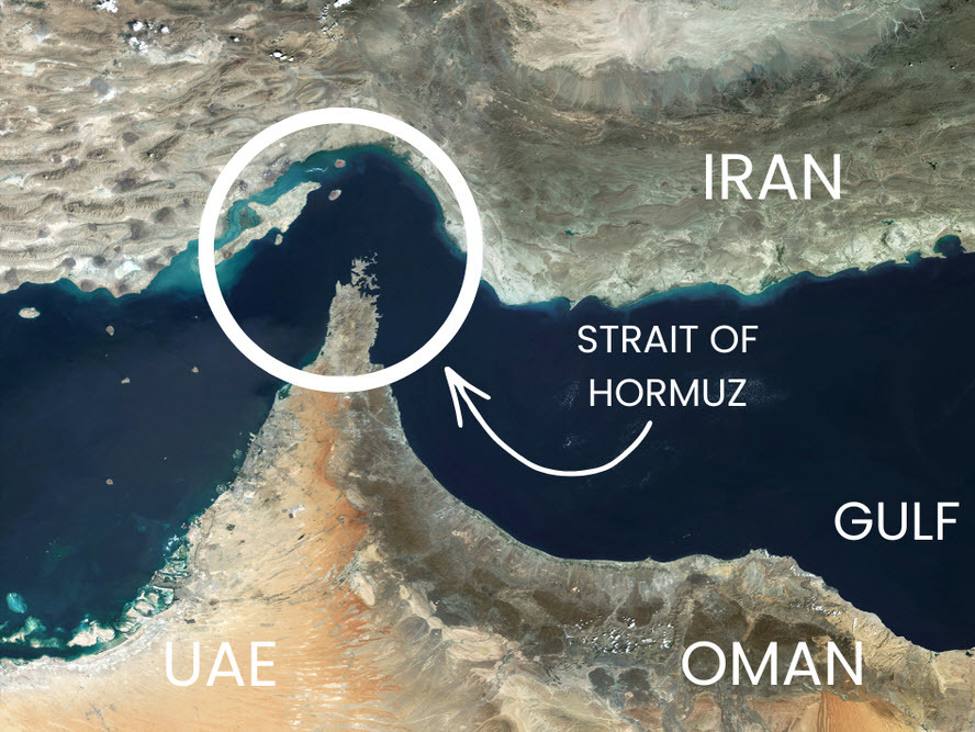

Chevron CEO Mike Wirth warned that the Strait of Hormuz closure is now close to triggering physical global oil shortages as commercial stocks, shadow fleet capacity, and strategic reserves are being exhausted. He said Asia would be hit first, with Europe next, and that the U.S. would ultimately feel the impact even as a net crude exporter. Wirth compared the disruption’s potential scale to the 1970s oil shocks, implying meaningful risks for energy prices, inflation, and broader economic contraction.

This is not just a crude-price headline; it is a logistics and balance-sheet event. When inventory cushions, chartered shadow tonnage, and strategic reserves are all being consumed at once, the next marginal adjustment is not price alone but forced demand rationing, which is why downstream spreads and physical availability matter more than front-month Brent. The second-order winner is not simply the upstream producer base, but any asset with optionality on regional dislocations: non-Gulf crude exporters, refinery systems with alternate feedstock access, and tanker exposure if ton-mile demand expands and vessel quality constraints tighten. The most vulnerable pocket is Asian industry with high fuel intensity and thin inventory coverage: airlines, petrochemicals, and container shipping should underperform before the macro data fully rolls over. Expect the first visible market damage to show up in freight, jet crack spreads, and import-dependent industrial equities rather than headline CPI, because shortages typically force margin compression immediately while inflation statistics lag by weeks. If the closure persists beyond a few weeks, the risk shifts from inflation shock to growth shock, which would pressure cyclicals and EM FX simultaneously. For CVX, the equity reaction is likely to be less linear than spot oil: upstream cash flows improve, but the market will discount the probability of policy intervention, demand destruction, and asset-level disruption. The cleaner expression is relative rather than absolute long energy, because downstream refiners with optionality on non-Gulf barrels can outperform integrated producers if cracks widen faster than crude rises. The contrarian miss is that the biggest beneficiary may be U.S.-linked infrastructure and logistics assets if Gulf-linked physical trade reroutes, while the biggest loser may be global carriers and Asian import-dependent industrials, even before oil-sensitive consumers are cut back.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.82

Ticker Sentiment