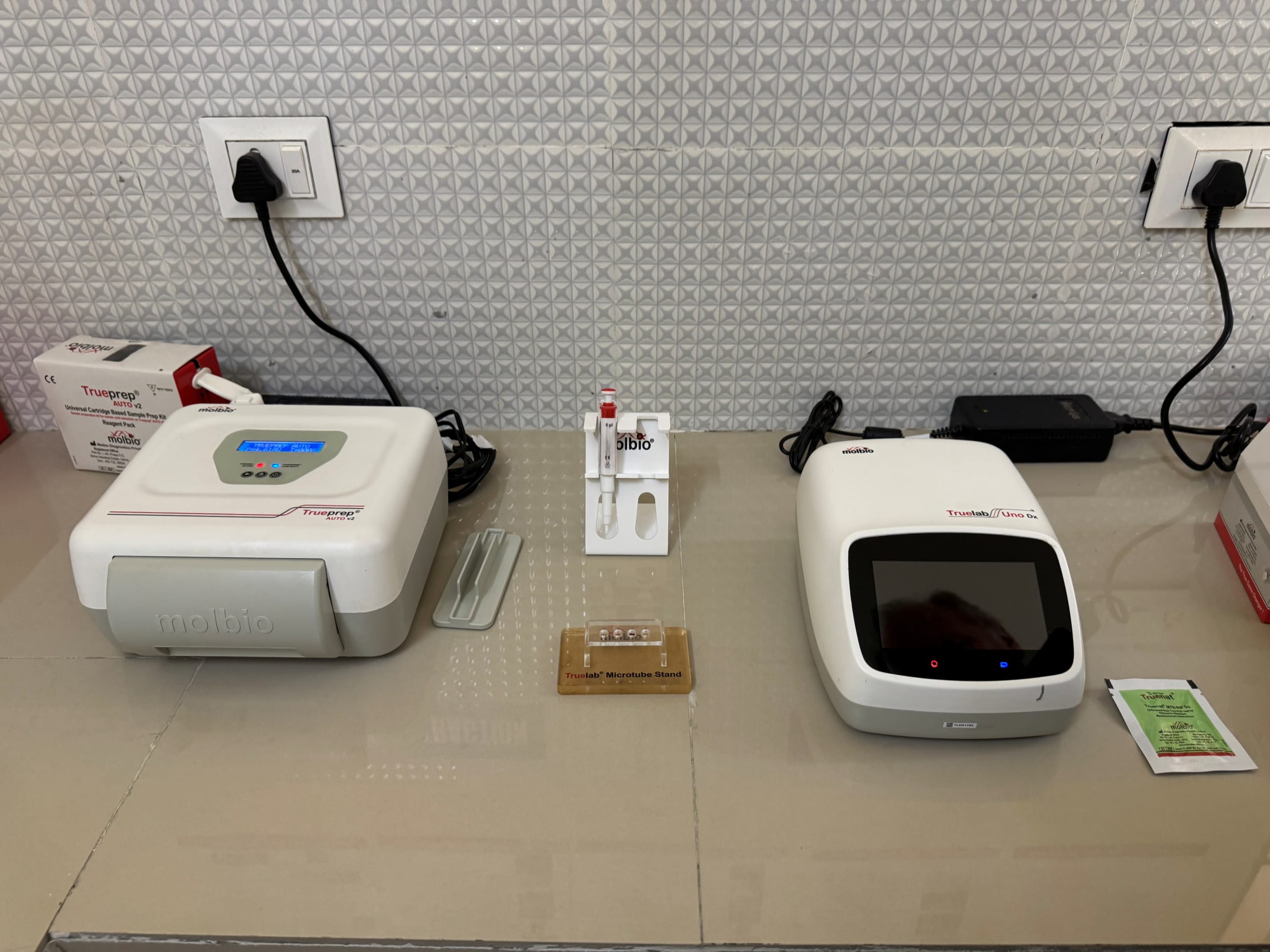

A modeling study estimates that termination of U.S. funding could cause ~10.6M additional TB cases and ~2.2M additional TB deaths from 2025–2030; in 2024 there were ~10.7M TB cases and 1.23M deaths. The WHO has endorsed near point-of-care (NPOC) molecular tests and tongue swabs, enabling decentralized testing and potential cost-effective diagnostics (Pluslife test priced at $3.60/test via the Global Drug Facility, ~50% cheaper than some other WHO-recommended rapid molecular tests). Global Fund rollouts are planned for 2026 with larger funding cycles in 2027, but deep cuts to international aid threaten program continuity, placing a premium on frugal innovations and country-led scale-up to sustain progress.

Budget compression in donor-funded health programs will accelerate two visible structural shifts: procurement decentralization (buying smaller-capacity, field-deployable platforms) and a rapid substitution of low-cost, locally manufactured consumables for legacy Western SKUs. Expect winners to be firms that can scale high-margin reagent/kit volumes while tolerating lower device ASPs; incumbents with vertically integrated consumable supply chains are best positioned to defend margins.

A realistic timing view is 6–24 months for procurement pilots to convert into recurring volume and 24–48 months for portfolio-level earnings to reflect the shift; near-term revenue volatility is likely as ministries stagger purchases to align with constrained budgets. Key operational chokepoints that could delay adoption are chip/module shortages, localized regulatory backlogs, and lack of trained end‑user support — any one can push expected revenue realization out by a year.

Second-order market effects: broader primary‑care digitization and multiplexing demand will expand the per‑patient lifetime spend on diagnostics, creating cross-selling paths for molecular platforms into respiratory, STI and antimicrobial‑resistance testing; conversely, laboratory consolidation players that depend on high‑margin centralized testing face margin erosion. Sovereign credit and social‑stability risks in heavily affected low‑income markets will rise modestly and nonlinearly, creating event-driven opportunities in EM credit and political‑risk hedges.

The main downside catalyst is a restoration of large donor flows or emergency bridging funds; a faster-than-expected uptick in donor commitments would re-center procurement around larger legacy suppliers and compress the runway for local players. Monitor three binary readouts (tender awards, component lead times, and first 6-month field sensitivity data) — a positive trifecta accelerates upside, while any single miss supports trimming exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15