regionally — HD and CAT could outperform in 3 months. Conversely, insurance stocks could be oversold if FEMA/state reimbursements blunt insured losses; avoid sized directional shorts >1% portfolio without monitoring CA Dept. of Insurance rate filings and first-wave claims (48–72 hours). Historical parallels (CA storms 2017–2019) show 60–120 day earnings impacts but positive 6–12 month demand for construction materials and resilience projects.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25