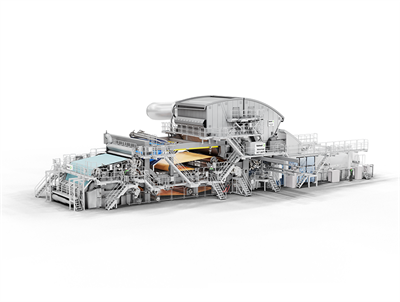

Valmet has received an order from WARAK (a Faderco Group subsidiary) for a complete Advantage DCT 200TS tissue production line, including stock preparation, automation (Valmet DNA), two Focus rewinders and full engineering, installation and commissioning; start-up is scheduled for Q1 2027. The third Valmet-supplied line for Faderco will double the group's tissue capacity—adding 65,000 tonnes/year—and targets domestic and export markets across Southern Europe, the UK and Africa while emphasizing lower energy and water use. The order is recorded in Valmet’s Q4 2025 orders received; the contract value was not disclosed. For investors, the news is a positive operational win for Valmet with modest near-term market impact given the undisclosed value and multi-year delivery timetable.

Market structure: Faderco’s +65,000 tpa tissue line (startup Q1 2027) strengthens North African capacity and export supply into Southern Europe/UK, likely depressing regional spot tissue prices by low-single-digits and raising competitive pressure on smaller local producers. Valmet (VALMT.HE) is a direct winner — order supports aftermarket, automation and installation revenues; given Valmet’s EUR 5.4bn 2024 sales, this single order is likely <1–2% of annual revenue but meaningful for niche margins and recurring services. Risk assessment: Tail risks include construction/start-up delays, Algerian export regulation or FX/capital controls, and potential machine performance/warranty disputes; any of these could push commissioning beyond 2027 or incur >€10–30m remediation. Short-term (days–months) market reaction will be muted; medium-term (6–18 months) risks center on orderbook recognition and supply-chain bottlenecks (spare parts, skilled operators); long-term (2–5 years) outcome depends on Faderco converting capacity into profitable exports. Trade implications: Primary trade is a modest long in Valmet (equipment + services exposure) with an options overlay to cap downside; secondary plays include selective longs in automation/industrial equipment suppliers and underweight positions in regional small-cap tissue manufacturers whose local pricing could compress. Cross-asset: minor upward pressure on pulp/recycled fiber demand (order implies incremental pulp demand in the tens of ktpa), negligible sovereign bond or FX impact unless Algeria policy shifts. Contrarian angles: Consensus may underweight recurring service/automation upside — aftermarket could add 3–5% to Valmet’s margins over 3 years if similar orders scale. Conversely, the market could be underestimating regional oversupply risk: if several peers replicate expansion, tissue pricing could fall >5–10% in Southern Europe, hurting producers’ EBITDA margins and making equipment OEM equities mean-reverting.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.40