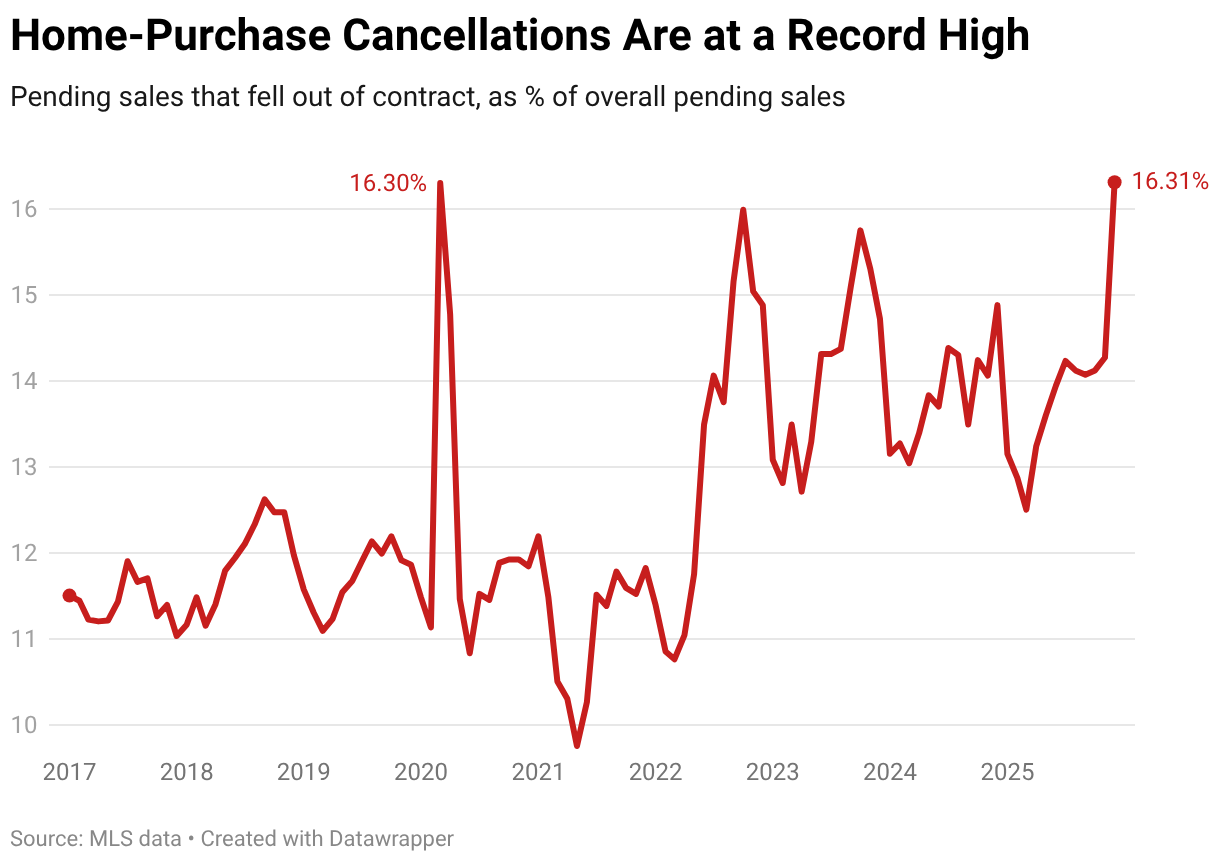

Roughly 40,000 U.S. home-purchase agreements were canceled in December, equal to 16.3% of pending contracts (up from 14.9% year-over-year) — the highest December rate since records began in 2017, per a Redfin MLS analysis. Cancellations were concentrated in Atlanta (22.5%), Jacksonville (20.6%) and San Antonio (20.6%) while Nassau County (3.8%), San Francisco (4.2%) and San Jose (8.9%) saw the fewest; several Bay Area metros registered the largest annual increases. Redfin attributes the trend to elevated housing costs and rising inventory that give buyers leverage (buyers often use inspection contingencies to walk away), though recent mortgage-rate declines and easing price growth may modestly improve affordability into 2026.

Market structure: Rising cancellations (16.3% nationally; 22.5% Atlanta) shifts bargaining power to buyers and increases effective inventory, pressuring home prices and new-build absorption. Losers: public homebuilders (Lennar, D.R. Horton, KB Home) and mortgage originators; winners: buyers, single-family rental operators (AMH, INVH) and agency MBS buyers as origination volumes and pricing concessions rise. Cross-asset: expect downward pressure on short-term rates and a bid into agency MBS/long-duration Treasuries if housing softens further, while regional banks with mortgage pipelines face credit-flow volatility. Risk assessment: Tail risks include a regional housing bust scenario (20–30% localized price drops) that stresses construction lenders and regional banks within 3–12 months, or a policy tightening of mortgage-insurance rules. Immediate (days) risk is idiosyncratic headlines; short-term (weeks–months) is inventory-driven price discovery; long-term (quarters) is demand normalization as wages outpace housing. Hidden dependencies: inspection contingencies, appraisal gaps, and rising seller carrying costs can accelerate cancellations; increased rentals could blunt price declines. Trade implications: Implement short exposure to homebuilders (DHI, LEN) via 3–6 month put spreads sized 1–2% NAV, and pair with long single-family rental REITs (AMH) or agency MBS (MBB) sized 2–3% as a hedge. Use options: buy 3-month put spreads on DHI (strike -7.5%/-15%) and collar long AMH with short calls to finance. Rotate away from home-improvement cyclicals after continued cancellations; overweight mortgage-sensitive bonds and long-duration Treasuries if mortgage rates resume decline. Contrarian angles: Consensus focuses on transient seasonality; missing is the structural hit to new‑build affordability—if cancellations remain >16% for two consecutive quarters, builder earnings will reprice 20–30%. Historical parallel: 2018–2019 regional slowdowns showed builders can quickly cut starts and margins, creating a buying opportunity in high‑quality builders on deep pullbacks. Unintended consequence: higher cancellations can boost REIT rental demand and renovation stocks (low-lift winners) before homebuilder recovery.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25