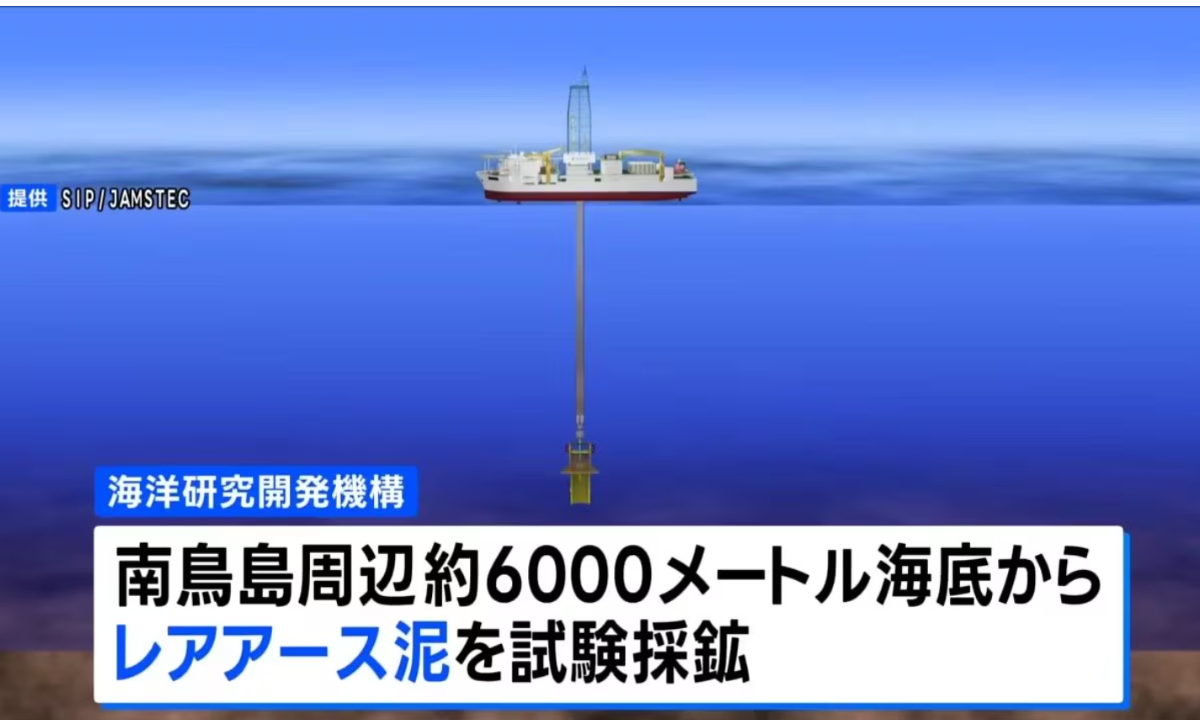

Japan is launching an experimental deep‑sea extraction of so‑called ‘rare earth mud’ in its EEZ, lowering equipment to about 6,000 meters in a trial running through Feb. 14, 2026, though departure was delayed by weather. Analysts and academic estimates warn of formidable technical barriers, extreme costs and long payback horizons (a 2019 study cited potential losses of ¥83.4bn over 20 years for some deposits and a 2013 estimate that rare‑earth mud equipment would take ~16 years to recoup ~¥75bn), while Japan still imports roughly 60% of its rare earths from China and is nearly fully dependent on China for some heavy rare earths. Beijing’s recent tightening of export controls on dual‑use items for Japan, and bilateral political tensions, raise near‑term supply‑chain and geopolitical risk despite Tokyo’s outreach to G7 partners.

Market structure: The JAMSTEC pilot is strategically symbolic but economically marginal — Japan’s 18,000 tpa rare‑earth demand vs. the study’s requirement to mine “millions of tons” of sediment implies any domestic output will be years and >¥75bn capex away from scale. Short‑to‑medium term winners are non‑Chinese processors and recyclers (pricing power for NdPr/heavy REE likely to remain with incumbents), while miners face high break‑even thresholds and capital intensity that keep supply tight and spot prices vulnerable to policy shocks. Risk assessment: Tail risks include China broadening export controls (to precursor chemicals or separated oxides) or a failed high‑pressure seabed operation leading to asset writedowns; both could spike rare‑earth spreads >20% in weeks. Immediate noise runs through Feb 14, 2026 (end of trial); medium term (3–12 months) hinges on G7 coordination, while commercialization timelines realistically stretch 5–15 years given tech and capex hurdles. Trade implications: Tactical trades should target non‑China processing exposure, capped-option structures for miners, and diversified ETF exposure to rare‑earths; bond and JPY moves are second‑order (safe‑haven flows may bid JPY on geopolitical escalation). Monitor NdPr and heavy‑REE spot moves (+/-20% trigger), China MOFCOM notices within 30 days, and pilot outcome by Feb 14 for re‑rating events. Contrarian angle: Consensus overstates the pilot’s near‑term supply relief and understates processing bottlenecks — if China’s controls force buyers to secure non‑Chinese supply, Lynas and recyclers could capture outsized margin expansion even if volumes are small (20–40% price premium on separated oxides is plausible 6–18 months out). Conversely, a quick diplomatic de‑escalation would compress premiums rapidly; position sizing and option structures should reflect this binary risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45