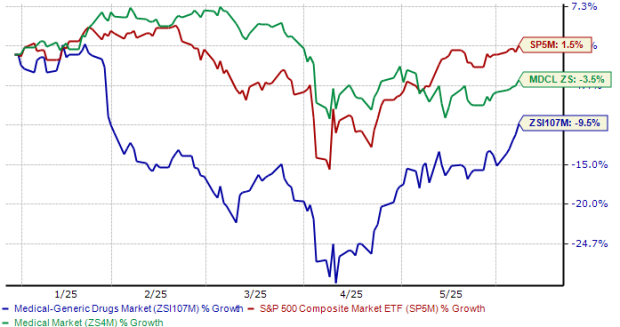

Generic drugmakers are facing headwinds from pricing pressure, potential tariffs, and the "most-favored-nation" pricing model, impacting revenues and profitability; branded drugmakers are better positioned to withstand these pressures. Despite industry challenges, Sandoz (SDZNY), Teva Pharmaceuticals (TEVA), and Viatris (VTRS) are highlighted as companies well-positioned to navigate these headwinds due to their global scale, diversified portfolios, and strategic emphasis on complex and branded generics. The Zacks Medical – Generic Drugs industry has underperformed the broader market year-to-date, declining approximately 10%.

The generic drug manufacturing sector is currently navigating significant headwinds, including intense pricing competition, the looming threat of U.S. pharmaceutical import tariffs, and potential disruptions from proposed 'most-favored-nation' pricing models, all of which exert pressure on revenues and already tight margins. This challenging environment is reflected in the Zacks Medical – Generic Drugs industry's performance, which has declined approximately 10% year-to-date, substantially underperforming both the broader Zacks Medical sector's 4% fall and the S&P 500's 2% dip, and its current Zacks Industry Rank in the bottom 25% of industries signals gloomy prospects. The industry's forward 12-month P/E ratio of 10.40X also trades at a significant discount to the S&P 500 (21.96X) and the Zacks Medical sector (19.13X). Despite these overarching concerns, certain companies like Sandoz (SDZNY), Teva (TEVA), and Viatris (VTRS), all holding a Zacks Rank #3 (Hold), are identified as potentially better equipped due to global scale, diversified portfolios emphasizing complex/branded generics, and cost optimization. Sandoz reported a 3% (ex-FX) increase in Q1 2025 net sales to $2.48 billion, driven by biosimilars, expects mid-single-digit 2025 sales growth with a core EBITDA margin around 21%, and saw its 2025 EPS consensus estimate rise to $3.17, contributing to a 51% stock appreciation over the past year. Teva, with a 7% U.S. generic market share and significant ex-U.S. revenues, leverages its U.S. manufacturing and a robust biosimilar pipeline (seven U.S., four European launches expected 2025-2027), though its 2025 EPS consensus estimate recently dipped to $2.51. Viatris has benefited from recent generic launches but faces an FDA import alert on its Indore facility; its stock declined 17% over the past year, while its 2025 EPS consensus estimate slightly increased to $2.25.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment