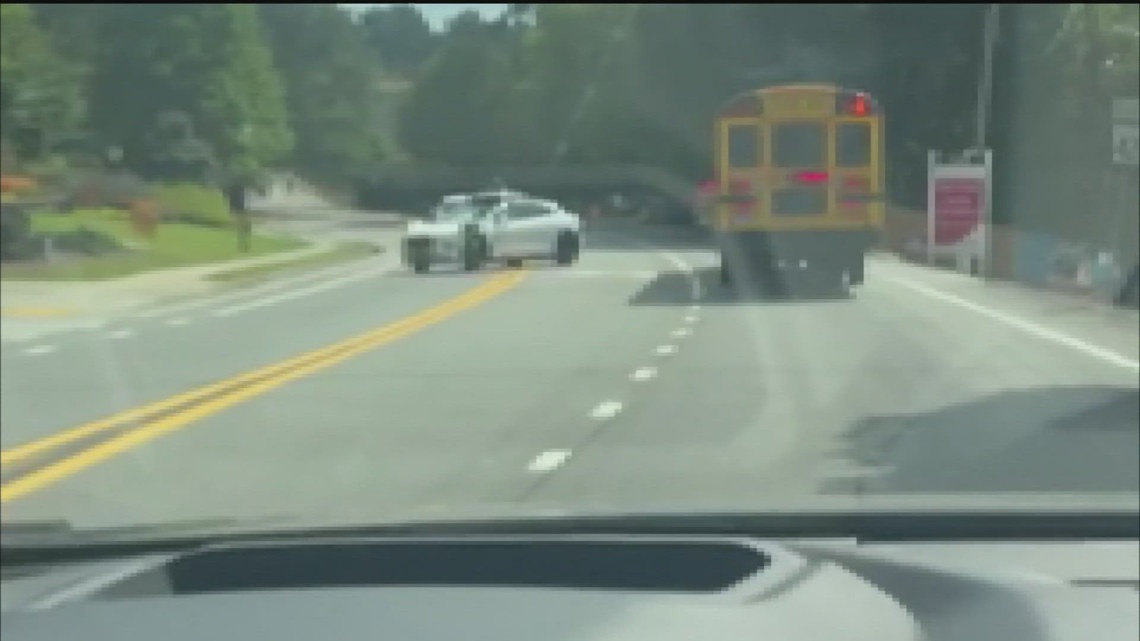

Waymo is facing a widening federal safety investigation after multiple incidents of its autonomous vehicles illegally passing stopped school buses surfaced in Georgia and Texas, with Atlanta Public Schools documenting six cases and Austin ISD reporting 19 camera-captured violations this school year. NHTSA issued a Dec. 3 letter asking Waymo for detailed responses by Jan. 20 while districts have asked the company to cease operations during pickup/drop-off hours; Waymo says it has rolled out software updates fleet-wide and cites a fivefold reduction in injury-related crashes versus human drivers. The developments heighten regulatory and reputational risk for Waymo and could pressure local operating permissions or prompt further enforcement, though the company is pushing back against operational stoppages.

Market structure: Short-term winners are well-capitalized incumbent OEMs (GM, F) and ADAS specialists (Mobileye - MBLY, Aptiv - APTV) as regulatory friction raises barriers to L4 rollout; losers are L4-focused services and the perceived standalone value of Waymo (Alphabet GOOGL). Expect a 12–36 month shift: slower robo-taxi supply, preserving human-driver demand and ADAS revenue, compressing upside assumptions for AV pure-plays by ~30–50% of previously modeled TAM timing. Risk assessment: Tail risks include a formal NHTSA finding forcing fleet restrictions or recalls (low-probability, high-impact) that could trigger a 5–12% near-term hit to Alphabet equity allocated to Waymo and legal costs for suppliers; key catalyst dates: Waymo response deadlines (NHTSA Jan 20, 2026) and local cease-operation requests over the next 30–90 days. Hidden dependency: public perception and school-bus edge cases disproportionately raise regulatory scrutiny versus technical severity, amplifying outcomes beyond incident frequency. Trade implications: Tactical hedges on Alphabet and selective longs in ADAS/legacy OEMs are preferred over outright AV-speculation. Volatility for GOOGL and MBLY should rise; use 1–3 month options around the Jan 20 window. Reallocate 2–5% of risk budget from small-cap AV names into MBLY/APTV and defensive OEMs, holding 3–12 months to capture re-rating if regulators favor incumbents. Contrarian angles: Consensus overweights headline safety risk to Alphabet’s core business; an overdone sell-off (>7–10%) would be a buying opportunity because core ad & cloud cashflows are insulated. Historical parallel: 2016–18 autopilot scares created multi-quarter drawdowns but not permanent impairment to strong-capital firms; regulatory tightening likely accelerates consolidation, benefiting players with scale and balance sheets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35