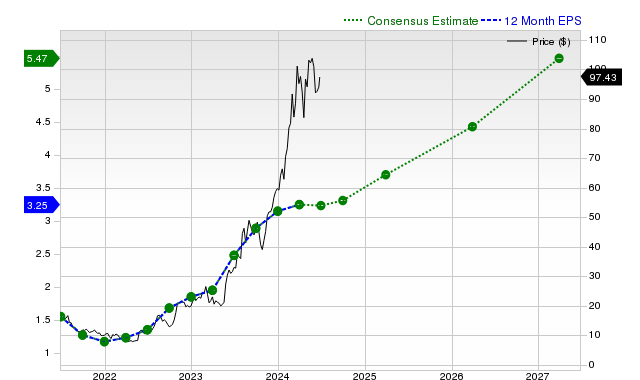

Despite recent share underperformance, Modine (MOD) has garnered a Zacks Rank #1 (Strong Buy), driven by favorable earnings estimate revisions for the current and next fiscal years, with next fiscal year EPS projected to increase 30.8% year-over-year. The heating and cooling products manufacturer has consistently surpassed revenue and EPS consensus estimates for the past four consecutive quarters, signaling robust operational performance and suggesting potential for near-term market outperformance.

Modine Manufacturing Company (MOD) presents a notable divergence between its recent stock performance and underlying fundamental strength. While the stock has declined 4.7% over the past month, underperforming both the S&P 500's +3% gain and its Automotive - Original Equipment industry's +11.9% gain, its financial outlook appears robust. The company has earned a Zacks Rank #1 (Strong Buy), primarily driven by positive analyst earnings estimate revisions. Consensus estimates project significant earnings growth, with a +14.3% increase to $4.63 per share for the current fiscal year and an acceleration to +30.8% growth to $6.06 per share for the next fiscal year. This earnings momentum is underpinned by solid revenue forecasts, with expected growth of +11.3% and +14.1% for the current and next fiscal years, respectively. Modine's operational execution is strong, evidenced by a track record of beating both revenue and EPS consensus estimates for four consecutive quarters; the last reported quarter featured a +4.86% revenue surprise and a +13.98% EPS surprise. Despite this growth profile, the company's valuation is considered on par with peers, as indicated by a Zacks Value Style Score of 'C', suggesting the stock is not excessively priced.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment