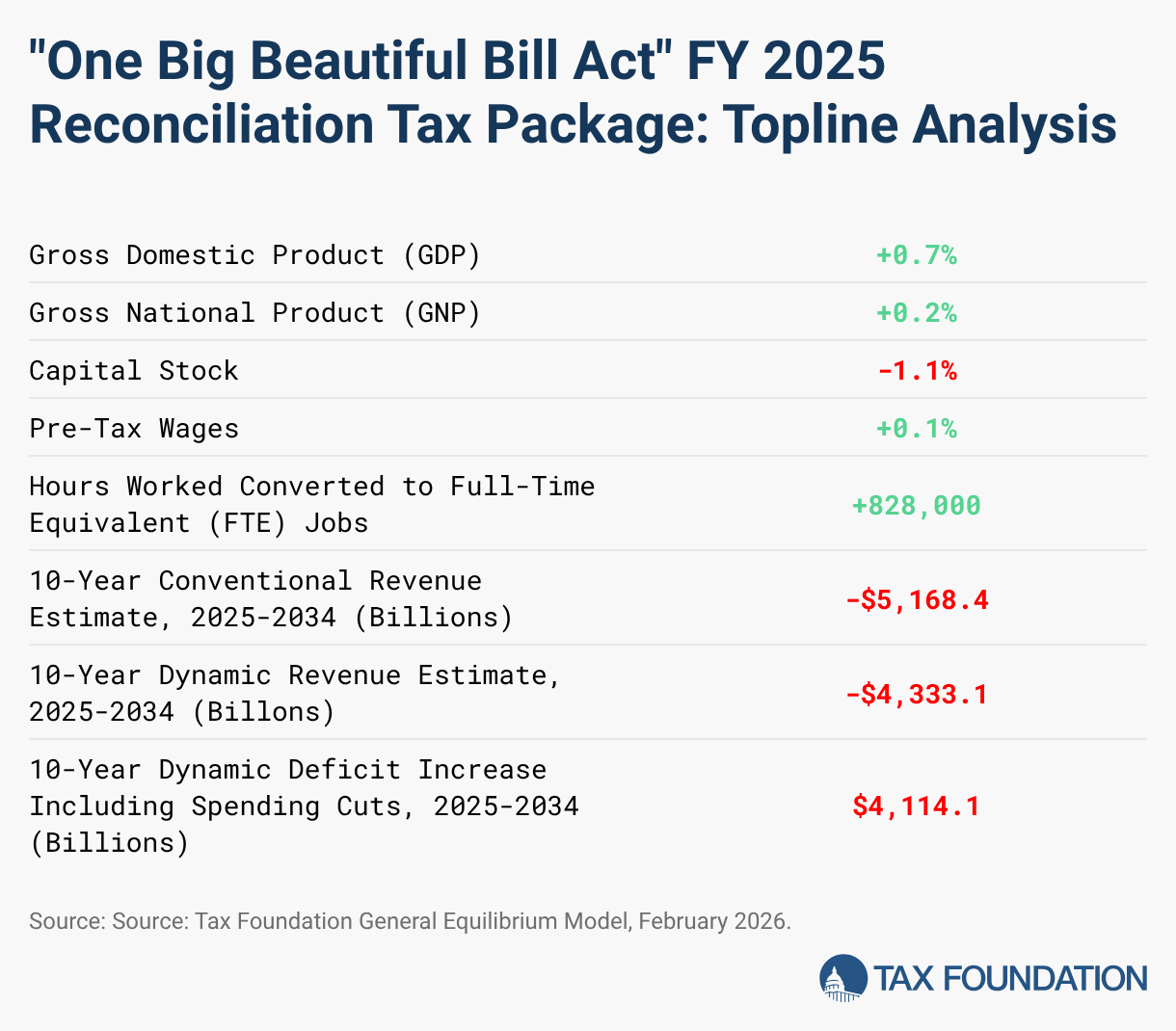

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, makes permanent key pro-growth tax provisions like 100% bonus depreciation and R&D expensing, alongside extending most 2017 TCJA tax cuts, which is projected to increase long-run GDP by 1.2% and raise after-tax incomes. However, the legislation is estimated to add $3 trillion to the deficit over the next decade, introduces complexity through various temporary deductions, and significantly phases out many green energy tax credits. Critically, existing and scheduled tariffs threaten to offset much of OBBBA's economic benefits, potentially reducing net long-run GDP growth to 0.4% and failing to cover the bill's cost, raising concerns about its overall fiscal and economic impact.

The One Big Beautiful Bill Act (OBBBA) institutes a significant fiscal stimulus by making key provisions of the 2017 Tax Cuts and Jobs Act (TCJA) permanent, most notably for businesses through 100% bonus depreciation for short-lived assets and immediate expensing for domestic R&D. These pro-growth policies are projected to expand long-run GDP by 1.2% and increase after-tax incomes by an average of 2.9% in 2026. However, this growth comes at a substantial fiscal cost, with the law estimated to increase the national deficit by $3 trillion over the next decade on a dynamic basis. The legislation introduces a mix of permanent and temporary measures; while permanence for TCJA provisions provides certainty, temporary deductions for tips, overtime, and auto loans (expiring in 2028) create future policy uncertainty and obscure the true long-term fiscal impact. A major policy reversal is the accelerated phaseout and repeal of many Inflation Reduction Act (IRA) green energy tax credits, a significant headwind for that sector. Critically, the economic benefits are significantly threatened by concurrent tariff policies, which are estimated to reduce long-run GDP by 0.8%, offsetting two-thirds of the gains from the tax cuts and leaving a net GDP boost of only 0.4%. This combination of expansionary fiscal policy and restrictive trade policy creates a conflicting economic signal, with distributional analysis showing that by 2034, the lowest income quintile could see after-tax income fall by 0.4% on a conventional basis.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

-0.15