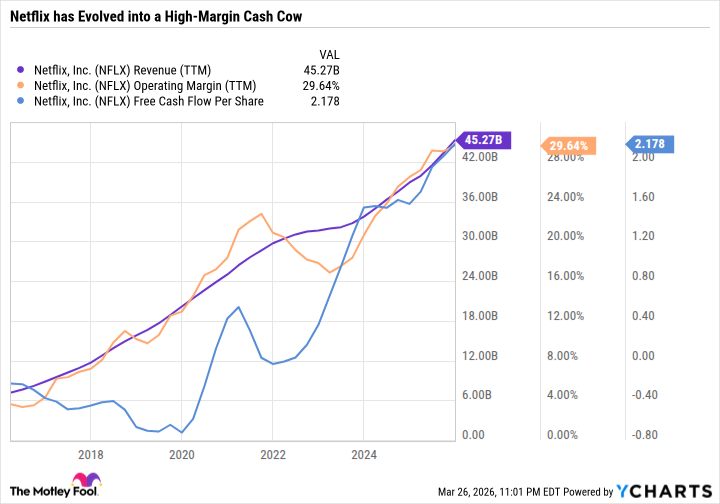

Netflix raised subscription prices to $26.99 (premium), $19.99 (standard) and $8.99 (ad-supported), and charges for adding a non-household user of $9.99 (ad-free) and $6.99 (ad-supported). Management frames the hikes as a profitability lever amid uninterrupted subscriber growth and materially higher margins; NFLX is up 184.3% over three years but remains 30.3% below its June all-time high. These hikes serve as a litmus test for U.S. consumer resilience—if subscriber losses exceed revenue gains it could signal weakening household spending and broader recession risk, but if retention holds it reinforces Netflix as a durable consumer franchise.

Netflix’s latest price move functions like a high-frequency elasticity experiment: because content cost per incremental subscriber is effectively near-zero, marginal pricing drops straight to operating leverage. A modest single-digit percentage price uplift that produces only low-single-digit churn still meaningfully lifts reported EBITDA margin within one quarter; conversely, a churn shock concentrated in lower-income cohorts would show up as a leading indicator for discretionary weakness long before headline retail sales print. Track cohort-level churn and non-household paid conversion rates on a weekly cadence for the first 8–12 weeks after the rollout — those datapoints will tell us whether the change is demand- or willingness-to-pay-driven. Second-order winners are not only Netflix but the ad-ecosystem and broadband upstream: higher ad-supported mix increases demand for addressable targeting and measurement vendors and tends to keep households on higher-speed broadband plans, supporting cable/MSO ARPU. Competitive dynamics tilt toward platforms that can absorb tiering friction (bundles, hardware lock-in) — ecosystems with large non-video revenue (e.g., commerce or devices) retain optionality to bundle and blunt pure-play pricing moves. Watch for ARPU divergence between markets with bundled alternatives (where churn will be muted) versus pure standalone markets (where downgrades to ad tiers will cluster). Tail risks and catalysts: a sharp ad-revenue contraction or a macro shock that forces widespread downgrades would reverse the thesis in 2–6 months; regulatory pushback on login-monetization or aggressive promotional responses from bundle players could also compress multiples. Practical monitoring: weekly churn by cohort, ad-ARPU and fill rates, broadband subscription growth from ISPs, and 2–3 successive quarters of margin realization — those five signals together reduce false positives and set a clear stop-loss framework.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment