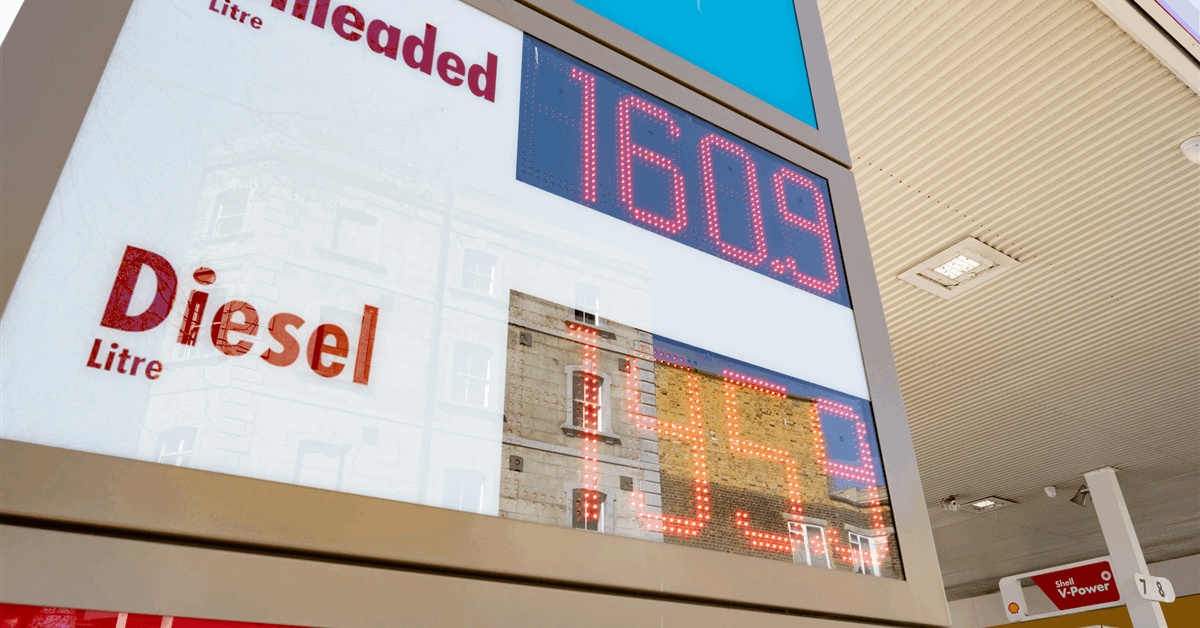

The UK will allow imports of diesel and jet fuel refined from Russian crude in countries such as India and Turkey, effectively easing part of its sanctions regime with no set end date. The move applies only to diesel and jet fuel and comes amid disrupted global supply, with ICE gasoil futures around $160 a barrel. It may modestly ease tightness in European fuel markets but does not remove broader sanctions on Russian oil and gas.

This is less a policy loosening than a re-routing of discounted Russian barrels through higher-value refining hubs, which should marginally improve middle distillate availability at the margin without materially changing crude balances. The most immediate beneficiary is not Russia, but Indian and Turkish refiners with access to cheaper feedstock and a wider arbitrage into Europe; their complexity spread should widen if European diesel remains structurally tight. The UK effectively acknowledges that sanction design is now colliding with physical scarcity, which is a signal that enforcement will remain flexible when product markets are stressed. The second-order effect is on European diesel benchmarks: if sanctioned-origin molecules are allowed back in via a processing hop, the marginal barrel becomes more fungible and ICE gasoil’s scarcity premium should compress before crude does. That matters because diesel is the global “industrial lubricant” for trucking, mining, and petrochemicals; a 5-10% pullback in gasoil from current elevated levels would relieve input-cost pressure for freight and industrials faster than for consumer-facing sectors. Conversely, any tightening of verification or a political backlash could reintroduce documentation risk and widen delivered spreads, especially for traders relying on opaque blending chains. The key risk is that this becomes a temporary valve rather than a durable supply reset. If Iran-related disruptions persist for another 1-3 months, refiners in India/Turkey gain pricing power, but if the conflict de-escalates, this import channel may look redundant and margins normalize quickly. Watch for a fast reversal if customs scrutiny increases or if EU/UK harmonization pressures force a narrower interpretation of the license. Consensus is probably underestimating how constructive this is for non-Western refining capacity and overestimating the direct benefit to end-users. The bigger trade is not “lower oil” but relative spread capture in complex refiners versus integrated producers, with the most attractive setup in firms that can source discounted crude and export diesel into tight Atlantic Basin markets. If diesel tightness eases while crude stays supported by geopolitics, downstream margins and crack spreads should outperform outright energy-beta trades.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05