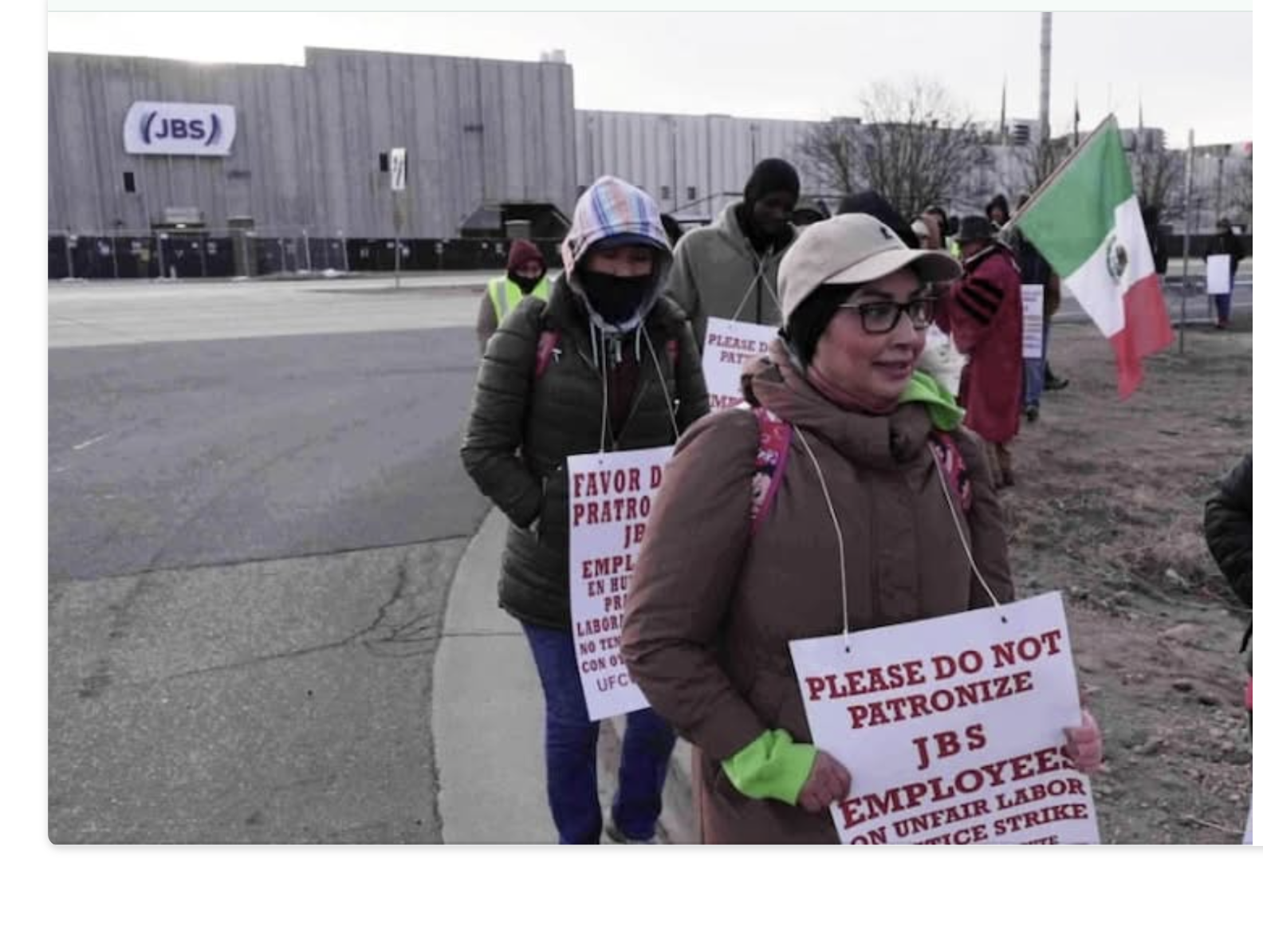

3,800 unionized workers at JBS’s Swift Beef Co. plant in Greeley began a strike March 16 with 99% support and have extended it into a third week. JBS (market cap $17B) is operating the plant at limited capacity and has shifted production elsewhere; the company offered 2% wage hikes which the union says are below inflation. Analysts say it’s too early to see a material impact on consumer beef prices, while reduced national slaughter capacity may be boosting packer margins and leaving JBS in a relatively strong position. Risk: localized supply disruption and modest upward pressure on beef prices if the strike persists.

Consolidation-driven pricing power is the hidden lever here: when a handful of integrators can flex production across plants, temporary capacity shocks translate into margin upside for the largest operators rather than supply-driven price spikes at retail. Expect the next 4–12 weeks to show packer EBITDA expansion of several hundred basis points versus pre-strike baselines if throughput stays structurally reduced; the incremental economics are concentrated at companies that can reroute supply and absorb regional labor disruption without major capital spend.

Second-order supply-chain dynamics cut both ways on a 2–6 month horizon. Prolonged reduced slaughter creates cattle backlog, putting downward pressure on live-cattle prices (benefiting packer inputs later) and incentivizing herd liquidation or retention decisions that alter supply 3–9 months out. Conversely, sustained wholesale-to-retail pass-through could depress retail volumes and accelerate protein substitution (pork/chicken), capping durable boxed-beef price gains.

Key catalysts and tail risks: a strike extension beyond 8–12 weeks materially increases the probability of government intervention, antitrust scrutiny, or settlement-driven wage steps that compress margins; an abrupt capacity reallocation by competitors or rapid re-hiring would reverse packer near-term gains within days. Monitor live-cattle futures moves (>10% vol), union bargaining milestones, and DOJ/DOI filings — any of these within 30–90 days will materially reprice the sector.

Contrarian read: the market’s instinct to punish packers for labor headlines misses concentrated optionality — large integrators are more likely to consolidate pricing power than to see permanent volume loss. That said, legal/reputational catalysts tied to past corporate behavior remain an underpriced asymmetric downside that can wipe out short-term gains if regulatory action is re‑ignited within 3–9 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment