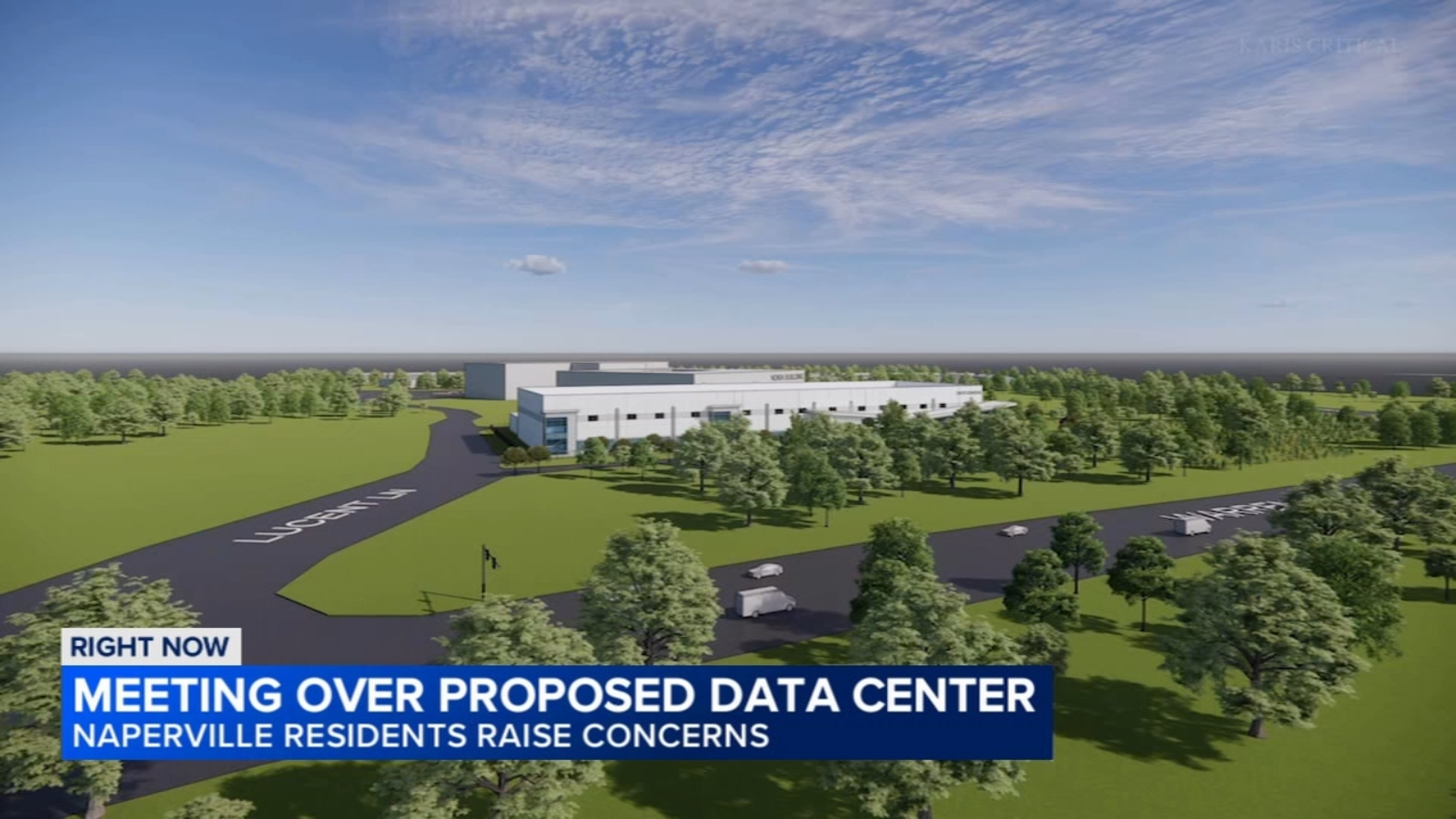

Karis Critical is seeking city approval to build a roughly 145,000‑square‑foot, 36‑megawatt data center on the former Lucent campus along I‑88, recently scaling back plans and reducing on‑site diesel generators from 24 to 12. The proposal triggered heavy local opposition—more than 5,000 petitioners and dozens of public speakers—who cite noise, air‑pollution, public‑health and property‑value risks, while the developer argues generators are low‑emission, used only for outages/testing and that commitments will be codified by the city; the Naperville City Council decision could set a regional precedent for future data‑center siting.

Market-structure: Local opposition to Naperville’s 36 MW project highlights rising frictions between hyperscale/edge data center demand and NIMBY/regulatory constraints. Winners are large, ESG-forward REITs (EQIX, DLR) and grid/storage suppliers that can offer low-emission backup; losers are smaller regional builders and diesel-generator OEMs if municipalities ban/limit diesel. Expect modest pricing power shift to operators with certified low-carbon offerings over 12–36 months. Risk assessment: Tail risks include municipal ordinances banning diesel backup or zoning freezes that delay projects 6–24 months, stranding development capex and compressing smaller players’ valuations by >20%. Immediate impact (days–weeks) = permitting delays; short-term (3–9 months) = pipeline re-routing to friendlier states; long-term (1–3 years) = capex mix shifts toward batteries/fuel cells, raising upfront costs 5–15% but lowering OPEX and emissions. Trade implications: Short-term trades favor long positions in large data-center REITs (EQIX, DLR) and battery/storage plays (AES, TSLA, BE) while underweighting regional developers (CONE, QTS) and diesel genset exposure (select Cummins product lines). Use 3–9 month call overlays on EQIX/DLR and 6–24 month exposure to AES/TSLA for structural storage adoption. Watch Illinois/other Midwestern municipal votes for regulatory templates over next 60–180 days. Contrarian angles: Consensus assumes blanket community defeats; historical parallels (Amazon/warehouse fights) show many projects proceed after mitigation and concessions. If >70% of new builds adopt grid-tied battery backup within 24 months, generator OEM revenue could reprice but overall data-center demand may accelerate land-price dispersion, creating arbitrage for REITs with flexible site portfolios.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35