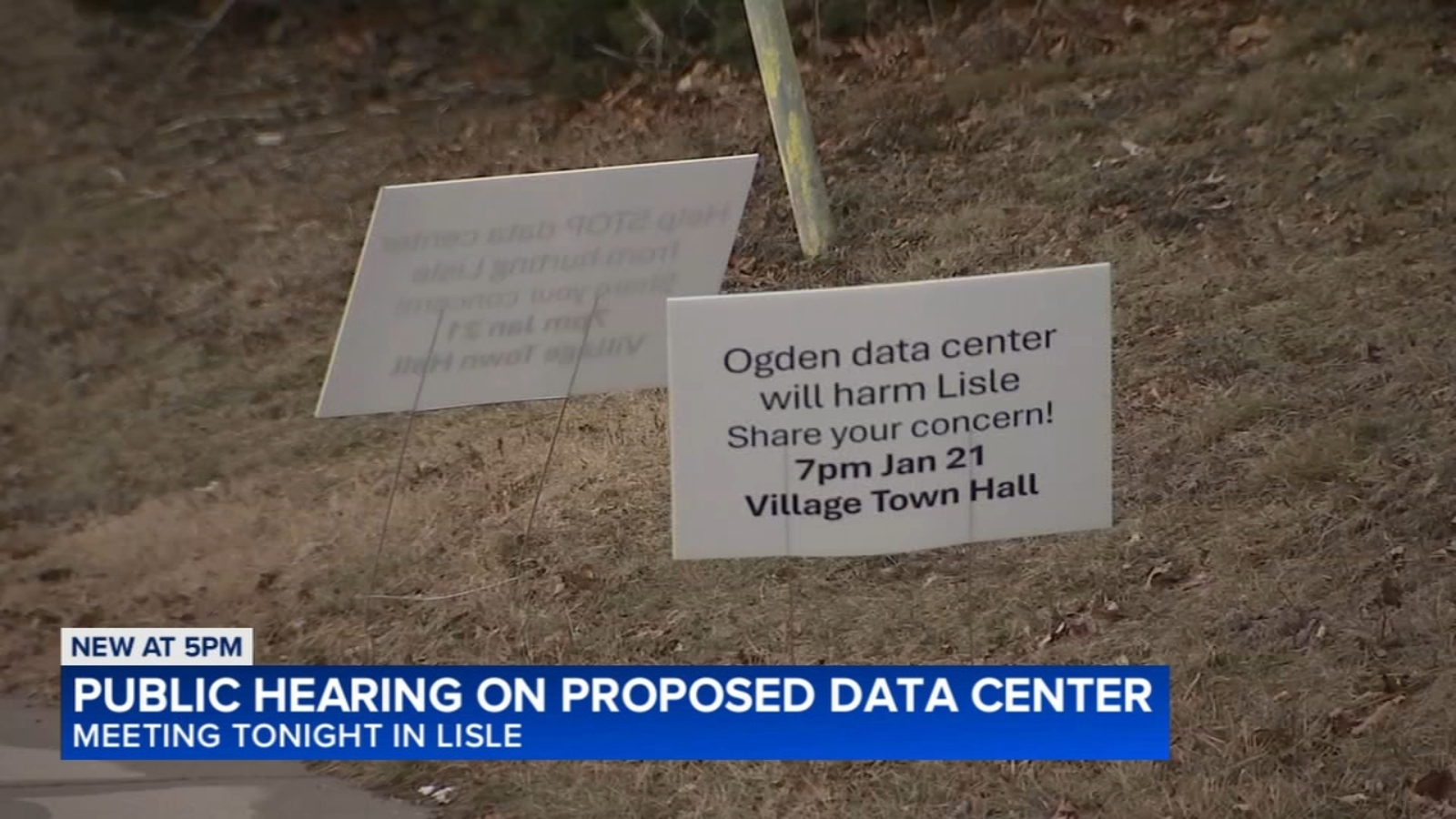

CloudCenters LLC has proposed a 50 MW, 256,000-square-foot data center on the former Lockformer site on Ogden Avenue in Lisle, prompting a heavily attended planning-and-zoning public hearing that was postponed for a larger venue. Neighbors cite concerns about diesel backup generators, air and noise pollution and proximity to homes, parks and a daycare, while Naperville recently denied a separate 36 MW project, signaling heightened regulatory and community resistance to suburban data-center builds. Lisle officials note potential tax-base benefits if redevelopment is handled safely, but developers face short-term political and environmental hurdles with a rescheduled hearing expected in three to four weeks.

Market structure: Local opposition to 36–50 MW suburban builds (Naperville denied; Lisle proposed 50 MW) favors large incumbents (Equinix, Digital Realty) with existing capacity and pricing power while punishing small/greenfield developers who rely on rapid permitting. If municipal friction trims the midwest suburban pipeline by 10–20% over 12–24 months, constrained supply could lift colocation rents in tight micro-markets by an estimated 5–15% and raise replacement-cost economics for hyperscalers (AWS/AMZN, MSFT) forcing higher site-acquisition premiums. Risk assessment: Immediate (days) risk is reputational and hearing volatility; short-term (weeks–months) risk is moratoria and permit delays; long-term (quarters–years) is structural shift to cleaner backup (battery) or relocation to lower-regulation geographies. Tail risks include coordinated county/state bans or litigation tied to contamination history causing multi-year project write-offs; hidden dependency: municipal budgets may flip from opposition to approval for tax relief, accelerating approvals if fiscal pressure >2% property tax shortfall. Trade implications: Favor large-cap data‑center REITs (EQIX, DLR) and suppliers of cleaner backup (AES, ETN) while underweight/short smaller new‑build exposed names (CyrusOne/CONE, QTS). Use 3–12 month directional equity or 6–12 month call spreads on winners; hedge hyperscaler exposure (AMZN) with modest puts if capex guidance rises or permit friction escalates. Contrarian angle: Consensus frames this as purely local NIMBY risk; the broader outcome may be accelerated electrification of backup power and higher pricing for entrenched operators, a structural positive for incumbents and battery/storage suppliers. Historical parallels (2010s local fights) show demand centers migrate, not disappear — so shorting large-scale capacity providers is likely overdone.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment