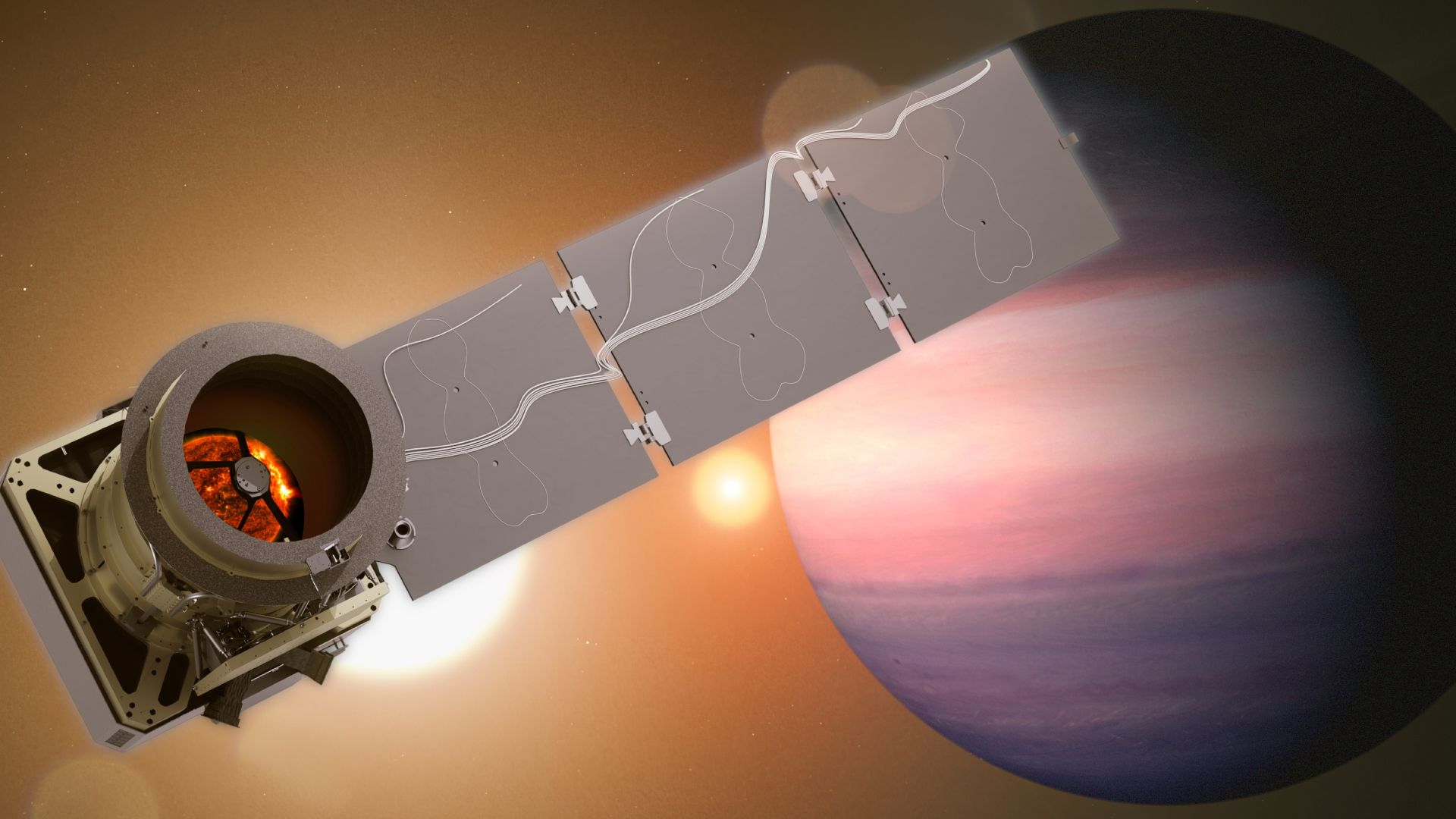

SpaceX will launch the Twilight rideshare from Vandenberg on Jan. 11 carrying about 40 payloads, notably NASA's 716-lb (325 kg) Pandora exoplanet satellite—featuring a 17-inch (45 cm) telescope for a yearlong mission to study at least 20 transiting exoplanets—and commercial satellites including 10 Kepler Aether comms craft and two Capella Acadia SAR imagers. The Falcon 9 first stage is on its fifth flight and is slated to land back at Vandenberg ~8.5 minutes after liftoff; the mission underscores continued demand for low-cost rideshares and incremental commercial revenue opportunities for smallsat operators, but is unlikely to shift broader market sentiment.

Market structure: SpaceX’s high-cadence, low-cost rideshare program (Twilight/Transporter) widens affordable LEO access and directly benefits constellation builders, smallsat manufacturers, and data buyers by compressing per-kg launch cost possibly 20–50% versus legacy dedicated small-launch pricing. Winners: data/analytics firms scaling revenue per satellite (Earth-imaging, SAR, comms) and SpaceX-adjacent suppliers with high fly-rate contracts; losers: pure-play small-launch companies facing margin pressure (price competition) and specialist launch insurers. Expect incremental pricing power shift toward large, reusability-enabled launchers over 12–36 months, driving consolidation in the small-launch segment. Risk assessment: Tail risks include a high-profile Falcon 9 failure (reputational/manifest delays), tightening export/regulatory controls (ITAR/BIS) or a defense procurement pivot that re-prioritizes government payloads — each could cut manifests by 20–40% in a quarter. Short-term (days–weeks) market moves will be noise around individual launches; medium-term (3–12 months) effects play out via manifests and backlog; long-term (1–5 years) structural lower launch costs increase supply of imagery/data, pressuring pricing for raw data but expanding downstream analytics TAM. Hidden dependency: satellite data monetization depends on timely data contracts and processing software — hardware launches do not guarantee revenue growth. Trade implications: Tactical plays favor public imagery/data leaders over small-launch pure-plays. Consider overweight exposure to diversified space ETFs (ARKX) or imagery providers with recurring revenue, versus short/put exposure to small-launch equities (e.g., RKLB) that sell based on dedicated missions. Use options to size asymmetric risk: sell limited-risk call spreads on small-launch names if implied vol spikes after missions; buy multi-month calls on high-quality imagery/analytics names to capture downstream monetization. Contrarian angles: Consensus frames SpaceX dominance as uniformly negative for all space incumbents — miss: companies owning unique IP/data, defense contracts, or vertical integration (manufacturing+analytics) will capture disproportionate value as launch commoditizes. History: containerization lowered per-unit shipping but created winners in logistics and platform providers; expect similar bifurcation. Unintended consequence: flood of low-cost satellites may trigger data gluts and price wars, amplifying value for differentiated analytics providers while punishing pure raw-data sellers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.10