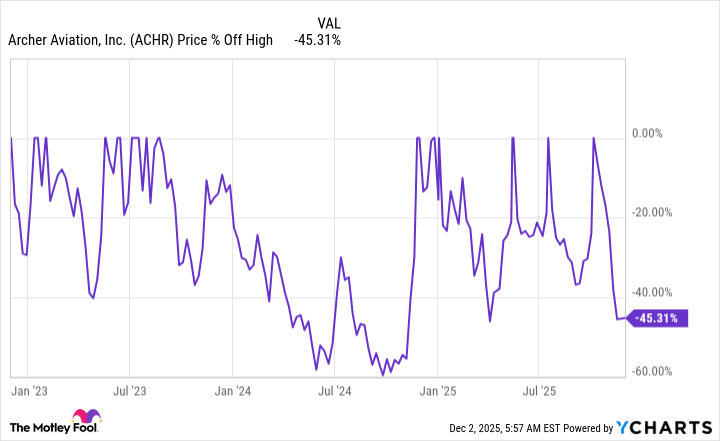

Archer Aviation shares have plunged roughly 45% from recent highs since early October 2025, are down about 22% year‑over‑year but remain up nearly 190% over three years, reflecting high volatility. The company is a pre-commercial, money‑losing start‑up that has a flying Midnight aircraft, regulatory processes underway, a planned Abu Dhabi commercial launch and partnerships in Japan, Korea and Indonesia, and has agreed to acquire control of a California airport to serve as a U.S. hub. Key risks are execution, regulatory approval and continued capital needs; successful commercialization would materially increase upside, but the story remains speculative and suited to aggressive, long‑horizon investors.

Market structure: Early commercial eVTOL winners will be battery suppliers, vertiport/airport operators and regional partners (e.g., Abu Dhabi concession holders) who capture high-margin per-ride economics; losers are incumbent short-hop helicopter operators and pure-play OEM suppliers lacking certification scale. Pricing power will be high initially (premium urban commuters) but volume elasticity will cap long-term margins until unit costs fall ~30–50% via scale. Limited supply (certification + factory ramp) creates embedded scarcity that supports volatile forward-looking valuation; options IV will stay elevated and credit spreads on small aerospace names will widen on funding concerns. Risk assessment: Tail risks include failed FAA certification, high-profile accident, or cash runway exhaustion forcing >20–30% dilution; each could halve equity value within weeks. Immediate (days) risk: headline-driven 10–30% swings; short-term (months) risk: certification/Abu Dhabi launch timing; long-term (2–5 years): adoption, pilot availability and unit economics. Hidden dependencies: airport access rights, pilot training pipeline, battery supply chain and regulatory noise/curfew rules; catalysts are FAA Part 135/air carrier approvals, first paid flight in Abu Dhabi (next 3–9 months), and quarterly cash-burn guidance. Trade implications: Tactical direct play: size ACHR exposure small (2–3% equity) and conditional on a verifiable catalyst; otherwise use option structures to limit downside. Pair trade: long JOBY (JOBY) 1–2% vs short ACHR equal dollar to express dispersion of certification/timeline risk. Options: buy 9–12 month ACHR call spread financed with nearer-term puts for protection; sell short-dated calls if owning stock to monetize IV. Contrarian angles: Consensus underprices upside if the Abu Dhabi launch occurs on schedule — a successful first 6-month commercial run could re-rate ACHR 2–3x from depressed levels because of scarcity of operating eVTOL fleets. The drop may be overdone relative to operational progress; conversely, regulatory delays create cluster downside as funding windows close. Historical parallel: early commercial drone/aircraft rollouts where first-mover service revenue materially re-priced equities, but only after surviving initial safety/regulatory shocks.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment