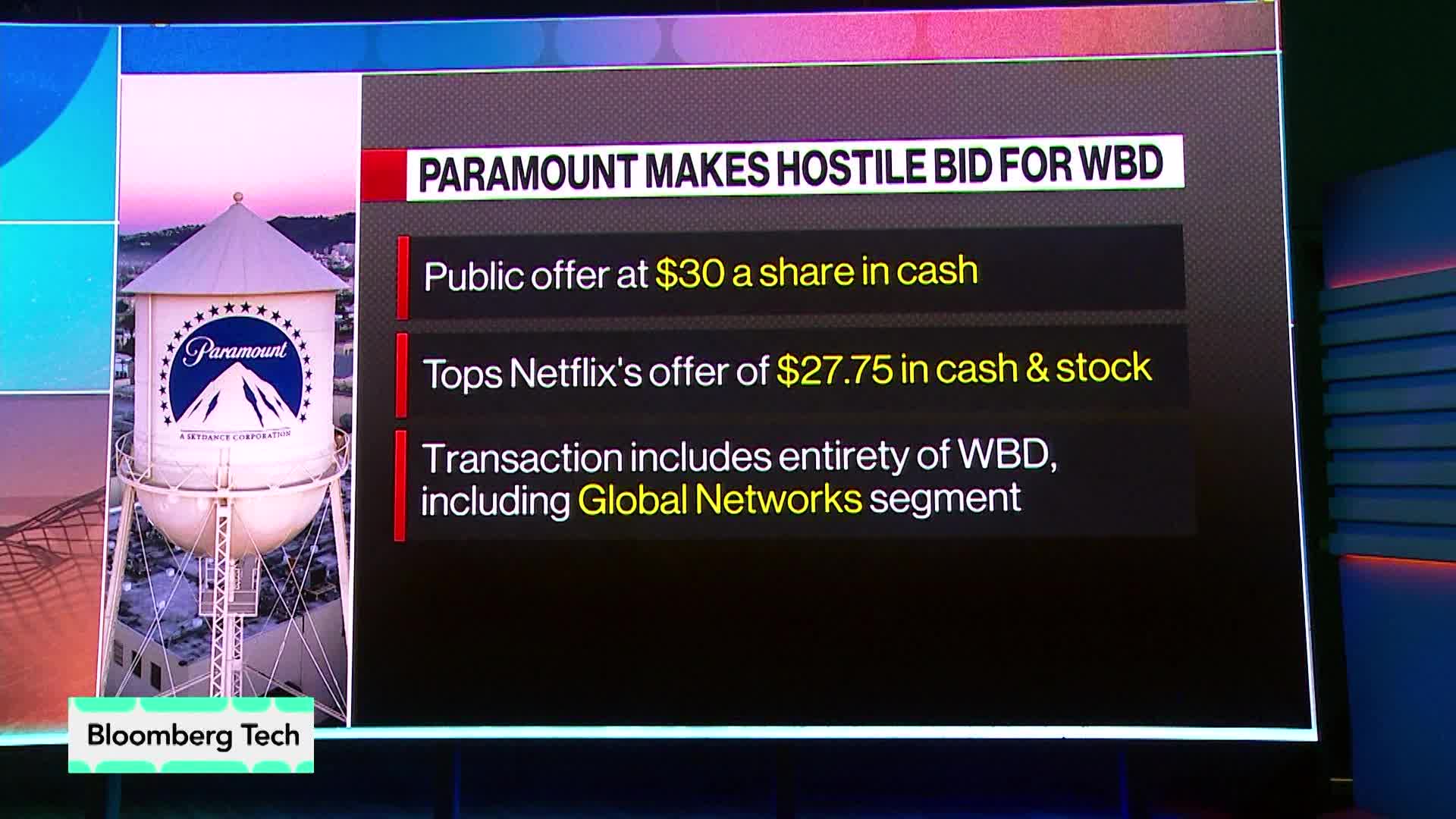

Two competing, hostile bids for Warner Bros. have created a complex takeover fight: Netflix reportedly offered $27.75 for the streaming and studio assets while Paramount/Skydance put forward a roughly $30-per-share all-assets bid, leaving the residual cable/network equity potentially valued roughly $1.50–$5 per share. Larry Ellison is reported to be directly backing about $12 billion of the Paramount bid with roughly $24 billion from three Middle Eastern investors, and both offers face lengthy 12–18 month regulatory and antitrust reviews as authorities wrestle with market definition (streaming vs. linear/YouTube), creating meaningful event risk and repositioning pressure across media equities.

Market structure: A Netflix acquisition of Warner’s streaming and studios (NFLX) materially concentrates global streaming library control and recommendation algorithms, increasing NFLX pricing/mix power over 12–36 months and pressuring mid-tier streamers (DIS, Peacock) by 5–15% EBITDA margin compression. Paramount/Ellison (private/FOXA-linked comparables) winning would preserve a standalone cable/network equity stub trading at an implied $1.5–$5/sh and keep linear-ad pricing pressure intact; ad revenues and licensing flows become the marginal arbiter of value. Cross-asset: expect widening corporate bond spreads for highly leveraged acquirers (+100–300bp) and a 20–50% lift in implied equity volatility for NFLX/FOXA around tender/regulatory windows, with minor USD bid from Middle East capital flows during deal funding windows. Risk assessment: Key tail risks are antitrust blocks (20–35% DOJ/EU probability) and host-capital political pushback from large Gulf investors (10–20% reputational/regulatory hit), each capable of wiping 15–40% off acquirer equity in a disorderly unwind. Immediate (days) risk: tender mechanics and share reactions; short-term (weeks–months): regulatory filings and shareholder votes; long-term (12–36 months): integration failure and content amortization risk. Hidden dependencies include the valuation path of the cable/network stub (range $1.5–$5/sh) and global licensing repricing; catalysts: formal HSR/DOJ filing, shareholder tender threshold events, and EU review windows within 60–180 days. Trade implications: Primary direct play is asymmetric NFLX exposure via spreaded calls (9–12 months) sized 1–3% portfolio to capture deal upside while selling higher strikes to fund cost; protect with 6–12 month puts (0.5–1% notional) keyed to regulatory outcomes. Relative trades: long SONY (1–2%) to capture stronger content licensing pricing vs reduce DIS exposure by 2–4% due to domestic box-office and streaming cannibalization risk. Options: sell short-dated premium ahead of known filing dates if IV spikes >30% vs historical, and use calendar spreads to monetize elevated term IV. Contrarian angles: Consensus treats Netflix bid as superior; markets underprice the political/regulatory stake concentration (Middle East >50% fund contribution) and overprice immediate synergy capture—history (AT&T/TimeWarner, Disney/Fox) shows multi-quarter legal friction and at times litigation risk. If Paramount wins, cable-network stub could rerate higher than consensus $1.5–$5/sh as buyers monetize live sports; alternatively, a blocked deal could create a multi-month short-squeeze in NFLX, so prepare for asymmetric outcomes on either approval or block within 60–180 days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment