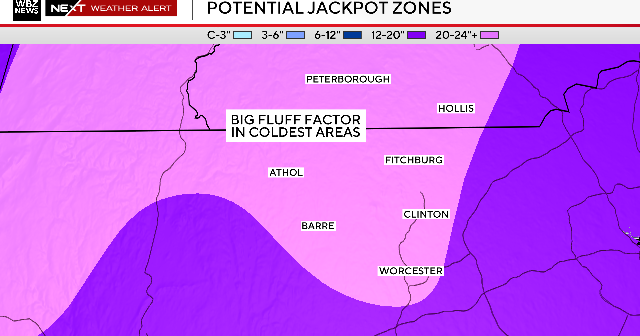

A major winter storm is expected to drop 12–20 inches of snow across most of Massachusetts Sunday into Monday, with Boston, the North Shore and upper South Shore likely in the mid-to-high end of that range and potential localized bands pushing some towns over 20 inches. North of the Mass Pike (Worcester Hills, I-495, Route 2) is forecast to receive the highest, fluffier totals possibly approaching two feet, while south/coastal areas (south of the Pike, Cape Cod and islands) face sleet, coastal-front warming and ocean-enhanced bands that could reduce accumulations to roughly 3–12 inches and produce wetter, heavier snow—heightening short-term risks to transportation, energy demand and local logistics.

Market structure: A 12–20" NE storm is a clear short-dated demand shock for salt, snow-removal equipment and short-term heating fuel (heating oil/NG). Winners: Compass Minerals (CMP), Home Depot (HD)/Lowe’s (LOW), Tractor Supply (TSCO) and regional fuel suppliers; losers: insurers with concentrated NE property portfolios and last-mile logistics providers facing cancellations. Expect a 3–7% same-week revenue bump at physical retail stores in affected ZIPs and a 5–15% intraday move in local heating fuel / day-ahead NG prices if storm intensity surprises models. Risk assessment: Tail risks include coastal flooding or multi-day outages that could push insured losses into the high tens or hundreds of millions — a scenario that would pressure P&C insurers’ near-term loss ratios by 3–8% and widen MA muni yields by 5–15bp. Time horizons: immediate (0–7 days) for retailers, fuel and power; short-term (2–8 weeks) for insurer loss recognition and municipal budget impact; long-term negligible. Hidden dependencies: diesel availability for plows, port/warehouse choke points and coastal band localization that can turn a 12" forecast into 24" locally; updated meteorological models are the primary catalyst. Trade implications: Favor small, tactical longs in salt and physical retail exposure and short-dated directional plays on natural gas/heating oil. Use options to cap downside — e.g., 7–14 day NG call spreads sized 0.5–1% portfolio. Avoid large uninsured exposure to regional muni credits; expect muni spreads to move only on sustained multi-day municipal expense increases. Contrarian angles: Consensus will overstate broad insurer vulnerability — a single localized storm rarely shifts national P&C earnings materially, so insurer equities may be oversold on headline noise. Conversely, the market may underprice localized logistics disruption risk (e‑commerce delivery misses), creating short-term alpha in long bricks‑and‑mortar retailers with strong NE footprints. Historical parallel: Presidents’ Day 2003 “jackpot band” behavior implies asymmetric upside to local snow beneficiaries if models trend heavier in 24–48h.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00