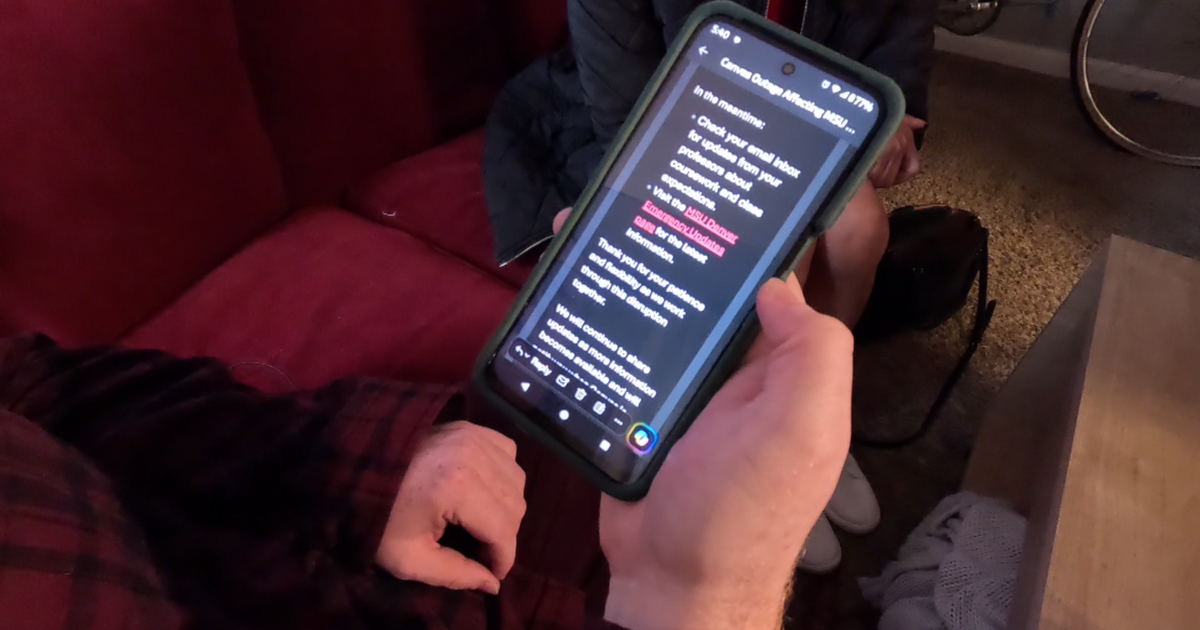

A cyberattack on Canvas is disrupting more than 20 Colorado schools and potentially affecting about 9,000 schools nationwide, with attackers claiming access to student names, IDs, email addresses, and academic records. The group ShinyHunters is allegedly extorting Instructure and has set a May 12 deadline before possible data release, raising risks of identity theft, privacy violations, and operational disruption during finals week. The incident is a significant cybersecurity event with sector-wide implications for edtech and cloud software providers.

This is less a single-issuer event than a demonstration that education software has become a high-beta critical infrastructure vertical. The immediate economic damage is limited, but the second-order cost is trust erosion: schools will reassess vendor concentration, cyber insurance underwriters will widen spreads, and procurement cycles should get longer as institutions demand offline failover, immutable backups, and incident response SLAs. That favors larger platform vendors with balance-sheet capacity and security roadmaps, while smaller point-solution edtech names face rising renewal friction.

The more important risk is liability tail. If student records are exfiltrated and publicized, the issue shifts from outage management to privacy claims, regulatory scrutiny, and potential class-action exposure. That can persist for quarters, not days, because notification, remediation, and reputational repair tend to outlast the initial technical fix; meanwhile, affected institutions may temporarily suspend integrations or reduce cloud reliance, creating a modest but real headwind for adjacent SaaS vendors selling into higher education.

The market is likely to overreact on the wrong axis: investors may focus on the breached vendor’s near-term churn risk while underappreciating the broader uplift to cybersecurity budgets across K-12 and higher ed. That creates a relative-value opportunity in cyber beneficiaries versus edtech exposure. The contrarian angle is that the incident may ultimately accelerate platform consolidation and security monetization, making the long-term impact on the category more constructive for incumbents than the headline suggests.

The catalyst window is twofold: the next 7-10 days for extortion/no-extortion resolution and disclosure quality, then the next 1-2 quarters for contract renewals, insurance repricing, and any litigation/regulatory actions. A clean resolution would blunt the immediate headline risk, but any staged data release would extend the overhang and likely trigger a second wave of institutional controls. Expect the biggest market impact not at the point of outage, but when schools quantify remediation spend and re-budget for FY26.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.72