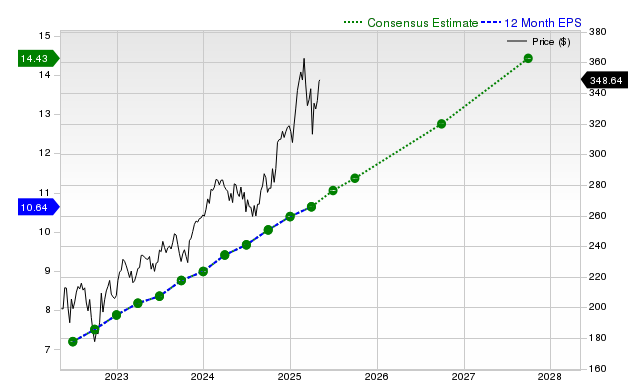

Visa (V) has recently underperformed the S&P 500, declining 2.2% over the past month, yet fundamental analysis suggests a positive outlook. The payments processor is projected to achieve strong earnings growth, with current quarter EPS estimated at $2.84 (+17.4% YoY) and full-year EPS at $11.35 (+12.9% YoY), alongside robust revenue growth forecasts. Visa has consistently beaten consensus earnings estimates, contributing to its Zacks Rank #2 (Buy), which indicates potential near-term market outperformance despite its current valuation suggesting it trades at a premium to peers.

Despite Visa's recent stock underperformance, evidenced by a 2.2% decline over the past month against the S&P 500's 5.2% gain, the company's fundamental outlook remains robust. Analyst consensus points to significant earnings growth, with a projected 17.4% year-over-year increase in EPS for the current quarter and a 12.9% increase for the current fiscal year. This earnings momentum is supported by strong top-line forecasts, including a 10.7% YoY revenue growth expectation for the current quarter. Visa has a consistent track record of operational outperformance, having beaten consensus EPS estimates in each of the last four quarters and revenue estimates in three of those periods. However, this positive fundamental picture is tempered by valuation concerns; the stock receives a 'D' grade for value from Zacks, indicating it trades at a premium to its peers. The Zacks Rank #2 (Buy) suggests that positive earnings estimate revisions may drive near-term outperformance, presenting a classic growth-versus-value scenario for investors to evaluate.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.50

Ticker Sentiment