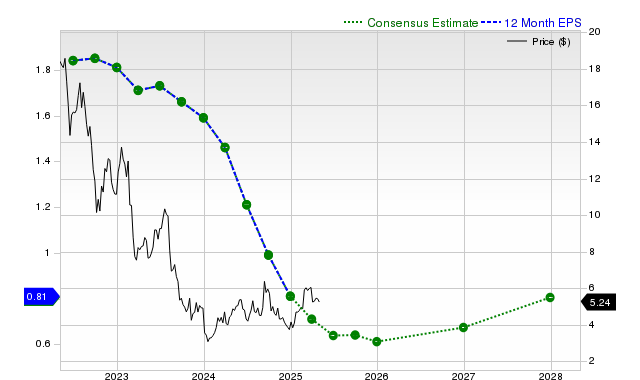

Medical Properties Trust (MPW) shares have significantly underperformed recently, returning -4.4% over the past month compared to the S&P 500's +4.6%. The healthcare REIT faces substantial negative earnings estimate revisions, with current quarter EPS projected to decline 43.5% year-over-year to $0.13 and current fiscal year EPS down 31.3% to $0.55, following recent misses on revenue and EPS. Consequently, Zacks has assigned MPW a Rank #4 (Sell), indicating potential near-term underperformance, despite a projected 12% revenue increase for the next fiscal year.

Medical Properties Trust (MPW) is facing significant fundamental headwinds, reflected in its recent stock underperformance of -4.4% over the last month against a +4.6% gain for the S&P 500 composite. The primary driver of this negative sentiment is the sharp deterioration in earnings expectations. For the current quarter, consensus EPS is projected to decline 43.5% year-over-year to $0.13, while the full-year estimate of $0.55 represents a 31.3% drop from the prior year. These forecasts have been subject to recent downward revisions, with the current quarter and full-year estimates being cut by 4.1% and 2.4% respectively over the last 30 days. This trend is reinforced by the company's last reported quarter, where it missed consensus estimates for both revenue (-5.1%) and EPS (-6.67%), posting a 17.5% year-over-year revenue decline. While analysts forecast a rebound next fiscal year with 12% revenue growth and 23.2% EPS growth, confidence appears shaky as even that forward estimate has been revised downward by 2.9% recently. The stock's valuation, graded 'C' by Zacks, indicates it is trading at par with its peers, offering no apparent discount to compensate for the near-term operational challenges and negative analyst revisions, culminating in a Zacks Rank #4 (Sell).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.65

Ticker Sentiment