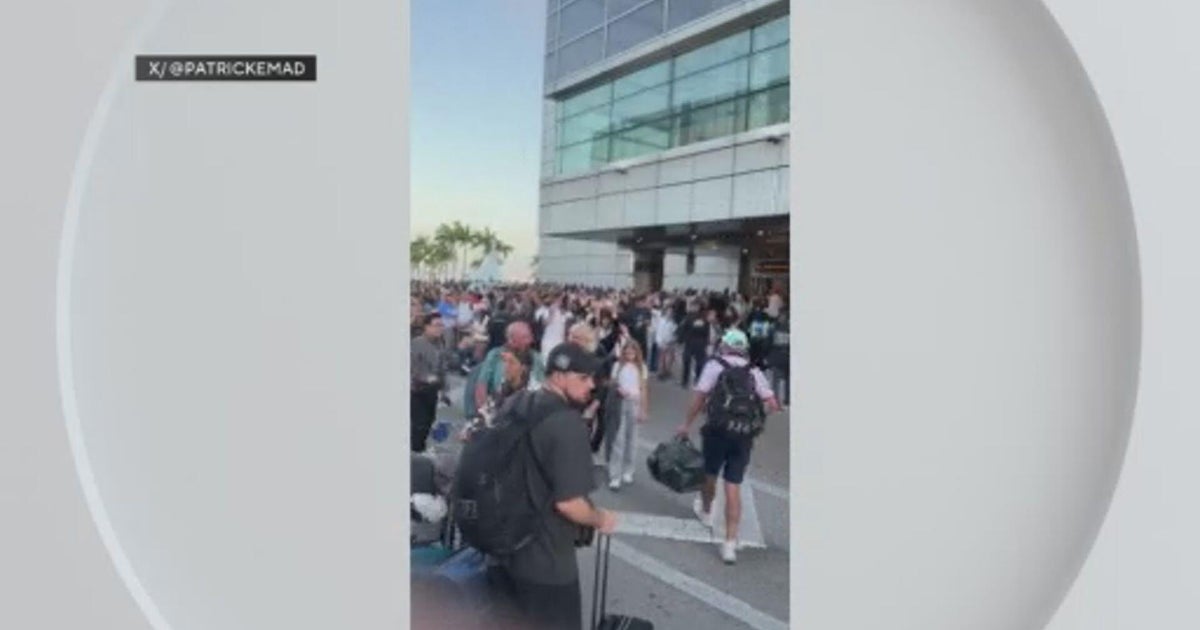

Miami International Airport briefly evacuated Sunday evening after unattended luggage was reported at Door 21 of the South Terminal departures level, prompting closures of TSA checkpoints for Concourses G, H and J and curbside roadway disruptions. The Miami‑Dade Sheriff's Office Bomb Squad investigated and issued an all‑clear around 7:40 p.m., with airport operations resuming afterward; the disruption was temporary, caused local traffic delays, and is unlikely to have material financial impact.

Market structure: This single MIA evacuation is a localized operational shock with negligible direct equity-market impact today, but it reinforces perennial winners (security hardware/software providers, defense primes) and losers (airlines and airport service operators) when incidents accumulate. Expect incremental procurement cycles (portable scanners, bomb-disposal robots, screening staffing) with procurement decisions shifting toward specialist vendors over 6–24 months; winners could see contract uplifts of 5–15% revenue annually on localized demand spikes. Competitive dynamics: Large defense primes (LHX, RTX, LMT) compete with niche avionics/security tech firms (TDY, FLIR legacy) — niches can command premium margins and win municipal contracts quickly, altering small-cap share gains in 6–12 months. Risk assessment: Tail risks include a large-scale airport attack (low probability <1% annually) that would cause multi-week travel demand shocks and regulatory hikes in capital expenditure and insurance costs; a regulatory shock could force airports to spend +10–30% on security capex over 1–2 years. Immediate effects (days) are flight delays and minor revenue loss for carriers; short-term (weeks) raises volatility for AAL/UAL; long-term (quarters) could reprice airport concession revenues and TSA staffing budgets. Hidden dependencies: municipal budgeting, federal grant timing, and TSA procurement cycles (watch FY budget windows) materially affect winners’ revenue timing. Trade implications: Direct plays include small tactical long exposure to LHX and TDY (security hardware/software) with time horizons 3–12 months, and short/hedge positions in heavily MIA-exposed carriers (AAL) via short-dated puts (2–6 weeks) sized to 0.5–1% portfolio. Pair trade: long LHX (1–2%) / short AAL (0.5–1%) to capture relative re-pricing if local incidents rise. Options: buy 1–3 month AAL 10% OTM puts to hedge operational risk; buy 3–9 month LHX or TDY call spreads to limit premium outlay. Contrarian angles: The market will likely underprice repeated ‘‘minor’’ incidents; cumulative frequency (>=3 similar evacuations across US hubs in 60 days) is the inflection that forces durable capex and re-rates specialists. Consensus misses the procurement lag: contracts awarded 3–9 months after incidents — therefore front-loading small positions in specialist vendors can capture the re-rating before large primes absorb orders. Unintended consequence: large primes may win via offset contracts, compressing small-cap upside; cap holdings should scale down if a prime secures a major TSA/port contract (> $50m).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.10