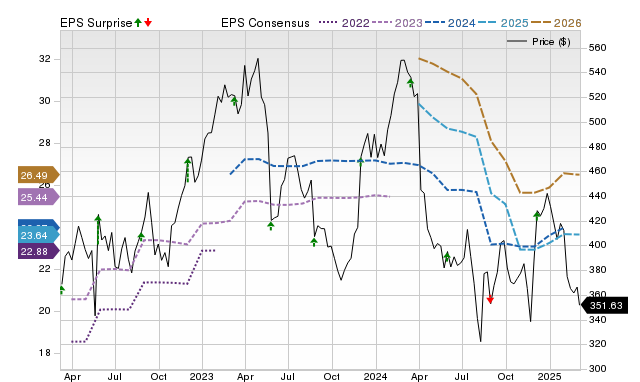

Ulta Beauty is forecast to report Q3 (ended Oct 2025) EPS of $4.51, a 12.3% year-over-year decline, on revenues estimated at $2.71 billion, up 7.3% YoY, with the print expected on December 4. The Zacks Consensus EPS was revised about 0.5% lower over 30 days, but a higher Most Accurate Estimate yields an Earnings ESP of +1.02% and the stock carries a Zacks Rank #2, signaling a higher probability of an EPS beat; Ulta has beaten consensus in each of the past four quarters (most recent surprise +14.91%). These signals increase the odds of an upside surprise that could move the shares, though falling EPS versus prior year tempers the outlook and management commentary will be key for sustained expectations.

Market structure: Ulta (ULTA) sits to benefit from resilient mid‑market beauty demand — consensus shows revenue +7.3% while EPS is down -12.3% (Dec 4 print expected), implying top‑line strength with margin pressure. Winners: private‑label suppliers, salon services, and brands with Ulta distribution; losers: low‑margin department stores and pure‑play discount outlets that rely on promotions. A confirmed beat would tighten credit spreads for specialty retail vs. mall-based peers and likely compress implied vol in options across the retail basket within 48–72 hours. Risk assessment: Tail risks include a larger‑than‑expected margin squeeze from promotions or inventory markdowns (EPS miss >5% downside), macro shock reducing discretionary spend (US consumer confidence drop >10 pts), or supply interruptions for key SKUs. Immediate risk (days): headline surprise and guidance; short term (weeks): holiday comps and inventory turns; long term (quarters): loyalty monetization and salon margin recovery. Hidden dependencies: reliance on brand assortment deals, salon throughput, and loyalty data monetization that can swing margins faster than revenue. Trade implications: Tactical approach favors defined‑risk upside — small long equity exposure pre‑earnings sized 1–3% and/or a Jan 2026 call debit spread (buy ATM, sell +10–15% strike) sized 0.5–1% notional to capture a directional move while capping vega. Pair trade: long ULTA vs short EL (Estee Lauder) at a 4:3 notional ratio for 3–6 months to express U.S. mass prestige outperformance. Post‑print, pivot to short if ULTA beats but issues conservative FY guide (cut position if FY margin guide down >100 bps). Contrarian angles: Consensus leans on another EPS beat (Earnings ESP +1.02%, Zacks #2) but may underprice guidance risk — a modest beat with conservative guide could trigger a sell‑the‑news 8–15% drop. Conversely, the market may be underestimating margin recovery from private label and salon scaling; if ULTA reports EPS in line but raises FY margin guide by >50 bps, expect a multi‑week re‑rating. Historical parallel: ULTA’s post‑beat guidance‑led rotations in 2021–22 show price action driven more by guide than quarter.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment