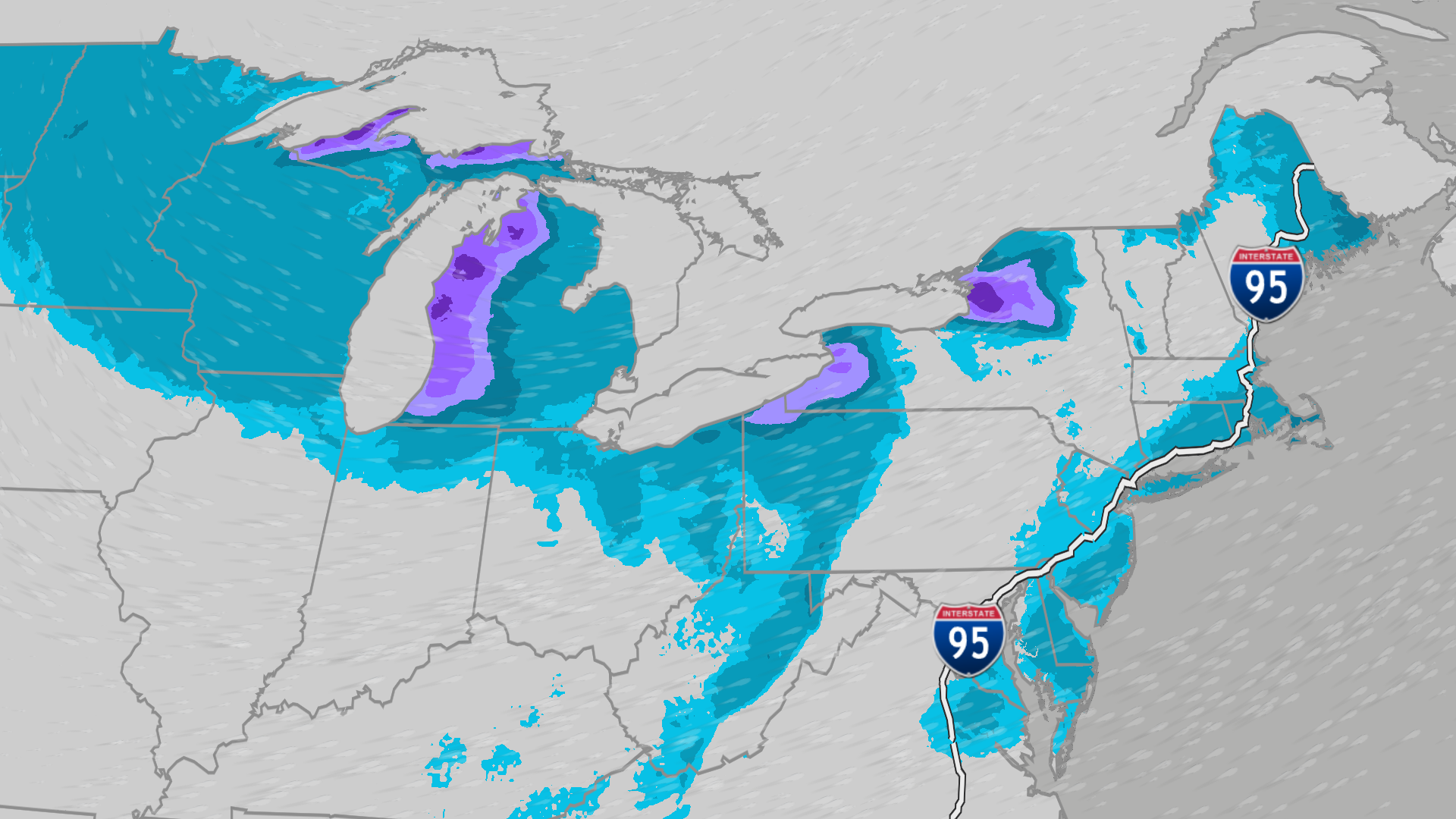

A sequence of winter storms will push heavy snow, strong winds and Arctic air across the Northern Tier and U.S. East into next week, with lake-effect bands producing up to 2–4 feet locally, 12–18 inches south/east of Lakes Superior, Michigan and Erie, 2–4 inches possible in New York City and Boston, and more than a foot in higher Appalachians. Wind chills are expected as low as 20–35°F below zero in parts of the Northern Plains and have already produced flight delays and cancellations along the I‑95 corridor; investors should monitor regional transportation disruptions, localized operational risk and short-term heating demand spikes in affected markets.

Market structure: Near-term winners are energy (natural gas, heating oil) and utilities that capture surge in heating demand, plus retailers/home-improvement (HD, LOW) and fuel retailers (XOM, CVX). Immediate losers are airlines/airports (AAL, DAL, UAL, JETS), time-sensitive logistics (FDX, UPS/short-term congestion), and regional retail/restaurant foot-traffic in impacted corridors; expect pricing power to favor large integrators and vertically integrated energy players over small carriers. Risk assessment: Tail risks include prolonged infrastructure outages (frozen pipelines, airport closures) that could spike energy prices >30% and produce insurance losses >$100m for regionals; short-term (0–7 days) operational disruption, medium-term (weeks) revenue hit for travel, long-term (Q1–Q2) potential modest margin benefit to utilities and energy. Hidden dependencies: port/rail bottlenecks could shift inventories, amplifying retail supply squeezes; catalysts to watch are NOAA model updates and weekly EIA storage data. Trade implications: Tactical commodity exposure and volatility plays are highest-conviction: expect natural gas demand to rise ~5–15% W/W during the plunge — this should lift gas forwards and power spreads; travel vol will spike, inflating IV in airline names. Credit: short-duration high-yield spreads in airlines may widen 25–75bp. Position timing: act within 48–72 hours for transport hedges; 1–6 week horizon for energy plays. Contrarian angles: Consensus underestimates operational resilience of large integrators (UPS) and the chance that short-term retail disruption boosts DIY/home-improvement sales for 4–8 weeks. Weather-induced spikes in gas/power are mean-reverting but can deliver concentrated returns in 2–6 weeks — don’t extrapolate beyond one season. Historical parallel: 2014–2015 cold snaps produced 20–40% short-term gas moves and 5–10% utility outperformance over two months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30